How to Reliably Maximize Your Retirement Income – Is the “4% Rule” Safe?

You want to retire soon. What is the best way to setup your retirement income to give you the maximum cash flow that will reliably last the rest of your life?

Many financial planners use the “4% Rule”, which says that you can, for example, withdraw $40,000/year rising by inflation for life from a $1 million portfolio. Is that safe?

I studied 146 years of investment history. The conclusions are surprising:

- Most of the advice seniors are given is not supported by history.

- I found what really works to give you the maximum reliable retirement income – both how to setup your portfolio and manage your income.

Prefer an overview? Like videos or podcasts? Check out our whiteboard video and podcast episode, or read the full post below!

You will learn:

- What is the typical advice given to seniors and does it work?

- What does Ed’s study of 146 years of history show about the 4% Rule?

- Which asset allocations provide the most reliable retirement income?

- What is the main risk to your retirement for any asset allocation?

- Is it safer to hold some cash to use during market downturns?

- What are the reasons that the actual results of history are surprising?

- How can you manage “sequence of returns risk”?

- What is the impact of inflation?

- How does your risk tolerance affect your retirement income?

- What is Ed’s rule of thumb for a safe withdrawal rate?

- Are there advanced methods to manage a higher retirement income with 100% success?

“Conventional wisdom”

Let’s look at the typical advice given to seniors about to retire:

- Invest conservatively because you can’t afford to take a loss.

- The “4% Rule”: You can safely withdraw 4% of your investments and increase that by inflation for the rest of your life.

- Invest conservatively because you can run out of money because of the “sequence of returns”. A few bad years shortly after you retire can sink your retirement.

- Try to live off the interest and don’t touch your principal.

- Don’t invest more than “100 minus your age” (or 110) in stocks. This is a common rule of thumb, saying that at age 70, you should have 70% in bonds and 30% in stocks.

- Keep cash equal to 2 years’ income to draw on when your investments are down.

These 6 are the “conventional wisdom” advice typically given to seniors, but history shows that these are generally not the best advice.

146-Year Study of Sustainable Retirement Income Withdrawals

I recently did a “maximum sustainable retirement income” study. I studied 146 years of history1 to see what would have happened if you had retired each year using different withdrawal amounts, various strategies, and varying amounts of stocks, bonds and cash to answer 3 questions:

- How much retirement income can you safely withdraw from your investments?

- How should you invest to minimize your risk of running out of money?

- What strategies can reliably give you the highest retirement income?

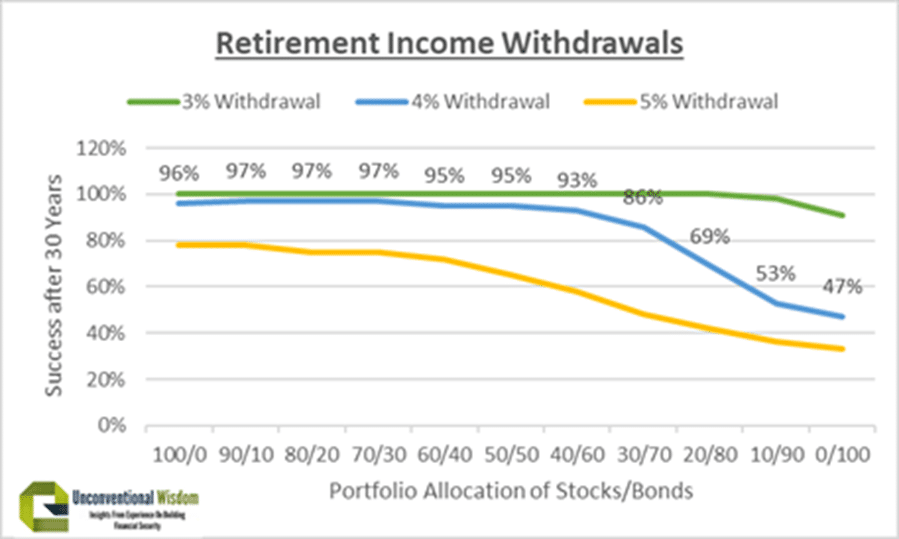

Some of the results of my 146-year study are in the chart below. The chart needs a bit of explanation:

- The “4% Rule” is not a rule. It is a guideline for a withdrawal rate that may or may not be safe depending on various factors.

- I defined a “success” in retiring as providing a reliable income rising with inflation for 30 years. That means you retire at 65 and your money lasts at least to age 95.

- The chart shows the odds of success at each allocation of stocks and bonds assuming different withdrawal rates plus inflation for 30 years. For example, looking at 4% withdrawal on the chart to test the 4% Rule, the success rate has been 96-97% with equity-focused portfolios, but only 47% with bond-focused portfolios. The allocation of stocks to bonds is most commonly done by selecting equity funds (stocks), balanced or income funds (typically 50% stocks/50% bonds), or bond funds.

- The bottom section on “Highest Success Rate” is a test of the 4% Rule. If you want to be 95% or 98% sure that you won’t run out of money, the chart shows the maximum amounts you can withdraw from your investments. For example, if you want to use the “100 minus your age” rule of thumb and have 70% bonds & 30% equities when you are close to 70, you should limit your withdrawals to 3.6% (not 4%) of your investments. 98% of the time in history, your money would have lasted 30 years.

Here is how the success rates for withdrawals of 3%, 4% and 5% have happened in history by asset allocation. Note the blue line with numbers is the 4% Rule. The most reliable is 70-100% in equities with a 97% success rate. Then is 50-60% equities with a 95% success rate, but is a 1 in 20 chance of running out of money safe enough? With less than 50% in equities, the success rate falls precipitously down to only 47% with 100% bonds.

