How to Easily Outperform Financial Advisors, Robo-Advisors & Index Investors (Canadian Financial Summit 2024)

Why do so many Canadians struggle to achieve financial freedom, even with a solid financial plan?

Why do they retire with less than they hoped for, despite diligently saving and investing?

The answer often boils down to two things: suboptimal investments and a misguided focus on risk.

In my latest YouTube video, podcast episode, and blog post we’ll uncover why good investment performance is essential for your financial success and show you how to take control of your portfolio.

We’ll also address common misconceptions about risk in the investment industry and uncover the secrets to thinking like a successful investor.

You’ll learn:

- Why is good performance important for your life?

- What rate of return do you need to become financially independent?

- What are the 4 performance drags that reduce investment returns?

- What is the Asset Allocation Loss Ratio (AALR)?

- Why is it easy to outperform financial advisors?

- What is wrong with the investment industry definition of “risk”?

- Why is it easy to outperform robo-advisors?

- Why is it easy to outperform index investors?

- How can you learn to think properly about investing?

- What are the secrets to outperforming?

- What is the right mindset to minimize the risk & maximize the benefits?

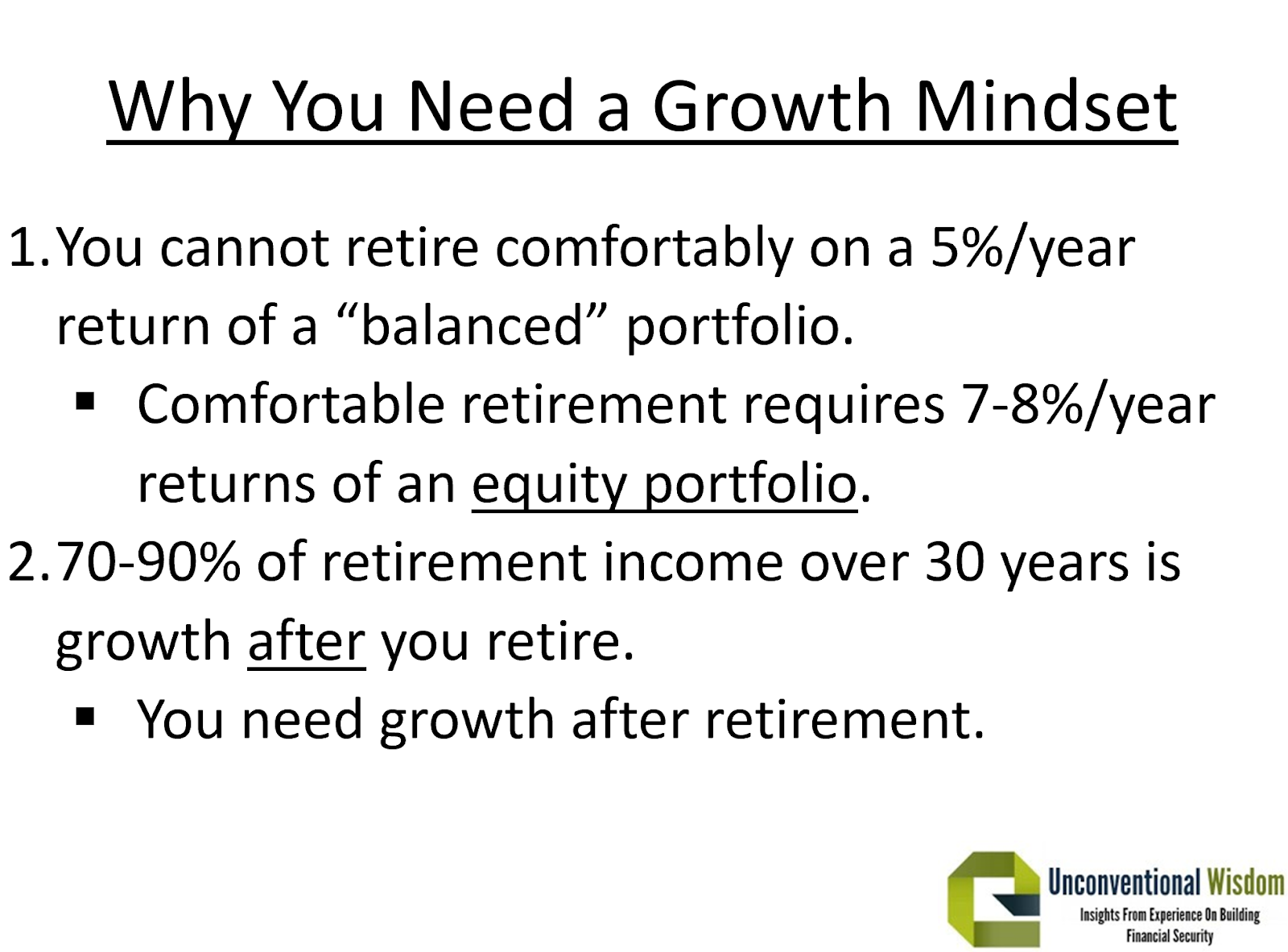

Why Is Good Performance Important for Your Life?

Good investment performance is the cornerstone of achieving financial freedom. From our experience writing over a thousand financial plans, one thing is clear: without a high-equity portfolio delivering strong returns, most retirement plans are nearly impossible to achieve.

