7 Best Ideas to Optimize the Smith Manoeuvre (Canadian Financial Summit 2024)

With its quirky name, the Smith Manoeuvre might sound unconventional, but it’s a strategy that truly works—when done by the right people, in the right way, over the long term.

From crafting over 1,000 professional Financial Plans, I’ve seen firsthand how the Smith Manoeuvre can transform your finances, helping Canadians use their home equity to invest for their future without impacting their cash flow.

When included as part of a comprehensive financial plan, this strategy can empower you to achieve the life you’ve always envisioned.

But optimizing the Smith Manoeuvre requires more than just the basics—it’s about mastering the practical details and understanding how to maximize its benefits.

In my latest YouTube video, podcast episode and blog post you’ll learn:

- What is the right reason to do the Smith Manoeuvre?

- How do you know if you are the right person for the Smith Manoeuvre?

- What is the right mortgage?

- How can you keep it 100% tax deductible?

- Which of the 8 Smith Manoeuvre strategies is right for you?

- Why is it critical that the Smith Manoeuvre is a long-term strategy?

- What is the right mindset to minimize the risk & maximize the benefits?

1. What Is the Right Reason to Do the Smith Manoeuvre?

Many misconceptions surround the Smith Manoeuvre’s primary benefits. Here’s what you need to know:

- It’s not about tax deductions. While tax savings are a part of the benefit, they only account for 15-20% of the overall value.

