RRSP Gross-up Strategy – Easily Contribute 40-70% More to Your RRSP

Wouldn’t it be great if you could save a lot more for your future without affecting your day-to-day cash flow?

One of the main things people learn when they first have a retirement plan done is that you need to invest more than you thought to have the future that you want. But with all the day-to-day expenses, it can be difficult to find the money to contribute as much as you would like to your RRSP.

The RRSP gross-up strategy is a simple strategy that can make a huge difference for you. It can enable you to easily contribute 40-70% more to your RRSP.

The strategy works if you already expect a tax refund. If you contribute monthly to your RRSP or have various tax deductions or credits, you probably expect a tax refund.

It is smart to gross-up every RRSP contribution you make.

RRSP Gross-up Strategy

You have 3 options with your tax refund:

- Spend it.

- Invest it.

- RRSP gross-up strategy.

Here is how the RRSP gross-up strategy works. Instead of investing your tax refund when you receive it in March, you contribute a gross-up amount in February that will be refunded by your tax refund.

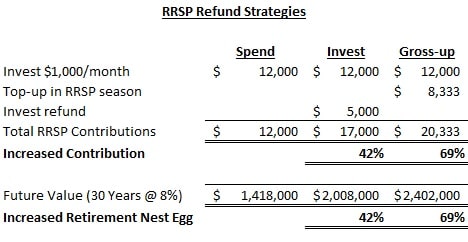

For example, if you have been contributing $1,000/month to your RRSP and are in a 40% tax bracket, you should already get a tax refund of about $5,000. Instead of investing the $5,000 refund when you receive it in March, you can invest $8,333 in February during RRSP season. This contribution increases your tax refund by $3,333, so you get a tax refund of $8,333 to pay for your contribution.

You can make the February contribution from cash or a credit line. You get it back a month or 2 later.

The formula is:

Expected tax refund / (1-Marginal tax rate) = Gross-up

$5,000 / (1-40%) = $8,333

With the RRSP gross-up strategy, you contribute $8,333 in February during RRSP season, instead of just your $5,000 tax refund in March. This is a 67% larger contribution.

We have just created an extra $3,333 in your RRSP and have not used any money from your day-to-day cash flow!

Benefits

This may be a simple strategy, but the benefits are huge, especially if you do this every year. Here is a comparison of your 3 refund options:

Over 30 years, this one little strategy can add $1 million to your retirement nest egg compared to spending your tax refund, and $400,000 compared to investing it. That’s huge!

Your tax refund:

Do you have plans for spending your tax refund? If not, then the RRSP gross-up strategy is perfect for you.

For many people, though, they want to use it for a trip, a home improvement, or to pay off a debt. The main reason they contribute to an RRSP is to get a tax refund.

Your tax refund may feel like free money, but it is not. It is a loan from the government. Remember, you have to pay the tax back when you withdraw it from your RRSP.

Most importantly, if you spend the refund, will you have enough to retire with the lifestyle you want?

People that have a retirement plan are much more likely to do an RRSP gross-up. One of the biggest benefits of having a retirement plan is that it changes your focus to thinking long term. You know how much you need to save to become financially independent, so you focus on how best to find the money to contribute.

It is much easier to use your tax refund effectively than to find an additional $8,333 ($700/month) from your monthly cash flow somehow – right?

“Never put dry pasta into your RRSP.”

Talbot Stevens advises to gross-up all your RRSP contributions in his book “The Smart Debt Coach”. He compares the smaller dry pasta to your after-tax cash and the larger cooked pasta to your before-tax dollars.

When you gross-up your contribution, you are putting your before-tax dollars into your RRSP.

“Never put dry pasta into your RRSP.” In other words, it is smart to gross-up all of your RRSP contributions every year.

Estimating accurately:

This is purely a tax strategy, so the only risk is estimating incorrectly. If you estimate a gross-up of $8,333, but then your tax refund is only $6,000, you are short the difference.

A good estimate includes looking at your total income, including taxable benefits, and all your tax deductions. Contributions to a group RRSP or pension do not give you a tax refund. Looking at the expected changes from your last year’s tax return can be very helpful.