Here are graphs showing the actual results in history of withdrawing $40,000/year plus inflation for 30 years with 3 different portfolios. Each line shows the portfolio value over 30 years for one retirement year. Note how often the line falls to zero:

Actual Retirement Success History – 100% Equities with 4% Withdrawal + Inflation

With 100% equities, your portfolio would only have hit zero only 5 times in the last 146 years. The only failures were retiring in 1929 and in the late 1960s. Note that retiring in 1929 just before the Great Depression was a failure, but not retiring one year before or after. Retiring in the late 1960s failed because the high inflation in the 1970s & 1980s made the withdrawal rate unsustainably high.

The main risk with 100% equities is not a market crash – it is inflation.

Actual Retirement Success History – 70% Bonds/30% Equities with 4% Withdrawal + Inflation

With the “100 minus age” rule of thumb, you would invest 70% in bonds when close to age 70. You would have run out of money retiring in 20 different years. These included a few times in the late 1800s and early 1900s, several when retiring in the late 1930s to mid-1940s, and most of the time retiring from the mid-1950s to late 1960s.

Actual Retirement Success History – 100% Bonds with 4% Withdrawal + Inflation

With 100% bonds, your retirement income is the opposite of safe! You would have run out of money more than half the time, including if you had retired almost every year from 1880 to 1970. For 90 years, almost everyone that retired with only bonds or fixed income using the 4% Rule ran out of money!

Results of the study

The conclusions are very useful – and surprising. The history of investments shows the following:

- Equities are safer! The more conservatively you invest, the more likely you will run out of money. At every withdrawal amount, the more you invest in stocks, the more reliable your retirement income. – Shocking!

- Fixed income is lower income. The more conservatively you invest, the lower your retirement income should be. – Not surprising.

- “4% Rule” – Yes for equity investors. No for income investors. – Surprising! The success of the “4% Rule” depends on how you invest:

- Equity investors (70+% equities) can safely withdraw 4%.

- Balanced investors (60/40 to 40/60) should reduce it to a “3.8% Rule”.

- Conservative investors (more than 60% bonds or GICs) should limit it to a “3% Rule”.

- Bond or GIC investors (no equities) should limit it to a “2.5% Rule”.

- It is safer not to hold cash. Holding cash does not protect you and may increase your risk of running out of money. It safer not to hold cash. – Surprising!

Holding cash to cover down years

Many financial planners recommend holding cash equal to 2 years’ withdrawals to draw on when your investments are down. The idea is that after a significant down year, you can live off the cash and not touch your investments, to give them some time to recover.

This sounds logical, but was not supported by the 146-year study. For example, assuming 100% in equities and a cash holding, here are the success rates for a 30-year retirement:

In every case, holding cash either had no effect or increased the risk of running out of money. I could not find a single example of a retiring year or withdrawal amount when holding any amount of cash provided a higher success rate than holding no cash.

The study showed that holding cash does not protect you. In fact, it often increases your risk of running out of money.

There is an argument that holding cash has a good behavioural effect on investors. With some cash, you may stay invested and avoid the “Big Mistake” of selling your equities while they are down. To the extent this is true, holding some cash may be beneficial for the behavioural effect only.

But cash does not actually protect you. It’s safer not to hold cash.

Reasons for the surprising results

The results of history are quite surprising, especially that investing in bonds or cash increased the risk of running out of money.

Why would stocks provide a more reliable retirement income? Aren’t they risky? What if the market crashes early in your retirement?

Let’s put some perspective on it.

The risk in retirement is running out of money. You can run out of money in 3 main ways:

- You withdraw too much from your investments.

- You invest too aggressively, your investments lose money and don’t recover quickly.

- You invest too conservatively, so that your rate of return is too low to support your withdrawals.

The study showed that the risk of stocks is real, but exaggerated, while the risks of bonds are much greater than most people realize.

The risk of stocks is short-term and medium-term market declines. The risk of bonds is long-term low returns or inflation. If there is even one period of high inflation in your 30-year retirement, you will likely run out of money if you have it all in bonds or GICs.

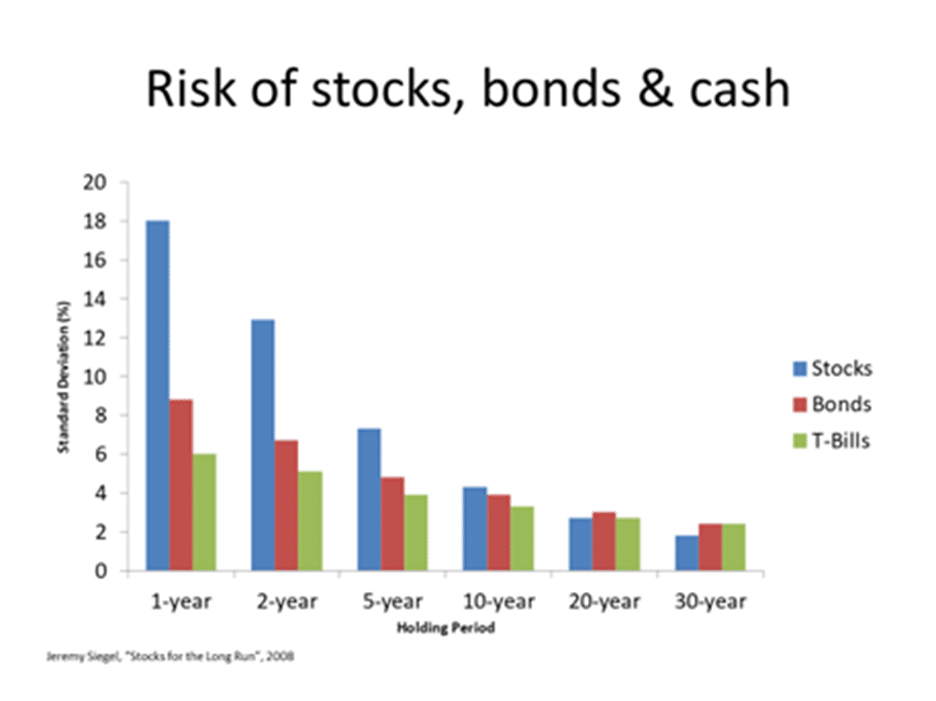

The study by Prof. Jeremy Siegel in his investment classic “Stocks for the Long Run” showed stocks are actually more reliable than bonds after inflation. The standard deviation (measure of uncertainty) of returns after inflation is lower for stocks than bonds for periods of 20 years or more.