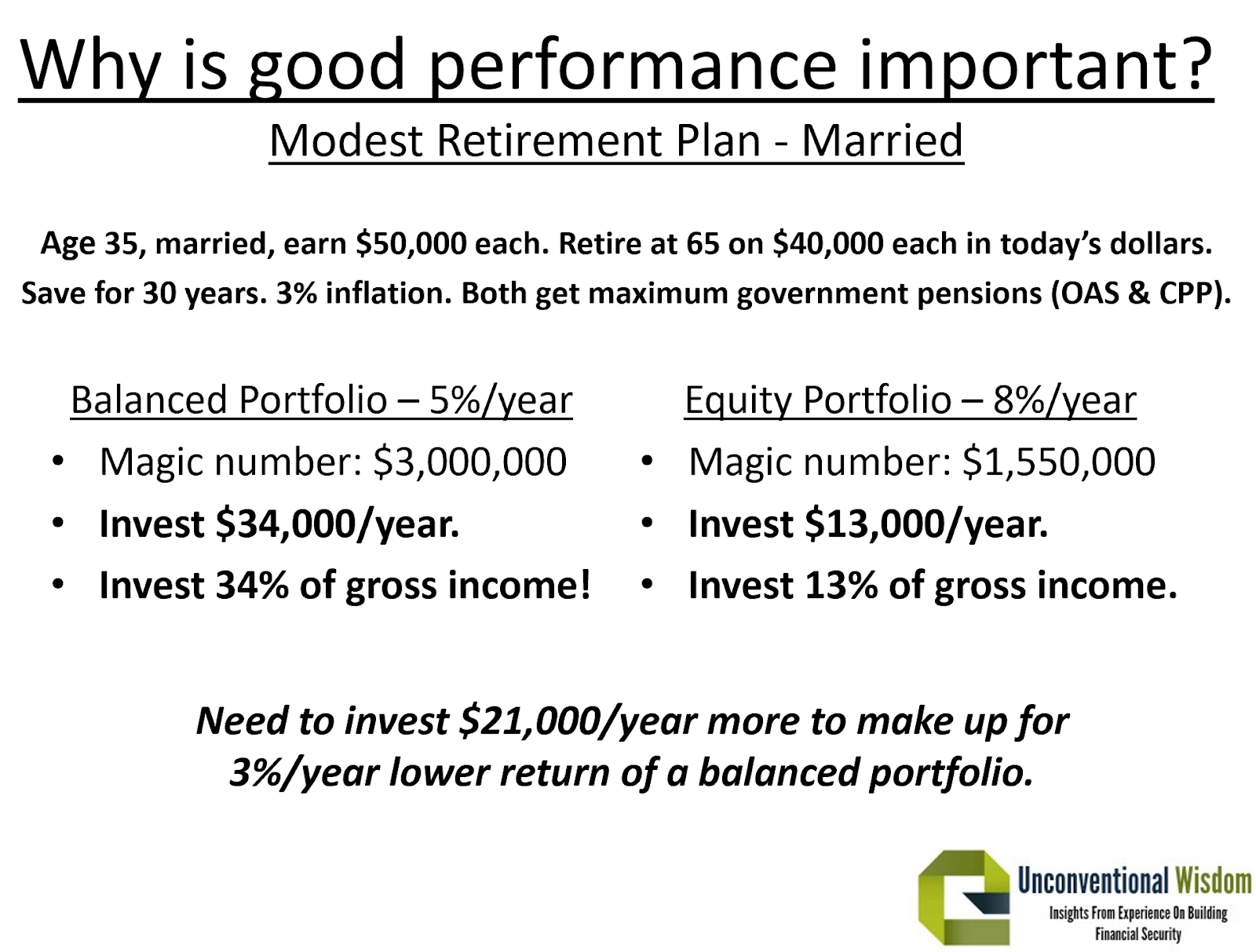

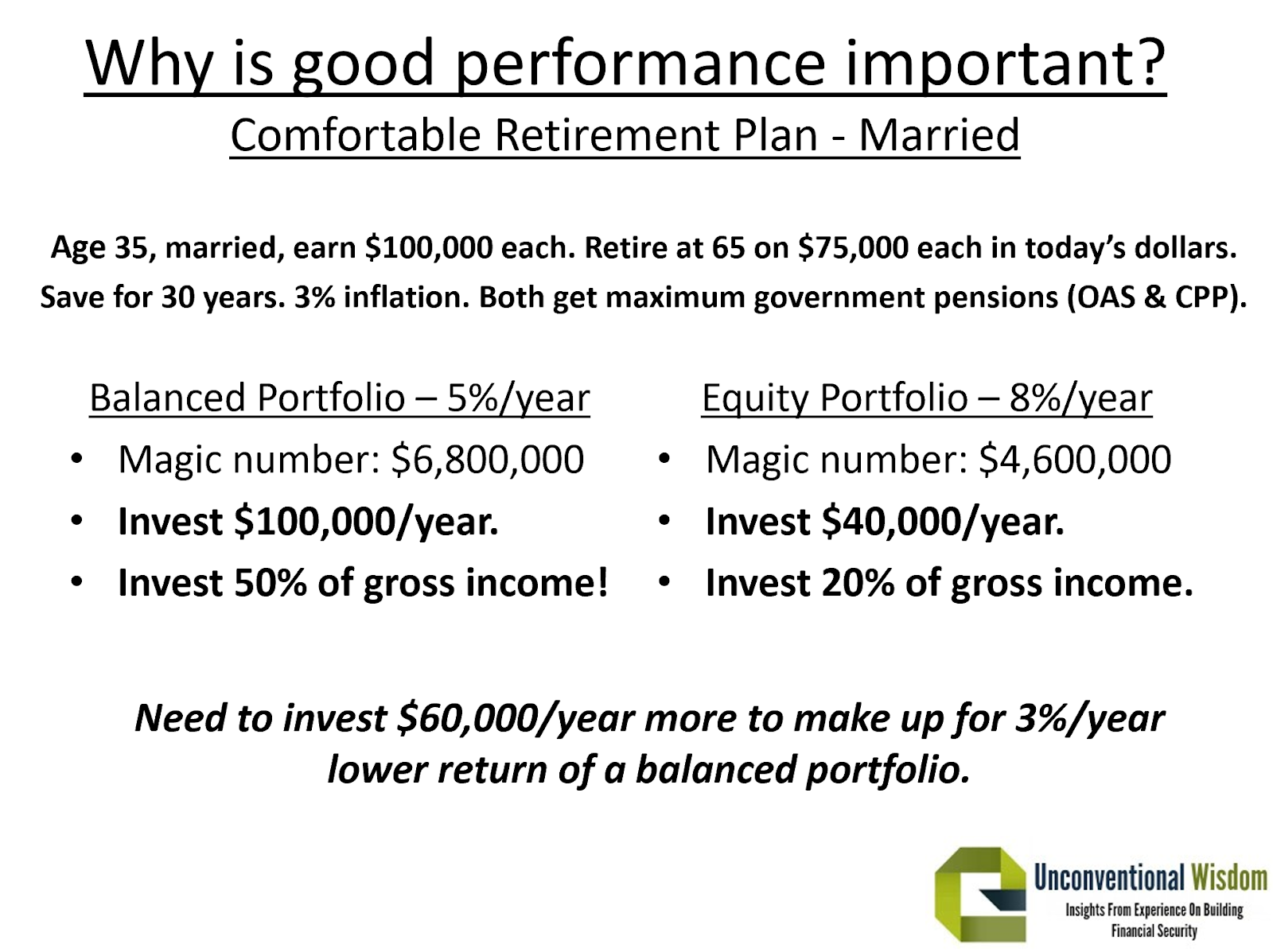

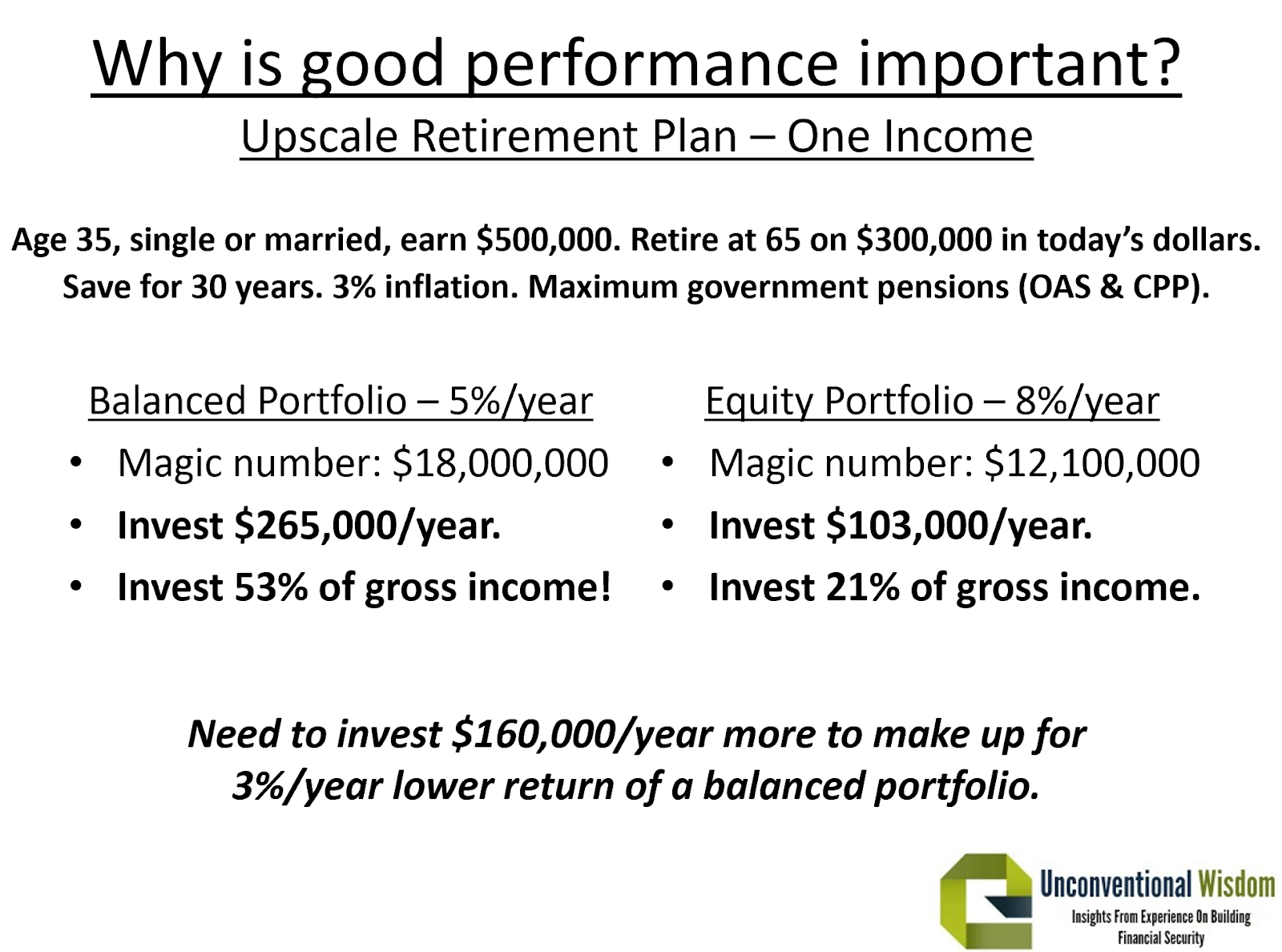

For example, with a balanced portfolio earning 5% annually, you might need to save an overwhelming 34% of your income just to retire comfortably. However, with an equity-focused portfolio earning 8%, that figure drops to a manageable 13%.

