TFSA vs RRSP – Clawbacks & Income Tax on Seniors

“The future ain’t what it used to be.” – Yogi Berra

Tax Free Savings Accounts (TFSA’s) were announced in the 2009 federal budget. At first, it seemed they would be not nearly as useful as RRSP’s since there would be no tax refunds for contributing. However, we are starting to analyze TFSA’s and it seems they beat RRSP’s most of the time. Credit Stephen Harper for implementing what may eventually become the most effective retirement savings vehicle for many (perhaps most?) Canadians, as well as a very useful tax saving tool.

To understand why TFSA’s will beat RRSP’s as a retirement savings vehicle for many Canadians, we first need to understand income tax on seniors.

TFSA’s appear to be almost exactly the same as RRSP’s, except without the tax refund on contributing and tax on withdrawals. Therefore, to determine whether TFSA’s or RRSP’s are better for you depends mainly on your tax bracket when contributing (during your career) vs. your tax bracket when withdrawing in retirement.

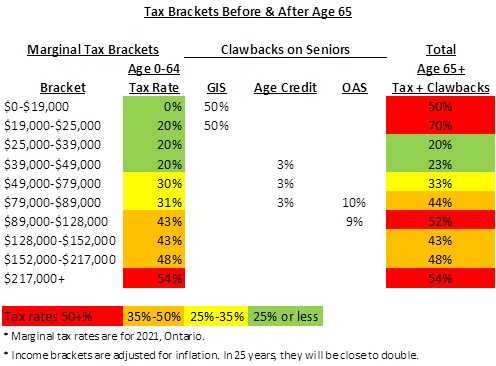

A common part of retirement planning and one of the main benefits of RRSP’s includes the assumption that most Canadians will be at lower income tax rates after they retire than they are during their working career. This may sound logical, but it is often not true. In fact, on average, when you include clawbacks on several programs for seniors, income tax rates on seniors are almost 50% higher than on adults under 65!

Our Canadian outlook of always looking after the have-nots has led to quite a few benefits for seniors that are clawed back based on income. The idea is that those with a lot of income do not need the tax relief. The end effect, however, is very high rates of income tax on seniors.

The 3 main Clawbacks that affect seniors are clawbacks on the Guaranteed Income Supplement (GIS), the age credit and on Old Age Security (OAS). GIS is a supplement of up to $14,024 of tax-free income paid to seniors with an income under $18,984 (single). Essentially, for every $2 of taxable income, the GIS is reduced by $1. The age credit is a tax credit of $7,637 that is reduced by 15% for any dollar of income above $38,508. Maximum OAS is a taxable income of $7,518 that is also reduced by 15% for incomes above $79,054. (The OAS clawback is not quite as bad, since we at least get credit for the income tax we would have paid on the OAS.)

There are also clawbacks that apply to adults under 65, such as employment insurance and the child tax benefit, but none of them apply to everyone at any given tax bracket.

When you add the clawbacks that affect seniors, here are the approximate marginal tax brackets in Ontario for adults under 65 vs. seniors. The marginal tax rates apply to everyone, while the tax rates with clawbacks apply specifically to anyone 65 and over.

The lowest tax rates for seniors are on capital gains. This is because the clawbacks are on taxable income – which is only 50% of capital gains but is 145% of dividends. For example, for seniors with no other income, the 50% GIS clawback is only a 25% clawback on capital gains income, but is a 73% clawback on dividend income.

Is there logic to these tax rates? Why should dividends have the lowest tax rate for adults under 65 who are building retirement assets, while capital gains have the lowest tax rate for seniors trying to get an income from their investments? It sounds backwards, but there is some logic when you understand the way CRA structures tax on investment income.

Many Canadians, if they have saved a good nest egg or have a decent pension, may be retiring on incomes of 50-70% of their working incomes. For example, an average Canadian may earn $50-60,000/year during their career, which would put them into a marginal tax rate of 31%. When they retire on say $30-40,000, they would be at a marginal tax bracket of 37% – which is higher than during their working career.

Note that many seniors will be at lower tax brackets in retirement, however. This is because most Canadians, if they have only modest savings for retirement, will likely be retiring with incomes of only $25-50,000/year, which would put them in the lower 20% tax bracket.

All of these tax brackets are adjusted for inflation each year. This means that the income amounts for each bracket will be close to double the figures in the above chart in 25 years.

What does all this mean for the usefulness of Tax-Free Savings Accounts (TFSA’s)? That will be the subject of our next article.

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

A most informative article