Stocks are more reliable after inflation over the long-term.

A stock market crash early in your retirement can be a problem. Financial people call it the “sequence of returns”. However, the truth is that the stock market usually bounces back within a year or 2. Stock market losses only caused a problem over a 30-year retirement once in the last 146 years – retiring in 1929. Inflation was the problem 4 of 5 times that investing 100% in stocks failed.

We experienced this with clients that retired in early 2008, just before the largest market crash since 1929-32. They retired on track for the retirement plan, but 6 months later were down 40%. What did we do? We kept sending them the same monthly income from their financial plan. In a few cases, we had to reduce it from $100-300/month for a year or 2. In 2-3 years, their investments had fully recovered.

This is a worst-case scenario, but ended up not affecting their retirement.

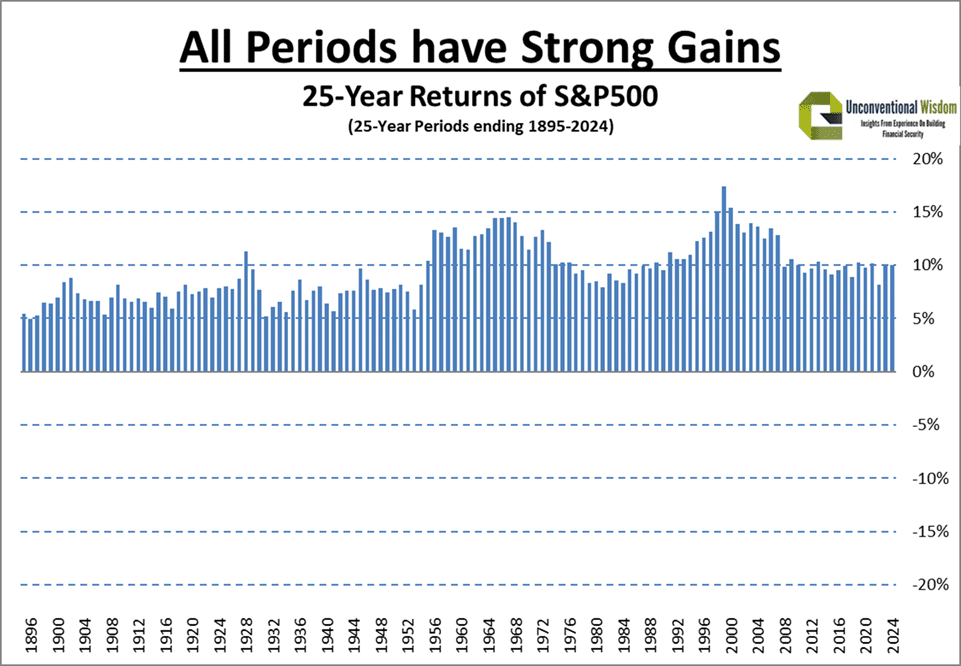

Stock markets go up and down a lot in short periods of time, but returns have been reliable over 25-year periods of time. Note that the worst 25-year return in the modern stock market (since 1930) was 7.9%/year.

This how to manage “sequence of returns”. Note it has not been an issue if you stay invested in equities for the full 25 years. Adding fixed income has made 30-year retirements less reliable. Staying invested in equities has been a far more reliable way to manage “sequence of returns risk”.

The risks of bonds is more subtle, but far more likely to happen. You can run out of money either from interest rates being low or from inflation being high.

Bonds get killed by inflation. There have been 40-year periods of time when bonds lost money after inflation. They paid interest, but your investments pay for less of your lifestyle expenses than they did 40 years ago. The longest time like this was from 1940-1980.

Note this worst period for bonds from 1940-80 started when interest rates were very low – like they were recently from 2009 to 2022.

Bottom line: Stock markets are more reliable over time than most people realize. This is the reason that equities consistently provided a more reliable retirement.

What is wrong with just investing safely in bonds or GICs?

History shows that having 100% in bonds or GICs can mean you run out of money if you withdraw too much or if inflation is higher. If you are going to invest this conservatively, you should limit your withdrawals to 2.5% of your investments per year. That means, for example, a $1 million portfolio can give you an income of $25,000, while it can be $40,000 or more for an equity portfolio.

Don’t forget that you will want your income to rise with inflation. You will have to cash in a bit of your principal every year, not just live off the interest.

Fixed income is lower income. It is important to understand this trade-off. Holding more fixed income means smaller market declines and may give you a feeling of security, but your actual risk of running out of money is significantly higher unless you live with the lower income that is sustainable.

Bottom line: Do you want a fixed income or rising income (by inflation) during retirement? Bonds and GICs are good for a fixed income, but can get killed by inflation, especially over many years. Stocks are much better at providing rising income. They tend to adjust to inflation.

Does your retirement income need to rise with inflation?

The part of retirement income planning that is most commonly missed is inflation. You need your income to rise by inflation.

Inflation is a huge factor over a 30-year retirement. With low inflation of 2%, the cost of living will roughly double during your retirement. Inflation has averaged closer to 4% historically, which means the cost of living roughly quadruples.

You have probably heard seniors complain about being on a “fixed income”. This is because they withdraw the interest only from their GICs. Their income is fixed, not rising with inflation. It is like getting a pay cut every year for 30 years. Your expenses keep rising, but your income is fixed.