You should also know how your income relates to the tax bracket. For example, you contribute $8,333, but only half is in the 40% tax bracket and the other half pushes you down to the 30% tax bracket. Your tax rate on the $8,333 is lower, so you should estimate a lower gross-up.

Your best estimate may be from your financial planner, if he prepares your tax returns, understands tax and knows what has changed in your life.

Summary

The RRSP gross-up strategy is a simple way to find 40% to 70% more to contribute to your RRSP without affecting your day-to-day cash flow.

With all your day-to-day expenses, it can be hard to find money to make a proper RRSP contribution. Using your tax refund in this highly effective way can give you a much more comfortable retirement.

There is a little effort involved in estimating the gross-up accurately. Your financial planner may be able to help you.

One sharp client pointed out to me that the benefit from this one strategy is more than the entire cost of a financial planner over your lifetime.

People that have a retirement plan are much more likely to do an RRSP gross-up. A retirement plan changes your focus to thinking long term. You know how much you need to save to have the life that you want, so you focus on how to find it.

“Never put dry pasta into your RRSP.” It is smart to gross-up all of your RRSP contributions every year.

The RRSP gross-up strategy can make it much easier to achieve financial independence and live the life you want.

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

Hi David,

The “RRSP Gross-up” strategy can still apply to you, depending on how you look at your cash flow and your plan.

For example, if you have $26,000 RRSP room and maximize it while you are in a 40% marginal tax bracket, you are using only $15,600 of your own cash. Think of this as an investment of $15,600 plus a gross-up, not as an investment of $26,000.

If you are reinvesting your entire tax refund, you are in essence doing it already. If you invested $15,600 into RRSP from your cash and put the rest into TFSA, and then did the RRSP Gross-up in February every year, you would essentially be in the same position as you are now.

The only difference is that if you know what your tax refund will be, you can borrow it sooner to invest, such as in February or by having less tax withheld from your pay cheque all year.

The goal is to invest the maximum you can within your available cash flow.

Ed

Great article! Does this apply to someone who doesn’t have additional RRSP room? I max out my RRSP every year and typically use the tax refund to max out my TFSA. I can’t see how I would use this “gross-up” strategy if I have maxed out contributions by Feb 28 already with regular pay-cheque deductions. Am I missing something?

Hello! Cool post, amazing!!!

Hi David,

To answer your question, not usually, but sometimes.

The general guidelines are:

– If you can max your RRSPs through your work life all at your current tax bracket, then don’t contribute so much that it pushes you to a lower tax bracket.

– However, if the lower bracket now is still the same or higher than your retirement bracket, it may still be worth contributing.

You should look at more than the current year for this question. I have seen quite a few cases with people that have a very large RRSP room. They have a high income now and will retire at a lower bracket, so it is worth contributing a lot. They will have to contribute enough to get into the lower tax bracket to max their RRSP by retirement.

Do these general comments address your specific issue, David?

Ed

Great point, MH. That is exactly what I do for my clients.

Calculating a gross-up based on your marginal tax bracket is good. Much better is knowing your entire tax situation and what refund you are expecting taking into account all your tax deductions and credits.

It’s a big advantage for an advisor to also do tax returns.

Ed

Is still worth doing this if it would bump you into a lower Marginal Tax rate?

If you do your own taxes you can rough them into the tax software mid February to figure out your approximate refund, then make your gross-up RRSP contribution before the end of February. That way you can “gross-up” all of your other deductions (health, donations etc) for an even bigger bang for your buck.

Hi David,

Good idea. Good use of the refund.

Are you thinking this way because your RRSP is already maxed?

Whether your idea or the RRSP gross-up strategy is better in your case depends on which is better for you: TFSA or RRSP? – The Right Answer for You

Ed

Hi Ed,

I am around the 50% tax bracket. What about using all of the RRSP generated refund to invest in my TFSA (not yet maxed). For example $40K in RRSP should generate close to $20K in refund for investment in TFSA.

Thoughts?

David