Examples:

- Modest Scenario: A couple earning $50,000 each ($100,000 total) wants to retire on $80,000 a year. With a balanced portfolio earning 5% annually, they’d need to save $34,000 annually—34% of their income. That’s unrealistic. But with an 8% return from an equity portfolio, they’d only need to save $13,000—just 13% of their income, a much more attainable goal.

- Upscale Scenario: A couple earning $200,000 combined, aiming to retire on $150,000 a year, would need to save $100,000 annually—half their income—if earning 5%. With 8%, they’d need just 20% of their income, which is far more feasible.

The bottom line: strong returns are essential. A fear-based mindset favoring low-risk, low-return investments often leads to failure in achieving retirement goals. High-equity portfolios, though requiring a long-term view, are the key to making financial freedom possible.

What Rate of Return Do You Need to Become Financially Independent?

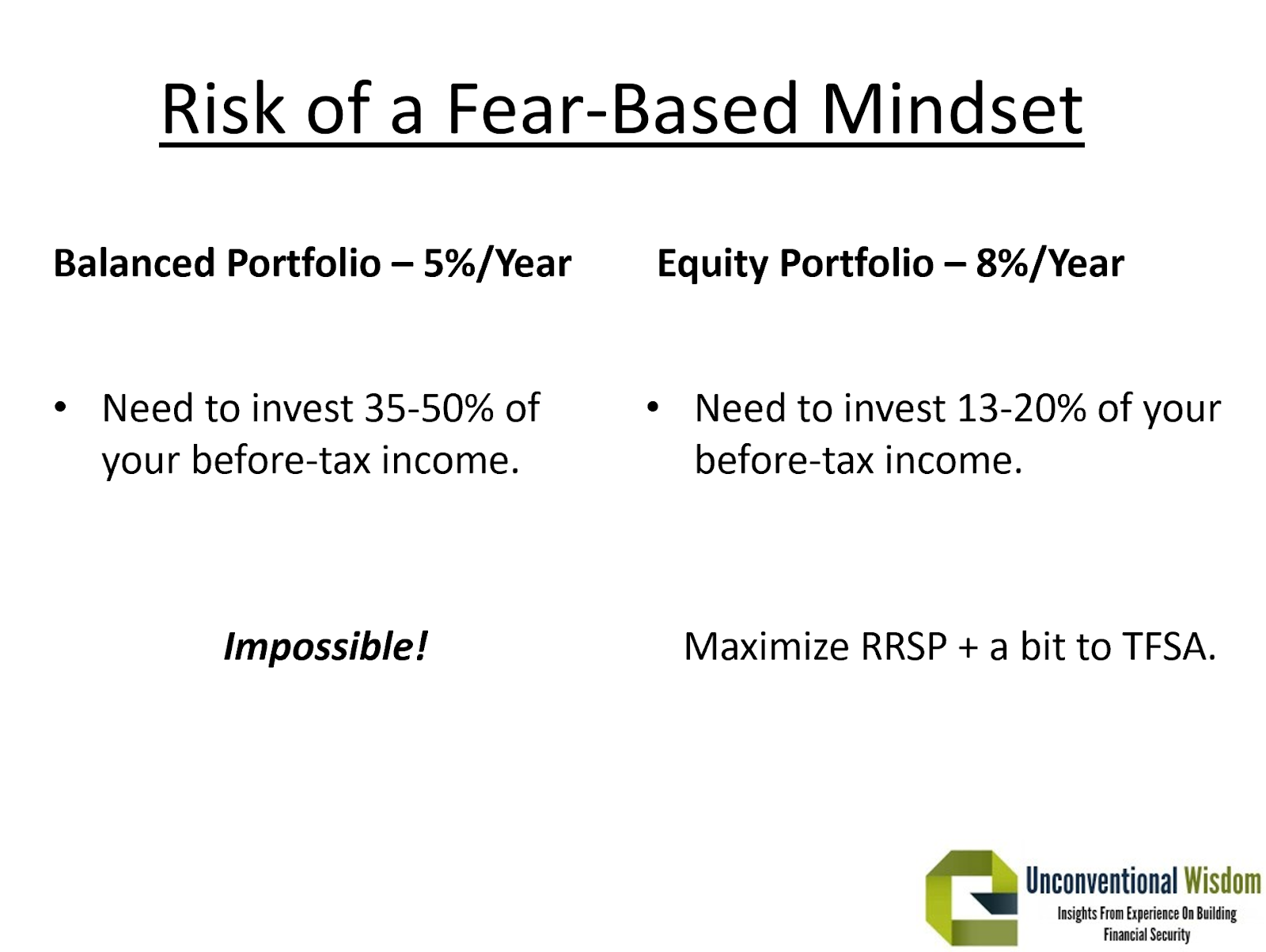

Reaching financial independence hinges on achieving the right rate of return. If your investments grow at 5% annually, you could end up needing to save an impossible 35–50% of your gross income to retire comfortably.

With an 8% return, that figure becomes 13–20%, a target that’s challenging but doable.

Even after retirement, growth remains critical—up to 90% of your retirement income could come from your portfolio’s returns. Without a solid plan and the right investment strategy, you may find yourself stuck in the “balanced portfolio trap,” where modest returns make your retirement goals unattainable. Focus on growth to secure your financial independence and your future.