Some advisors say that lifestyle expenses do not actually rise by inflation during retirement, because seniors spend less on travel and entertainment as they get older.

Others say this is often just a temporary lull. You may travel a lot in your 60s and 70s, then less in your 80s. But then you may move to a retirement home in your 80s, and have higher expenses. This is especially true if you want a nice, private retirement home, not a government one.

My own experience working with retirees is that, for the most part, income determines lifestyle. Those that have a good income tend to maintain a more active lifestyle. If you have money and health, you will likely maintain the same lifestyle through your 80s. Cruises are full of people in their 70s and 80s – especially luxury cruises. Those with limited income are forced to spend less.

The best advice is to plan for your income to rise by inflation. You don’t know what will happen. Living longer and healthier is the norm today. If you can afford to maintain your lifestyle, you will have more options throughout your life.

Planning for inflation means you can afford your lifestyle throughout your life. Remember that Income determines lifestyle.

Risk Tolerance

The surprising result that equities consistently provide a safer retirement than bonds or cash means we must discuss risk tolerance. In the last 146 years, investing 90-100% in equities has been the safest, but you should not necessarily invest this way.

It is still important to invest based on your risk tolerance. Most people have a fear of losing money and don’t really understand the stock market, which can lead to the “Big Mistake”.

The “Big Mistake” is selling your equity investments (or switching to more conservative investments) after they go down. This locks in your loss and does not allow your investments to recover.

You only get the retirement safety and higher return of stocks if you stay invested during the down markets.

The best way to think of your risk tolerance is your ability to avoid the “Big Mistake” in a worst-case scenario. If you invest 50% equities/50% bonds and there is a huge 40% market crash, your investments may be down roughly 20%. Can you avoid the “Big Mistake” with a 20% decline?

It is a good idea to get educated on stock market history. Many people don’t understand it and are scared of “losing all their money” in stocks. I would suggest the largest market crashes likely to happen in your life are probably in the 40-50% range – not 100%. I have a post specifically on this topic called “Can you be confident in the stock market?”

The highest and most reliable retirement incomes are with 90-100% in equities, but only if you can invest effectively that way – and stick to it through bear markets. There will almost definitely be very large down markets during your retirement.

If you commit the “Big Mistake” even once during your retirement, the higher returns and more reliable retirement from equities might not happen for you.

The best advice is:

- Have a decent exposure to equities, but within your risk tolerance. Don’t own equities past your ability to remain confident in a large bear market.

- It may be best to maintain the investment allocation you had just before you retired. You were comfortable with that. Most people assume they should invest more conservatively when they retire, but the 146-year study proved that increases your risk of running out of money.

- No matter what – never make the “Big Mistake” by selling or switching to more conservative investments after a market decline.

Advanced retirement income strategies

Is there a way to safely take a higher retirement income?

The main focus of my study was on choosing a withdrawal amount and increasing it every year by inflation. What if we managed the withdrawal, instead of increasing it every year?

I looked at a wide variety of ways to manage your retirement income, including only increasing by inflation in good years, having some type of cap and floor on the withdrawals, reducing withdrawals by some percent if they get too high, etc. I compared my best strategies with various studies, including several actuarial studies and some advisor formulas, such as the Guyton-Klinger strategy and the Hebeler Autopilot.

I tried to find the best formula to manage retirement income to allow a higher and safer income.

The options are complex, but I found there are effective methods that had 100% success in history with withdrawal rates of 5% and even 6% of your investments if they are effectively managed. You should be careful with these higher methods, since you will have to manage your income effectively.

Summary & Best advice: How to maximize your retirement income.

What is the best way to setup your retirement income to give you the maximum income with the lowest risk of running out of money?

- Equities are safer! Don’t assume you need to invest more conservatively just because you are retired. Retirement is for 30+ years. The median retirement age is 62 and 50% of couples age 62 have at least one of them live to age 94. Consider keeping the same allocation you had before retiring. Equities are taxed at much lower rates than bonds & GICs, as well.

- Fixed income is lower income. The more conservatively you invest, the lower your retirement income should be. Investing for more long-term growth means you can have a more comfortable retirement.

- Be smart about your risk tolerance. Invest with the highest amount in stocks that is within your risk tolerance. The more conservatively you invest, the more likely you will run out of money (at any withdrawal amount). Get educated on stock and bond market history, so you have an accurate picture of risks and returns. Watch my video, “Can you be confident in the stock market?” Make sure you can avoid the “Big Mistake”.

- Inflation is huge. Inflation will make the cost of living double or quadruple or more during your retirement. You need a rising income, not a fixed income.

- It is safer not to hold cash. Holding cash does not protect you and may increase your risk of running out of money.

- Is the “4% Rule” safe? – Yes for equity investors. No for income investors. The success of the “4% Rule” depends on how you invest:

- Equity investors (70+% equities) can safely withdraw 4%.

- Balanced investors (60/40 to 40/60) should reduce it to a “3.8% Rule”.

- Conservative investors (more than 60% bonds or GICs) should limit it to a “3% Rule”.

- Bond or GIC investors (no equities) should limit it to a “2.5% Rule”.

- Ed’s rule of thumb for a safe withdrawal rate is: 2.5% plus .2% for every 10% in equities With no equities, a 2.5% withdrawal is safe. With 70% in equities, you add .2%x7 for a safe withdrawal of 3.9%. With 75% or more in equities, the 4% Rule should provide you with a reliable, inflation-adjusted retirement income.

- Higher income is possible with effective management. You can have a higher income by withdrawing 5% or even 6% of your investments, if you can manage your income effectively or are working with a financial planner who knows how to manage it effectively.

If you are concerned about how to plan for or setup your maximum reliable retirement income, get your Free 30-Minute Consultation.