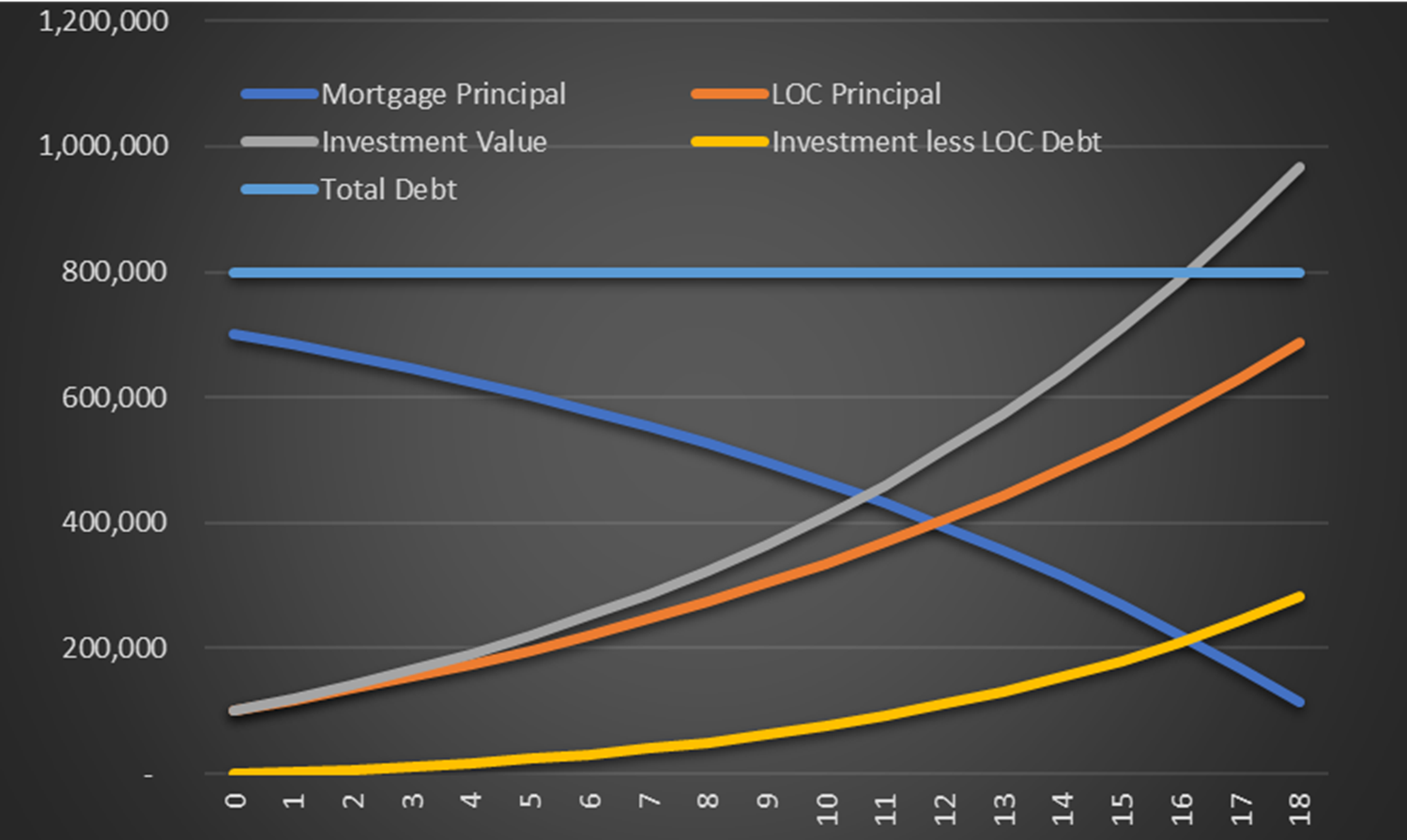

- The real advantage lies in long-term growth. The primary benefit is the compounded, after-tax growth of investments minus the after-tax cost of borrowing. For most people, the expected net benefit after 25 years is equivalent to the current value of their home.

- It’s not about eliminating debt. Some people mistakenly think the Smith Manoeuvre is a strategy to pay off their mortgage faster. That’s not the case. The focus is on investing for retirement without dipping into your cash flow.

- It’s a bridge to retirement security. Retiring comfortably is challenging for many, and the Smith Manoeuvre often fills the gap by enabling additional investments alongside RRSPs and TFSAs.

- Make efficient use of your home equity. Don’t let your home equity sit idle. One client, a widower, referred to unutilized equity as “fun I didn’t have.”

- Integrate it into your financial plan. The Smith Manoeuvre works best as part of a comprehensive financial plan designed to balance living for today with investing for your future.

2. How Do You Know If You Are the Right Person for the Smith Manoeuvre?

The Smith Manoeuvre isn’t for everyone. It requires specific traits and commitments:

- Risk tolerance. You must be able to stick with your investments even during downturns. Successful investors have the discipline to do nothing when markets decline.

- Long-term commitment. The strategy only works if you’re in it for the long haul—ideally 20 years or more. If you’re looking for a short-term fix, this isn’t the right approach. Better is for life – or as long as you own your home.

- Story of caution. A client once wanted to try the Smith Manoeuvre for just one year. If that’s your mindset, don’t even start.

3. What Is the Right Mortgage?

The foundation of the Smith Manoeuvre is a readvanceable mortgage (mortgage linked with a credit line), but not all are created equal:

- Features to look for:

- Overall limit of 80% of the appraised value at the start. (declines with new OSFI rules)

- Automatic and immediate readvancing.

- Invest from credit line – Or need a separate Smith Manoeuvre chequing

- Multiple credit lines available.

- Multiple mortgages available – Readvance into one credit line or multiple.

- Invest from $1 (No minimum)

- No minimum investment amount.

- No monthly fees.

- Competitive interest rates.

- 10 readvanceable mortgages. See my post with pros & cons of each, and ratings.

- Avoid suboptimal options. For example, Manulife’s readvanceable product only starts at 65% of the appraised value, has higher interest rates, and may charge monthly fees.

- Expert implementation matters. Many mortgage brokers and bank representatives don’t fully understand the Smith Manoeuvre’s intricacies or tax rules. Work with financial planners experienced in implementing this strategy.

4. How Can You Keep It 100% Tax-Deductible?

Tax-deductibility is a key element of the Smith Manoeuvre. Smith Manoeuvre is not complex, but is easy to mess up. Here’s how to ensure you stay on track:

- Choose the right investments. Invest in assets with income potential (e.g., equities) that don’t restrict dividends or interest payments. CRA’s folio S3-F6-C1 outlines interest deductibility rules.

- Keep accounts separate. Deductible and non-deductible credit lines, mortgages, and investments should never be commingled. Mixing them up can cost you tax deductions.

- Interest capitalization done right. Borrow only what you need for investments or to pay interest on investment loans. Missteps, like spending the full available credit, can lead to trouble.

- Be audit-ready. Keep detailed records. In the event of a CRA audit, you must prove your figures. We handle dozens of CRA pre-assessments annually, often with 60-page submissions.

- Collaborate with a CPA. Work with an accountant who understands the Smith Manoeuvre and will represent you with the CRA if necessary.

5. Which of the 8 Smith Manoeuvre Strategies Is Right for You?

The Smith Manoeuvre offers several variations to suit different needs. Here are the main options (details can be found on my blog):

- Plain Jane

- Debt Swap (Singleton Shuffle / Flintstone Flip) Make some of your mortgage tax-deductible in one day.

- Top-Up. Plane Jane plus lump sum.

- Triple Top-Up Plane Jane plus lump sum plus 3:1 investment loan.