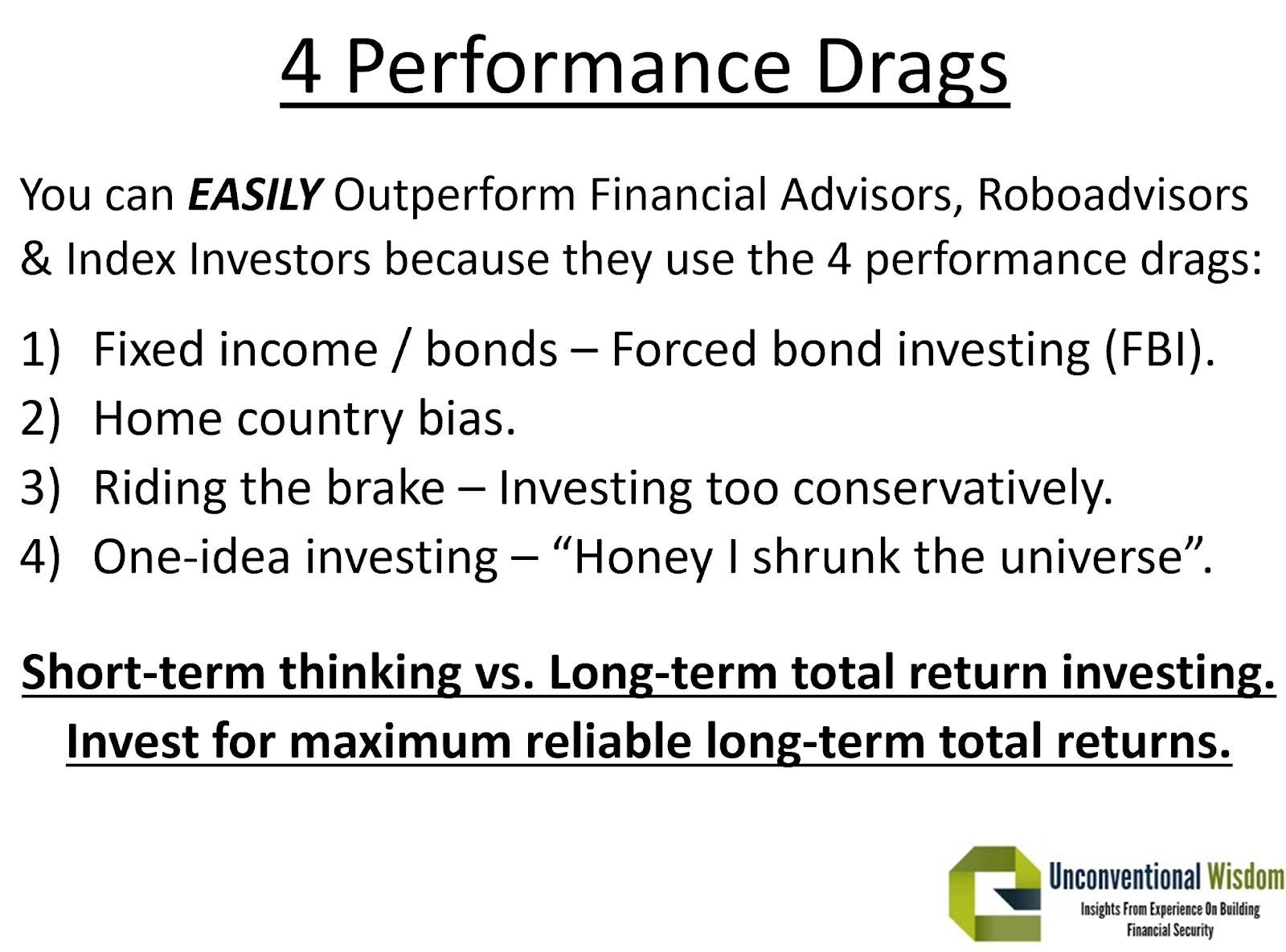

What Are the 4 Performance Drags That Reduce Investment Returns?

Many investors experience subpar returns due to common pitfalls that drag down performance. These drags are often built into the strategies used by financial advisors, robo-advisors, and even index investors. Here’s an overview of the four main drags:

- Fixed Income (Bonds)

Bonds are often marketed as a “safe” investment, but they come with a hidden cost: low returns. Forced bond investing (“FBI”) is a significant drag because bonds typically underperform equities over the long term. While they may appear stable, their failure to outpace inflation can erode your purchasing power over time. - Home Country Bias