Ed

1 Market history is US data since 1871 from Standard & Poors, Barclays and Bureau of Labour Statistics. cFIREsim.

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

Hi Carla,

I discuss your question in this post: “Debunking Sequence or Returns Risk” https://edrempel.com/debunking-sequence-of-returns-risk/ .

Sequnce of returns risk is bunk for long-termm investors.

We had exactly that happen to clients. They saved the amount they needed for retirement and retired. Unfortunately, it was 2008. 6 mmonths after retiring, their investments were down 40%!

What did we do? We kept sending them the cash flow from their Financial Plan. In 3 years, they had fully recovered.

Variations of this have happened to a few of our clients. In most cases, it works out over a few years. We monitor the withdrawal rate, though. If it goes above 6% (other than the year right after a large declien), then we recommend withdrawing less until the investments recover.

This takes faith in your investments. However, it works.

And it definitely better than any alternative of parking part of your investments in low-return fixed income for years.

Ed

So I get that 100% equities are safer in the long term but how does that work with sequence of return risk? Say a couple needs 80K so 2 million, they are all in equities and retire, then the market crashes 50%. If they cant reduce their spending their retirement would be at risk. Do you recommend 3 years of cash or something else to your new retirees in order to mitigate this risk?

Hi Massimiliano,

My study is based on no management of the withdrawal rate. We studied many methods of managing it. There are a bunch with studies. I agree that temporarily reducing the withdrawal by 5% or 10% to get it back in line raised the success rate. Our method of managing the withdrawal rate would have been reliable 100% of the time in history.

Some specific countries do have less reliable stock markets, which is why we invest globally. Of the 16 major developed countries, Canada and the US ar 5th and 4th in equity returns after inflation – a bit above average. The worst, however, have been Belgium, Italy and Germany, all of which had long periods of poor equity returns. Germany also had 2 periods of losses in government bonds after inflation of more than 90%. It’s best to diversify globally and not stick to one country.

Ed

Hi Ed! Really interesting and useful read.

I did find a simulation program where one was able to let default to sp500, or plug in your own numbers. I dont remember exact numbers, but here is what I remember.

For sp500, I recall very similar (slightly lower) to what was posted here ( something like 3.9%)

Being Canadian, I did manage to get a lot of history, and found you needed a smaller but similar withdrawal rate ( something like 3.6).

European numbers proved interesting!! For many countries the numbers were way lower, and for some, there was almost no safe withdrawal rate ( ie Italy).

One thing the simulation allowed for was to allow for variation of the withdrawal rate if funds were low. If one had the ability to temporarily drop withdrawals by 10%, the chances of not running out of money dropped dramatically!! And often this “drop of 10%” was only temporary…

[…] au niveau psychologique, beaucoup plus qu’au niveau performance. Les recherches d’Ed Rempel vont d’ailleurs en ce sens (traduction libre) […]

[…] Ultimately, having an emergency fund has a positive effect on a psychological level, much more than on a financial level. Ed Rempel’s research conclusions explains it perfectly well: […]

[…] instance, one interesting one that I’ve come across would be by Ed Rempel, who did a 146-year study to look for the maximum sustainable retirement […]

Hi Phil,

No, they are not relatives. It is a stock photo purchased from a photo site.

Being from Winnipeg and living in Toronto, I can usually pick out the Manitoban in any group. It’s the one really nice person. Perhaps that is what drew me to this photo! 🙂

Ed

Thank you, Ed for taking the time to answer my questions in some detail. Very helpful.

By the way, I’m intrigued by the photo of the twins that prefaces one of your articles. They look remarkably like two women who were good friends of my wife (who has since passed away) in Brandon, MB some 15-20 years ago. I can’t remember their names, but it seems to me that one of them was Brenda. Are they relatives by any chance?

Hi Phil,

To answer your questions:

1. I posted these results 4 years ago and nobody has questioned them. The results are factual. The returns of the stock & bond indexes and inflation are public. Some people with conventional thinking don’t agree with my advice from it, but the figures are all factual.

2. Yes, this is based on S&P500 and bond index returns. An index fund or ETF would obviously have a bit lower return for both stocks and bonds, which would not change the recommendations.

Global stocks have had a somewhat lower return than US stocks since 1950, averaging 9.5%/year vs. 11.7%/year for the US. Since 1900, the US has the 4th highest stock market return of the 16 major market indexes, so it’s not completely exceptional. The US has been the main growth engine for the world, but that is changing with Asia and the US being the 2 major growth engines today. Whether the US will continue to outperform the world stock market over time is a challenging question.

I just answered another question about US vs. global stocks in more depth. I would suggest a mix is the best. Our All Star Fund Manager portfolio manager invests today with 3 All Star global managers and one Al Star US manager. These are chosen because of the manager skill, not primariy because of a top-down allocation decision. It’s a bottom-up allocation.

3. Intersting question. I do believe that good stock-pickers can outperform the S&P500. The US equity All Star Fund Manager our portfolio manager is investing with today has a 30-year track record beating the S&P500 by 3%/year after fees. I believe this is skill.

You have to understand why a method outperforms and whether that will continue. Many factor-based methods may have worked in the past, but not necessarily in the future.

For example, the Dividend Aristocrats has a long-term good track record that stopped outperfroming by 2015 and I think is likely to lag in the future. Like any income-based investment, it does well in declining interest rates, but the 38-year period of declining interest rates appears to be over.

The Dogs of the DOW or other value-style methods may have trouble outperforming going forward.

The point is that any factor-based or style-based method goes in and out of favour. The past record may or may not continue.

True stock-picking skill should adjust to different markets. There are some skilled investors that are likely to continue to outperform based on skill.

I can’t comment on any specific investment advisory service.

I wouldn’t be deterred by short-term higher risk, if it is truly superior stock-picking skill. As a financial planner, I think long-term. I define risk not as short-term market fluctuations or declines, but as how predictable the 20-year or 3-year returns are expected to be.

