New Tax on Parents and 8 Ways You Can Benefit (as seen in Canadian MoneySaver)

Are you a parent? Is the income of your family between $30,000 and $119,000 per year? If so, congratulations! You are now paying the new “tax on parents”.

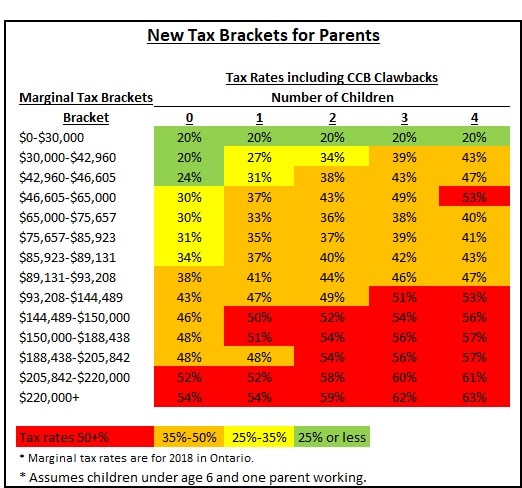

Total tax rates on parents can get very high, with marginal tax rates as high as 63%!

The new tax on parents is a game-changer! It can completely change your retirement plan. However, it also gives parents some exceptional tax planning opportunities. I’ll explain what it is, show you your new effective tax brackets and then give you 8 stories to show how you can benefit.

What is the “Tax on Parents”?

The “tax on parents” is the clawback tax that is part of the new Canada Child Benefit (CCB). The CCB provides generous benefits but is “clawed back” (reduced) if your family income is above $30,000. Your family income is the taxable income you and your spouse earn together.

The CCB pays a generous benefit of $6,400 per child under 6 and $5,400 per child age 6-17. However, for parents with a family income as low as $30,000, the benefit gets clawed back, with a higher clawback rate at $65,000 family income. The goal is to prevent families with higher incomes from receiving the CCB.

The Canada Child Benefit is both a generous benefit and a large tax increase for parents. It was introduced in 2016 with significant fanfare about the increased benefits, but there was little talk about the associated clawback “tax on parents”.

The clawback tax costs you actual money and is the same as a tax. It is delayed one year. For example, your family taxable income in 2018 determines the Canada Child Benefit you get from July 2019 to June 2020.

For example, Alex earns $50,000 per year and Emily stays home with their 2 children aged 1 and 3. Alex is effectively in a 43% tax bracket. He proudly told Emily about his $10,000 raise. However, he pays $2,965 income tax on it and their family loses $1,350 of their CCB over the next year. Alex brings home only $5,685 from his $10,000 raise.

It affects parents even at low incomes. Bob and Megan both have minimum wage jobs. They work only 3 days a week, so they can avoid day care for their 4 kids. Megan’s employer offered a group RRSP that matches her contributions. She thought her income is too low to benefit from an RRSP, but her financial planner advised her she is effectively in a 43% tax bracket. She earns only $17,000 per year, but a contribution of $1,000 to an RRSP reduces the tax on Megan’s pay cheques by $200 per year and gives her an extra $230 per year in CCB. In total, the government pay her $430 towards her $1,000 RRSP contribution.

Here are the CCB benefit amounts and the clawback tax rates:

What are the new marginal tax brackets for parents?

The “CCB clawback range” of incomes that are affected by the CCB clawback tax is family income between $30,000 and $119,000.

If you are a parent with family income in the clawback range, you have new, higher tax brackets. The charts below show your marginal tax brackets (tax on your next $1 of income) based on how many children you have.

The CCB can create surprisingly high tax rates. It also creates many new effective tax brackets, which are at the bottom of the chart.

Your new tax bracket depends on how many children you have and their ages. Here are the tax rates for a family with children under age 6 and one parent working in Ontario. The lowest line (0) is for non-parents and the 4 higher lines are for parents. Note the very high tax brackets over 50%.

8 Ways You Can Benefit

The upside of being taxed at exorbitant rates is that tax planning is far more effective for you. Every tax deduction has a much bigger benefit for you.

The Canada Child Benefit means the more kids you have, the higher tax bracket you are in. This means all tax deductions are more effective for parents, and tax planning is more effective.

Here are 5 ways you can benefit:

- Use RRSP contributions effectively. Consider your new effective tax brackets, including the CCB clawback, with all your RRSP decisions, especially:

- Whether RRSP or TFSA is better for you. Compare your new marginal tax brackets with your expected marginal tax bracket after you retire (including clawback taxes).

- How much RRSP is best to contribute. The CCB clawback tax means RRSP contributions are worthwhile at much lower incomes.