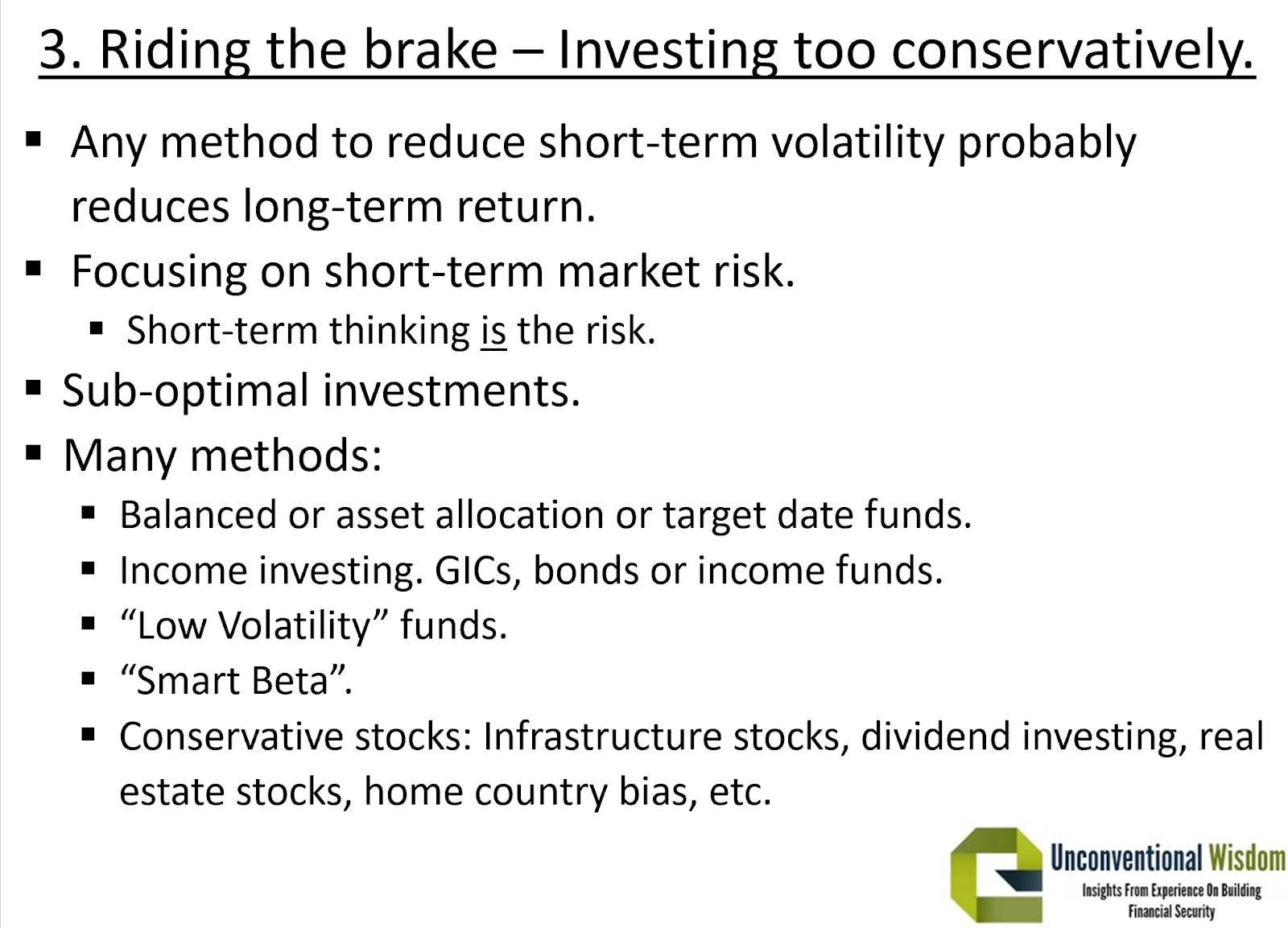

This occurs when investors overallocate to their domestic market, ignoring global diversification. Relying too heavily on one country limits opportunities and increases risk, especially if the local market underperforms. - Riding the Brake