Ed

Hi Ed,

Thank you so much for a very informative and admirably clear article. I have a few questions:

(1) I presume you have taken the results of this research and run them by various respected peers. Have you found that any of them disagree with your conclusions?

(2) I gather from your response to an earlier query, that you used the S&P500 as the benchmark for modelling those equity investments over the 146 years. So you were assuming that the equity investments in question took the form of an index fund/ETF that held all the stocks in the S&P500? Do you know if the results would have been significantly different if you had used a global index fund?

(3) There are some investment advisories that select individual stocks and that beat the S&P500 by quite a large margin, and have done so quite consistently over 20 years or more. They may be somewhat riskier over the short term, but would you agree that they could reliably outperform the S&P500 over the long term? And, if so, could not that retiree increase the amount of his reliable annual withdrawal by following

such an advisory? Or perhaps using it for part of his equities (with the other part in an index fund)? I realize that it would require somewhat more time devoted to tending to his investments, but could this not be done without undue risk?

[…] bonds at all costs. However, recent content from the Explore FI Canada Podcast (linked above), Ed Rempel’s Blog (the financial advisor interviewee) and Liquid Independence at Freedom Thirty Five Blog have […]

[…] older post by Ed Rempel who wrote about how to reliably maximize your retirement income. Here are some key points from the […]

Hi Vee,

What country are you in?

All you really need is a long history of actual returns on stocks, bonds, cash and inflation. After that, it’s just calculating what would have happened in history over 30-year periods with various portfolios.

I received a lot of help from the FIRE community with this. Is there a FIRE community in your country, Vee?

You could just refer to my research. Based on a comprehensive book “Triumph of the Optimists” that compared returns on stocks, bonds and cash for the 16 largest industrialized countries in the world since 1900, the main message of the high long-term success of stocks and the failure of bonds in any country that had a period of high inflation applies to all these countries.

Ed

Hi Ed! Really interesting and useful read. Was wondering how I can come up with my own version of your table and charts to reflect sustainable retirement income withdrawals for my country? What info would I need and how would I input it into Excel to generate the same?

Hi Isabelle,

Good question. I applaud your effort to try to figure other markets or currencies. Finding the data is a major challenge.

Your figures do not look accurate, though. For example, the $C was at about the same value 20 years ago than today. It was higher and lower for a while. This means the 20-year returns of the S&P500 should be about the same in the 2 currencies.

Thanks for the earlyretirenow site. I have not seen it before. It is very interesting.

Ed

Hello Ed, thanks for this article. I guess that you have done this research with US data for going back 146 years. Have you by any chance have done some research with our Canadian return? I downloaded the return of different stock market in canadian dollars from https://www.libra-investments.com/re01.htm.

I compared them with the return of investing in US$ and there is quite a difference because of the currency movement. After that, I’m quite worry that I’m investing in CAD, but I’m not sure if I have done the correct maths.

By example 48 years of investing in S/P 500 in a fund USD currency and CAD currency.

annual return USD$ CAD$

48 years 0,53% 6,65%

35 years 11,52% 8,94%

30 years 10,71% 8,28%

20 years 7,20% 4,55%

15 years 9,93% 6,42%

10 years 8,51% 9,36%

5 years 15,80% 19,43%

I wanted to do the same kind of study as you but with these return, but I’m not sure where to begin. If you would done that, I would be very grateful.

also, since you are interested in the Safe Withdrawal Rate, I don’t know if you have read this blog. That is quite an extensive research: https://earlyretirementnow.com/2016/12/07/the-ultimate-guide-to-safe-withdrawal-rates-part-1-intro/

Hi,

Thanks for sharing about these today I learned some new knowledge from this post. Keep sharing such as like this informative article. These Unique ideas helped me a lot. I and my friends are reading your article regularly. Please keep writing. It is inspire us.

Hi Marti,

I use the S&P500, since it is the index we have the longest history for.

It was less than 500 stocks, but the entire US stock market before 1926.

Ed

Which benchmark(s) are you using to model “Equity” investments over the 146 year timeframe?

[…] of the interview I did late last year with Certified Financial Planner Ed Rempel. On his blog Unconventional Wisdom, Ed reviewed his interesting research which reveals that if you want to withdraw 4% a year from […]

You are the best. Thanks a lot for the truly great job.

Corner Tub

Hi Richard,

I agree with you. There might be a behavioural advantage of holding cash for some people. If it prevents you from selling equities at the bottom of the market, then there is an advantage.

I have had a few emails from people that also said they agree with my article completely, except for the cash holdings.

There are a variety of defensive measures that could have the same effect. All will probably reduce your returns over time, as well.

I spend time educating my clients on bull and bear markets, and do “life boat training” during good markets, so they are ready for a market crash. If I am not confident they will stay invested, I go with a more conservative portfolio.

My point is that many financial advisors think there is a technical advantage to holding cash. There is not. I was struck by how pronounced the results were. The success rate in avoiding running out of money by holding cash in the last 150 years was 0% – in my study and others. This success rate of 0% held regardless of the withdrawal rate or the size of the cash holding.

The studies also show the size of the estate after 30 years was smaller 100% of the time with a cash holding.

Clients should know that the only benefit of holding cash is behavioural.

Ed

[…] These rules of thumb are not supported by history. I studied 146 years of history of stocks, bonds and inflation and found these common rules of thumb are generally not You can read the study here: “How to Reliably Maximize Your Retirement Income – Is the “4% Rule” Safe?“ […]

That is a very good tip particularly to those new to the blogosphere.

Short but very precise information… Appreciate your sharing this one.

A must read article!