- Debt Miracle. One couple used this strategy to combine many debts and start to invest $2,500/month with no change in cash flow.

- Smith Manoeuvre with Dividends. Less tax-efficient; need to earn 1%/year higher return.

- Smith/Snyder. Effective for retirement cash flow but has tax challenges. Story of mortgage broker firm heavily marketing Smith Manoeuvre with T-8 funds.

- Rempel Maximum. The ultimate growth-focused strategy.

6. Why Is It Critical That the Smith Manoeuvre Is a Long-Term Strategy?

Long-term thinking is essential to success:

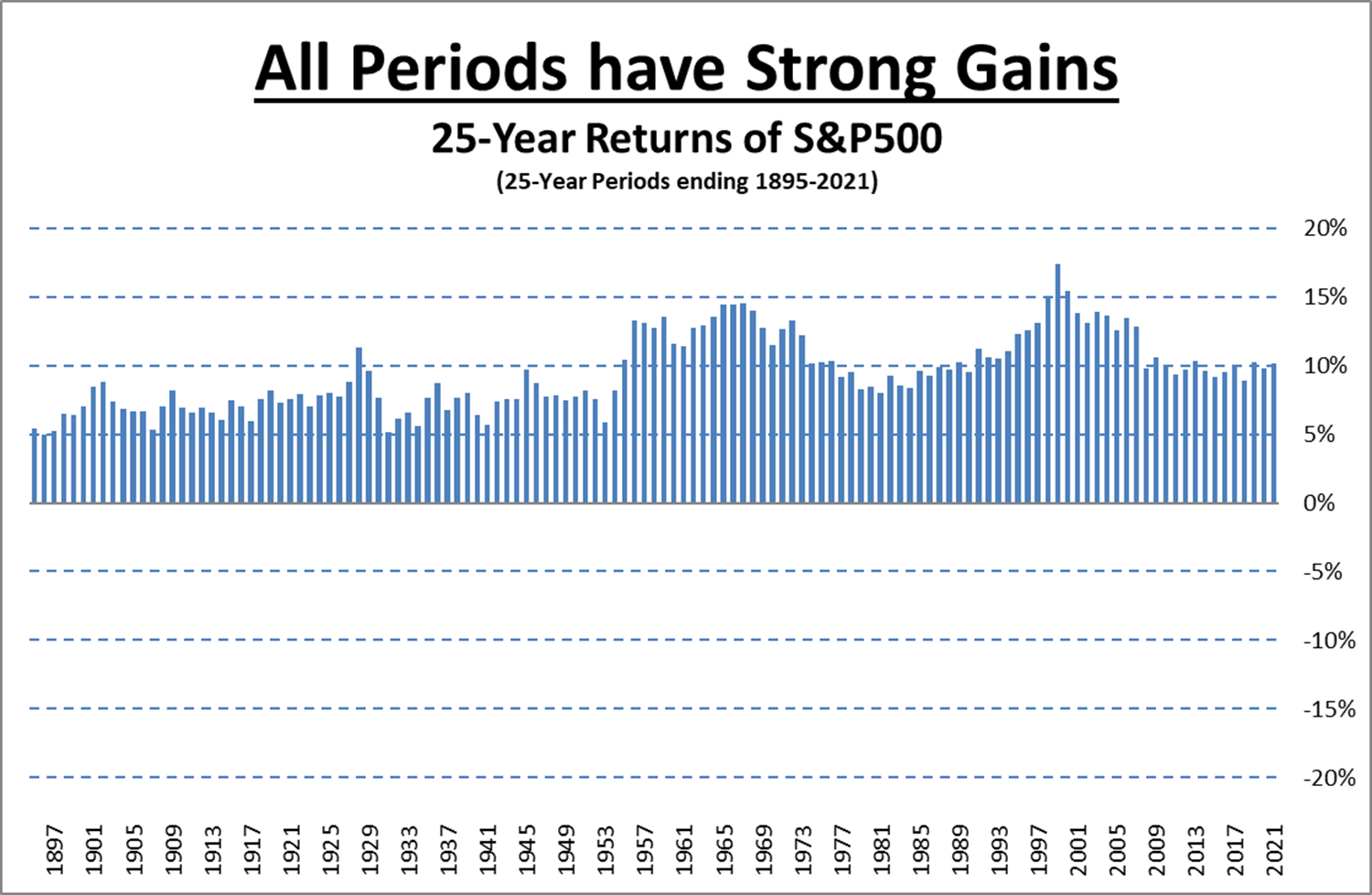

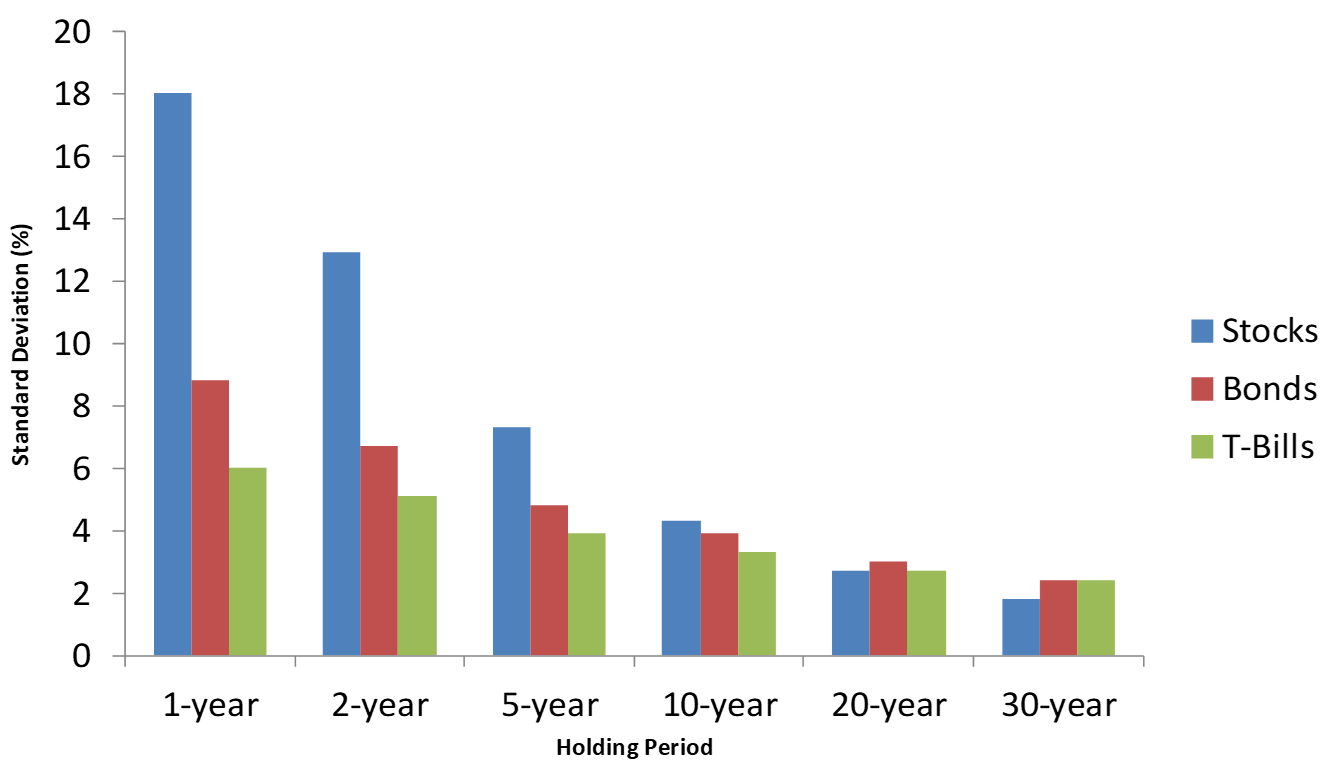

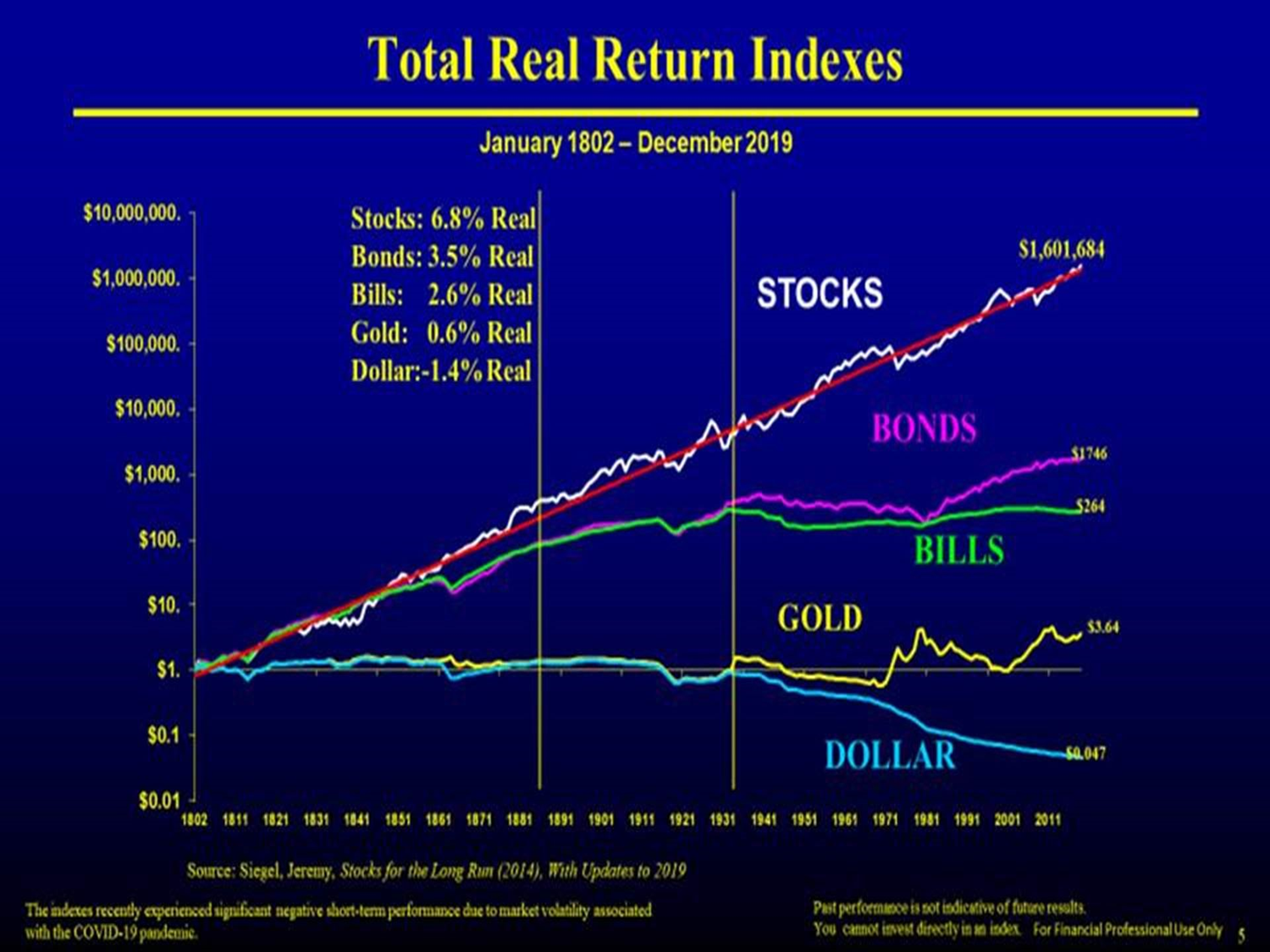

- Market reliability over time. While the stock market / equities are unpredictable in the short term, they become surprisingly dependable over 20+ years. Historical data shows the stock market has delivered returns 7-17 times higher after 25 years.

- Stock market is more predictable after inflation than bonds after 20 years or more.