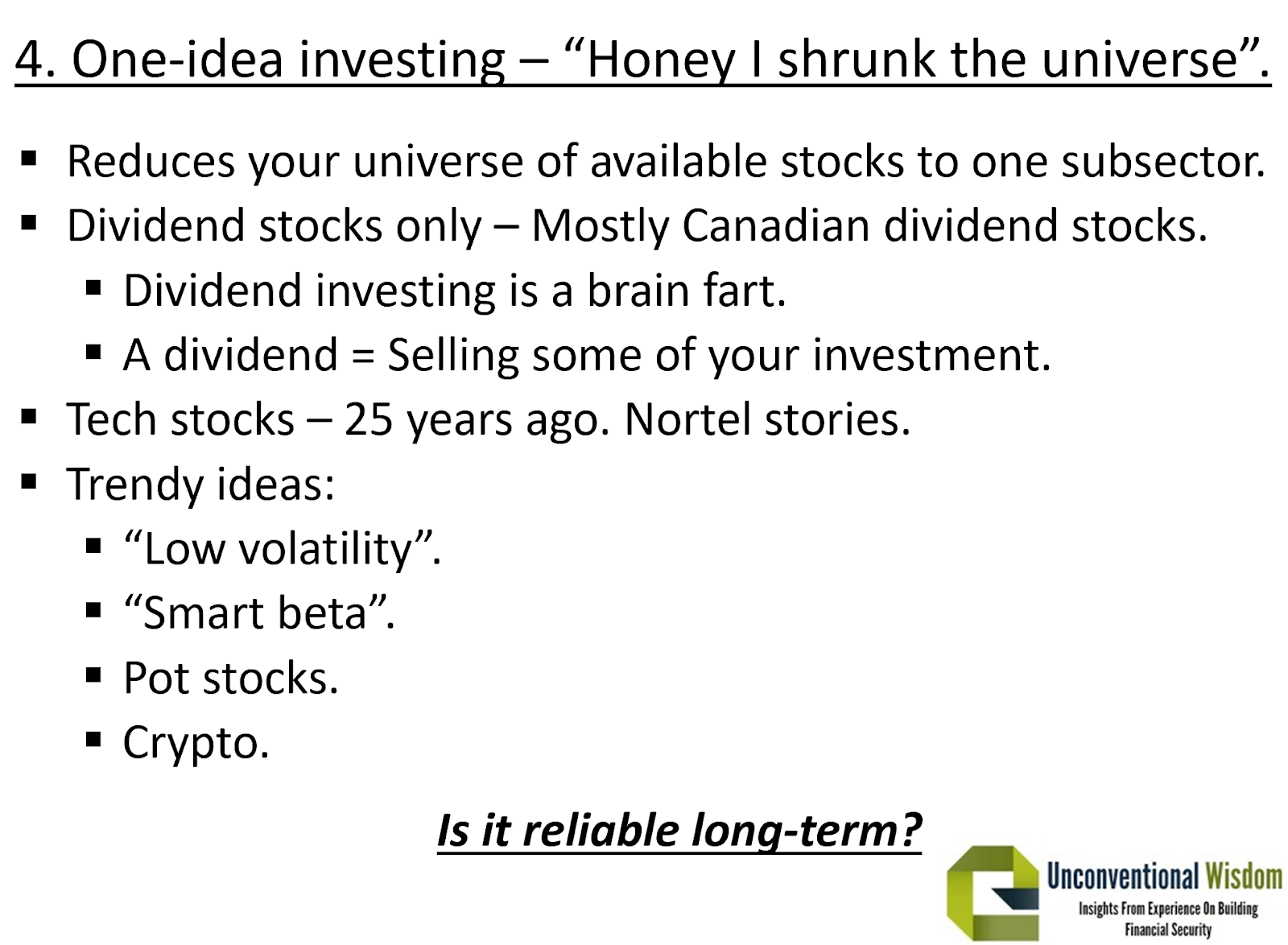

This refers to overly conservative strategies, like holding excess cash or investing in low-volatility assets. While it may reduce short-term fluctuations, it hampers long-term growth, making it difficult to build wealth or sustain a comfortable retirement. - One-Idea Investing

Narrowing your investment universe to a single concept or asset class—no matter how promising it seems—limits diversification and increases vulnerability. Successful investing requires a broad, well-balanced approach.

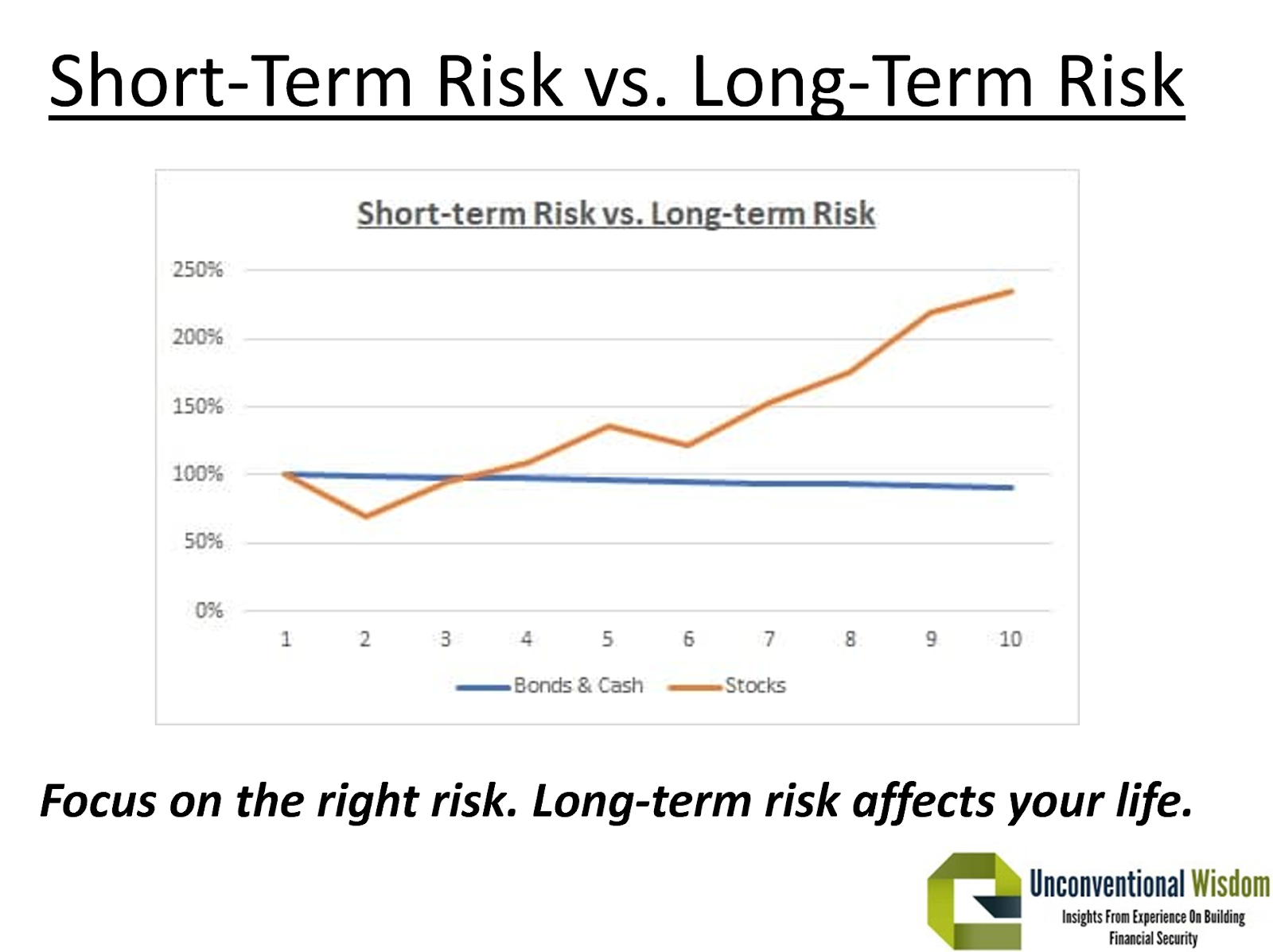

The Bottom Line: Long-Term Thinking Wins

Performance drags are rooted in short-term thinking: avoiding market volatility at the cost of long-term returns. Instead, focus on maximum reliable long-term total returns. Equities have consistently delivered the most dependable growth over time, despite short-term ups and downs.