I will acknowledge many of these suggestions may have statistical merit. However, one suggestion is ridiculous… Suggesting that retired individuals NOT hold onto a pot of cash is a triumph of esoteric logic over common sense. Cash provides psychological peace of mind. Cash reduces the urge to panic sell during a downturn. Cash provides flexibility for exigent circumstances. Cash provides time to exhale, while deciding what to do in a down market. Thanks but no thanks. Two years of cash is good for the soul of a retired person.

Good blog you have here.. It’s hard to find quality writing like yours nowadays. I really appreciate people like you! Take care!!

Hi Marianne,

My quote for you: “Investing is the last 20% of financial planning.”

You are driving to California. A Financial Plan is a GPS. By focusing on investing, you are looking for a faster car. That way, you can drive off fast in some direction or other… 🙂

Just my insight. Hope it’s helpful for you, Marianne.

Ed

Touché, Ed 😉 Yes, I need a plan, there’s so many variables at this stage it’s hard to manage even the basic possibilities nevermind the stuff I know I don’t know, nevermind again the stuff I don’t know I don’t know!

Real numbers would be fabulous, but it all hinges on investments so I guess that should be my first stop. Thanks for your input and I appreciate your work!

Marianne

Mark,

I agree completely. Your comment shows the issue with managing retirement income.

Take too little, and you die with millions you could have used to enjoy your life more. Take too much and you can be in your 80s and run out of money.

My question to you is: What risk of running out of money can you live with? Is 20% risk of running out of money too high for you?

You can take 5%/year and increase it by inflation with a 20% risk of running out of money for a 100% equity investor. 25% risk for a balanced investor. A 60% risk for people following the “age rule”.

I studied many methods to effectively manage retirement income and have found ways to take up to 6%/year and increase by inflation and still have 100% success in history. As you age, you can start to increase this withdrawal rate.

The real answer to your comment is effectively managing your retirement income yearly through your comfortable retirement.

Ed

Hi Em Jay,

I read your question and yes, something comes to mind. You need a Financial Plan!

You have many options. How long do you work full time? After that, how long do you work part time? What will your income be at each stage? How much income do you need to have the lifestyle you want?

There are probably options you have not thought of. When you can control your employment income, CPP & OAS, pension, taxable and non-taxable investments, there are often creative options to give you more income with less tax.

My experience from doing 1,000 Financial Plans is that you need real numbers to make these life decisions effectively. That is what a Financial Plan gives you.

Ed

Okay, I now understand how the 4% rule is designed to almost garauntee your money will outlast your life and you can rest easy.

How about this though. That million dollars you had in 2018 has given you your $40,000/year and actually grown to two million over the last twenty years.

With no children and no one to leave your money to, am I going to feel anger and regret that I didn’t spend a bit more on my dreams earlier on?

Absolutely!

Hi Ed,

I was glad to find this article! I’m all in on the 4% rule. I’m 36 with a same-aged husband and we have 3 little kids. Because we have decided to have a stay at home parent we won’t make that million fast enough to free me from my decent government job super early, I’m starting to see opportunities to build our portfolio ASAP to $500,000 for example (mostly in index fund equities, a bit of bonds for stability) I could work part time with the gov to supplement income from investments, ride out my years of service until pension and all that fun stuff kicks in. I’ll have 30 years of service at 57 years of age and if we’re focused with building out portfolio together (adding husband’s income once our littlest starts school in 4 years) I can see a path forward with lots of family time, minimized time in the office, and a pretty good life. I know part time work will affect pension, is there a calculator online I can play with? I’m interested in trying out scenarios (income from investments, pension income with part full time and part part time) to flesh out some options. I feel like the best time to plan your retirement is 10 years ago and the second best time is now! Do you know of any such calculator? The pension bit on the GC site is ok, but I’m cobbling together a few different vehicles. I see full time work to start (as it is now), giving in to part time work plus maybe some passion project income supplementing as portfolio increases , then pension taking over as time passes, or 4% rule investments take over our living expenses, whichever comes first. Does anything come to mind when you see this? I would like to win at life 🙂 Thank you!

Hi Mark,

Yes. You got it.

Ed

Hi Ed

Okay, I think I am getting it. It’s all about managing the risk of the unexpected. Sh*t does indeed happen!

Thanks for your help.

Best Regards

Mark

Hi Mark,

Good question. A related question I am often asked is, “If my investments are expected to make 8-10%/year long-term, why is it only safe to withdraw 4%?”

The issue with retirement income is that retirement is long and there are many uncertainties, mainly inflation and your investment return.

The focus is on the big retirement risk, which is running out of money. What happens if something goes wrong?

If you look at the colourful graphs showing actual history using the 4% Rule with 100% equities, you will see that on average you start with $1 million and die with about $4 million.

For most people following the 4% Rule with 100% equities, they receive their withdrawal every month and increase it by inflation every year. However, the investments grow faster than the withdawals, so after a few years, they are only withdrawing 3% of their investments. This means they can give themselves a significant increase for the next year and future years.

However, if you start with a higher withdrawal, your chance of success is much lower. For example, if you start with a 5% withdrawal, your chance of success drops from 96% to 78%. Most people would consider a 22% chance of running out of money to be too high.

What can go wrong? There were 5 times in the last 146 years that a 4% withdrawal ran out of money:

– Four of the 5 were because there was very high inflation early and it stayed high a long time. They happened for people that retired in the late 1960s. Inflation jumped as high as 15% and stayed high for about 20 years. Their withdrawal became quite large to keep up with inflation and could not be sustained for 30 years.

– One of the 5 was because of the 1929 crash. The market fell by 80% in the first 4 years. There was deflation, so the withdrawal actually declined and the stock market bounced back the next 4 years, however, returns the first 15 years were barely positive. Too much capital had been withdrawn and it could not quite make the 30 years.

Note that dividends made no difference in safet. When inflation jumped to 15%, dividends stayed low. When the market fell 80%, most dividends were cancelled.