If you have no kids, RRSPs are generally worth doing if you have income above $47,000. If you have kids, then RRSP contributions are generally worth doing with any income, as long as you and your spouse’s combined income is over $30,000.

– RRSP contributions are easier for you to do with both a tax refund and a higher CCB benefit.

You get a larger benefit from RRSP contributions while you are a parent, but it may be harder to make RRSP contributions with all the expenses of kids. You can plan for this many ways including:

Use RRSP loans to make larger contributions and spread out the payments.

Defer RRSP deductions from contributions before you become a parent.

2. RRSP loans can pay for themselves. An RRSP loan in February gives you a tax refund in March, plus more CCB monthly starting July to the following June. You can use the tax refund to reduce the loan, then use the CCB to help make the RRSP loan payments.

3. Deciding whether or not to stay home with your kids? Consider the effect on the CCB. Working affects your family income and your child care costs are tax deductible (up to the limits), so both can affect your CCB. This generally makes it more of an advantage to stay home

For example, if you and your spouse each earn $50,000 and you are just finishing your maternity leave with your third child, by staying home you lose $50,000 of income, but also incur high day care costs. You can claim up to $24,000 of child care (for kids under age 6). If your day care costs $24,000, you would lose $26,000 compared to working.

However, including the CCB clawback tax, you are in tax brackets between 39% and 49%. You get about half of this $26,000 loss back between income tax and higher CCB. You really only lose about $13,000 by staying home.

4. Every tax-deductible expense is more worthwhile. For example, moving expenses can be tax-deductible. Moving to take a new job can give you significantly more CCB the next year

5. Invest in TFSAs. Shelter non-registered investments from tax whenever you can, if your income is in the “CCB clawback range”.

6. Avoid dividends and interest in non-registered investments. Invest tax-efficiently with non-registered investments. Dividends can be a disaster for you, since the CCB clawback is “gross-up” by 38%. For example, if you have 4 children and have family income between $47,000-$65,000, the CCB clawback of 23% is grossed-up to 32%, because of way dividends are taxed.

For example, if you earn $50,000 and receive a $10,000 dividend, you pay only $639 income tax, but your CCB is reduced by $3,200. You are effectively in an 38% tax bracket! You keep only $620 from a $10,000 dividend!

Focus on deferred capital gains, the lowest taxed type of investment income.

7. Consider strategies for tax-deductible interest, such as the Smith Manoeuvre. The interest deduction can give you both a tax refund and higher CCB.

8. Withdraw cash from your corporation tax-efficiently, if you are self-employed. If you have a corporation, you can pay yourself salary or dividend. The dividends are now “grossed-up” by 16%, so your CCB clawback tax is 16% higher.

This is a complex topic. If you are self-employed with a corporation, make sure you consider the CCB. You can save yourself a lot by effectively deciding how much to withdraw from your corporation each year and whether you take salary or dividend.

Plan effectively

All the government clawbacks completely change your retirement planning. They also change whether RRSP or TFSA is better for you.

The Child Care Benefit clawback tax and other clawbacks, such as GIS and OAS for seniors, change many of the tax brackets both before and after you retire.

Your retirement plan should take into account whether your tax bracket today is higher or lower than you expect it to be at your desired retirement income, including all the clawback taxes.

The CCB clawback tax is a game-changer for your retirement plan!

Any professional financial plan should include a retirement plan to retire the way you want. This retirement plan should include tax planning, where a huge factor is your marginal tax bracket today compared to your tax bracket after you retire.

The new CCB “Tax on Parents” is a game-changer for the tax planning in your retirement plan. It puts parents in significantly higher tax brackets for a large period in their working life until all children are 18.

With the complexity of the tax brackets and clawbacks, plus all the available choices for retirement vehicles and tax-efficient investing, there is a huge opportunity to save tax throughout your working life with effective professional planning.

With a financial plan, you will know your income and tax brackets throughout your life and you can plan the optimal strategy for you.

How will the new “Tax on Parents” affect your financial plan?

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

Hi Jeffrey,

I agree. There are more and more benefit programs that are clawed back and they often overlap. It can lead to bizarre high effective tax rates.

Ed

What the above revision demonstrates is the insanity that the marginal rate for someone making $48000 is more than that for someone making $90000 with 2,3 or 4 kids.

Good catch, Mike. I revised the figures.

Ed

Hi Ed,

I think the rates used for calculation have been misinterpreted. For example, from the CCB webstie:

“families with two eligible children: the reduction is 13.5% of the amount of AFNI between $30,450 and $65,976, plus 5.7% of the amount of AFNI over $65,976. ”

That means that money over $65,000 has a marginal rate of 5.7, not 13.5 + 5.7. I tested it on the CCB calculator page, and added $1000 of income to a scenario with a starting income of $75k, and it was only clawed back an extra $57.