- The power of compounding. Stocks rise in the long term because corporate profits grow. This makes equities the most effective retirement investment for most people.

7. What Is the Right Mindset to Minimize Risk and Maximize Benefits?

Your mindset determines your success:

- Think long-term. Commit to the strategy for at least 20 years. Not a 1-year trial.

- Stay the course. Be prepared to hold your investments through market downturns. Confidence in your investments is key.

- Tax efficiency matters. Choose buy-and-hold investments that minimize tax impacts.

- Learn to tolerate risk. Risk tolerance is a skill that improves over time, much like adjusting to turbulence during air travel. You get used to it. Biggest mistake would be getting off. Air travel is still the most effective way to get to your destination.

- Always have a plan. Your financial plan acts as the GPS for your financial life, helping you stay focused on long-term goals.

- Work with experts. Collaborate with experienced financial planners and tax accountants to minimize risks and maximize benefits.

- Your Financial Plan is the GPS for your life. As the leading expert on the Smith Manoeuvre in Canada (and tax accountant), I’m the only source for all 8 Smith Manoeuvre strategies.

The Smith Manoeuvre is a powerful tool when implemented thoughtfully and as part of a comprehensive financial plan. With the right guidance, it can transform your home equity into a reliable vehicle for retirement security and long-term wealth growth.

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

Hi Ed,

With the new OSFI rules, would you say it is better to invest the yearly investment loan interest refund to RRSP (high tax bracket) now than to use it to pay down mortgage? I understand that priority for extra cash now for people in high tax bracket is RRSP then TFSA then SM. Does this also apply with the SM refund?

Hi Ed, great content. I own a duplex and live in one of the units. I am an employee and also entrepreneur. Is the smith manoeuvre possible in my situation?