If you are mainly in equities and get a good long-term return, whether that return is capital gains or dividends makes no difference. It is long-term total return that protects you. That is why stocks have more reliably provided for a 30-year retirement than bonds – because the long-term return is so consistently higher.

Does that make it clear for you, Mark?

Ed

So, regarding the 4% rule, if you had a million dollars invested in safe dividend paying stocks at 4% which is doable at the moment, you would get $40,000 per year. It seems with this scenario you would die with the principle amount at least intact if not increased in value so why not take out a bit more. I just can’t get that the 4% would include dividends.

I must be a bit slow here.

Thanks…..Mark

Read your article. Very interesting and insightful. Thanks for all your hard work, it was certainly time well spent reading.

This information is magnificent. I understand and respect your clear-cut points. I am impressed with your writing style and how well you express your thoughts.

Hi Alex,

I studied how to make your retirement income reliable for 30-year retirements in-depth, but the answer may vary somewhat for shorter periods of time. YOu would really need a financial plan to get an answer for your specific situation.

I can give you some general insights.

At age 70 or 75, you should plan for your money to last till at least 97, since you or your spouse have a 25% chance of reaching 97 (and a 10% chance one of you will make it to age 100). That gives you a 22 or 27-year time horizon, which is not much less than 30.

For shorter time periods, you could increase your withdrawal rate, but not by much. If you look at the curve of how your portfolio is used up during retirement, it tends to start slowly and then fall off quickly once it hits a certain point.

Generally, you should only reduce your stock allocation when your retirement time horizon gets down to about 15 years or less. Stock returns after inflation are more consistent than bonds for periods of 20 years or more, but not for 10 years or less.

To see this, check out the graph titled “Stocks are more consistent than bonds after 20 years” on my article on the Retire Happy blog on this topic: “Can we retire now? Retirement rules of thumb” (https://edrempel.com/can-retire-now-ed-rempel-tests-retirement-income-rules-thumb/ ).

Does that answer your question, Alex?

Ed

Thank you for the study Ed. However I’m still confused about retiring later, say mayba at 70 or 75. What then? could we increase de WR reducing the stock allocation? by how much?

Thank you again,

Hi Mark,

Yes, the 4% should include any dividends. It is any amount withdrawn from your investments.

If you are getting 3% in dividends, then only take 1% extra from regular share sales.

Ed

I just noticed my mistake. Please insert 4% instead of the 5%.

Cheers

Hi Ed

Can you please explain the 4% rule a bit more. Does the 4% you remove every year include the dividends that are paid out? For example, if you have a million dollars in conservative dividend payers such as the banks and you figure you are getting about 3% return then can you also take out the 5% and the 3% effectively giving you an income of $70K per year?

Thanks a lot and keep up the great work. We do appreciate the effort!

Best Regards

Mark

[…] These rules of thumb are not supported by history. I studied 146 years of history of stocks, bonds and inflation and found these common rules of thumb are generally not You can read the study here: “How to Reliably Maximize Your Retirement Income – Is the “4% Rule” Safe?“ […]

Saved as a favorite, I love your web site!

Hi Sarah,

I’m glad my study was helpful for you. It is an “unconventional wisdom”, but the higher proportion of stocks you have, the higher chance that your retirement income will last at least 30 years. That is as long as you are within your risk tolerance and can stay with these investments through the next market crash or bear market.

In your position with a reasonably large portfolio of non-registered investments focused on equites, you have lots of tax-planning opportunities, as well, Sarah.

To answer your questions:

1. Yes, I studied taking CPP and/or OAS early or late and wrote 2 detailed, unique articles about it. I found that how you invest is the most important factor. Here they are: https://edrempel.com/start-cpp-early-real-life-examples/ and https://edrempel.com/delay-cpp-oas-age-70-complete-answer-real-life-examples/ .

2. Insighful question, Sarah. I usually get asked about shorter periods. The longer period of time, the more likely equities will give you a better return than bonds. Equities are unpredictable short-term, somewhat unpredictable mid-term, but have historically been quite reliabe long-term. Check out the graphs here to see it clearly: https://edrempel.com/can-confident-stock-market/ .

Welcome aboard a new subscriber, Sarah!

Ed

Dear Ed,

This is exactly what I was looking for! My house sale is closing next week and I’ve been wondering what to do with the money (we’ll be renting in the future). I was going to put 100% of it into cash or bonds which would bring my non-equity investments to 25% (we’re currently 100% in equities except for a generous emergency fund).

My husband will be retired as of January 2018 (I’m a Homemaker) and I don’t want either of us to ever have to go back to work. We also have two young dependents.

After reading this, I feel comfortable leaving “only” 15% in cash/bonds. I was concerned that putting most of it into equities was being “too greedy”. That we’ve worked so hard for this money and I was going to risk it trying to get a little more out of it. However, I realize now that it’s not about getting more but just keeping what we do have! I’ve always known that inflation was my biggest risk but didn’t know the best way to protect myself against it.

Two questions;

1. Have you written anything about taking CPP early, on time, later?

2. Would you change anything to what you’ve written above if the money had to last 50 years?

Looking forward to what you have to write in the future #newsubscriber

Regards, Sarah.

[…] his blog Unconventional Wisdom, Ed recently discussed his very interesting research* which reveals that if you want to withdraw 4% […]

Hi Ed, can you recommend some books or liturature on stock market history that you reference in the article. Thank you.

[…] How to Reliably Maximize Your Retirement Income – Is the “4% Rule” Safe? You want to retire soon. What is the best way to setup your retirement income to give you the maximum income that will reliably last the rest of your life? […]

Hi Ben,

Thanks for the kind words, Ben!

I spent a lot of time on this research and consider it to be groundbreaking.

Ed

Thanks Ed. Amazing article with such depth of research behind. Greatly appreciated.