To illustrate: Bonds may feel “safe” due to their stability, but they carry long-term risks, like failing to keep up with inflation. While equities experience volatility, their long-term reliability far outweighs these short-term risks. The key is to shift your mindset from avoiding temporary losses to securing sustained growth, ensuring your investments align with your long-term goals.

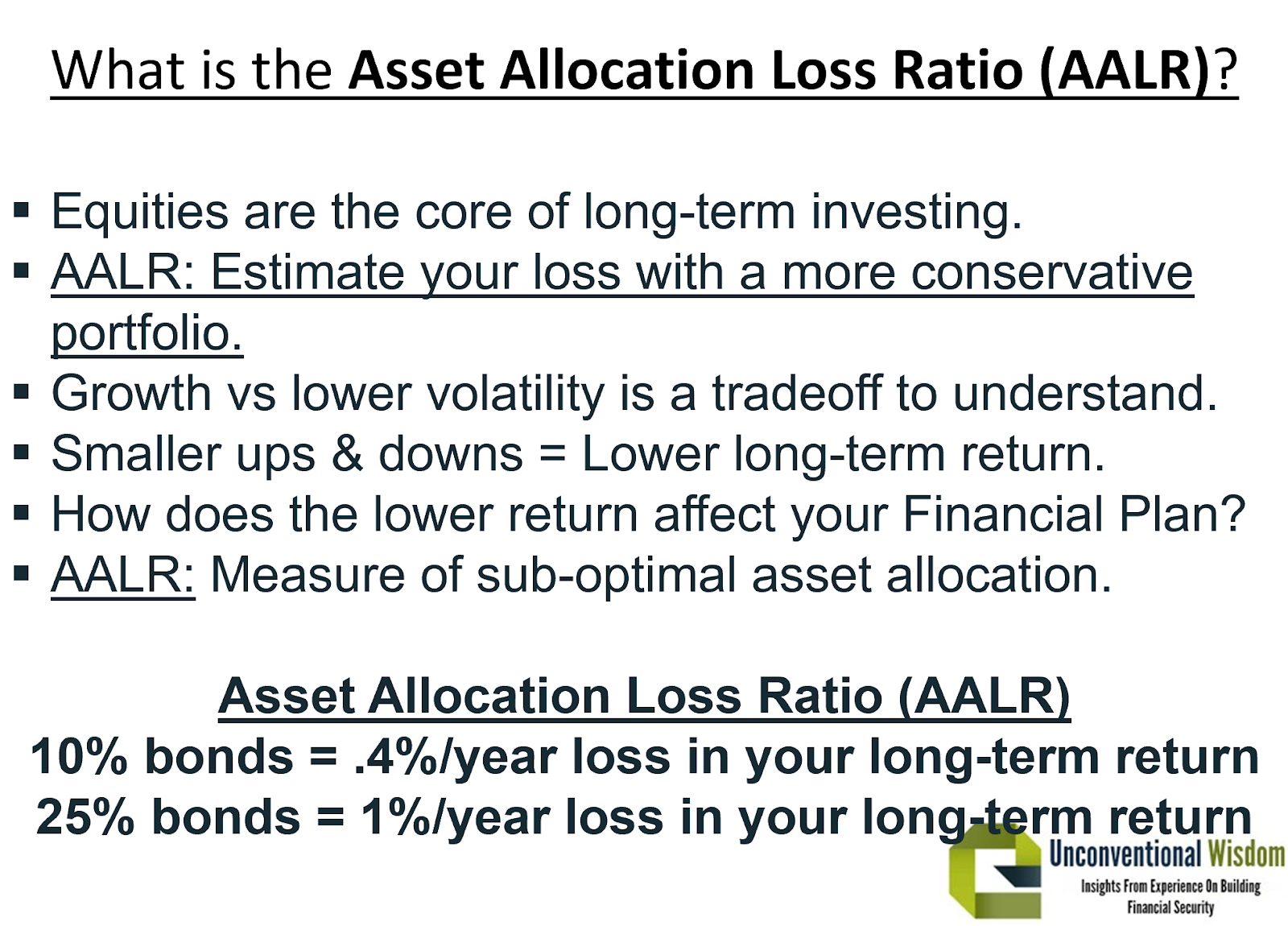

What is the Asset Allocation Loss Ratio (AALR)?

The Asset Allocation Loss Ratio (AALR) is a concept I developed to quantify the trade-off between long-term growth and lower portfolio volatility. It helps investors understand the cost of adopting a more conservative portfolio. For example, equities are the backbone of long-term investing due to their reliability and strong returns over time. However, choosing a conservative allocation, such as including bonds or fixed income, reduces portfolio volatility but also significantly lowers potential growth.

AALR estimates the impact of this reduced growth. For every 10% allocation to bonds, you can expect a decrease of approximately 0.4% to 0.5% in annual returns over the long term. For example, having 25% in bonds might result in losing 1% per year in returns. Over decades, this loss compounds, potentially affecting your financial goals, such as delaying retirement or reducing your lifestyle in retirement. AALR emphasizes how critical it is to align your asset allocation with your long-term objectives rather than simply aiming for lower volatility.

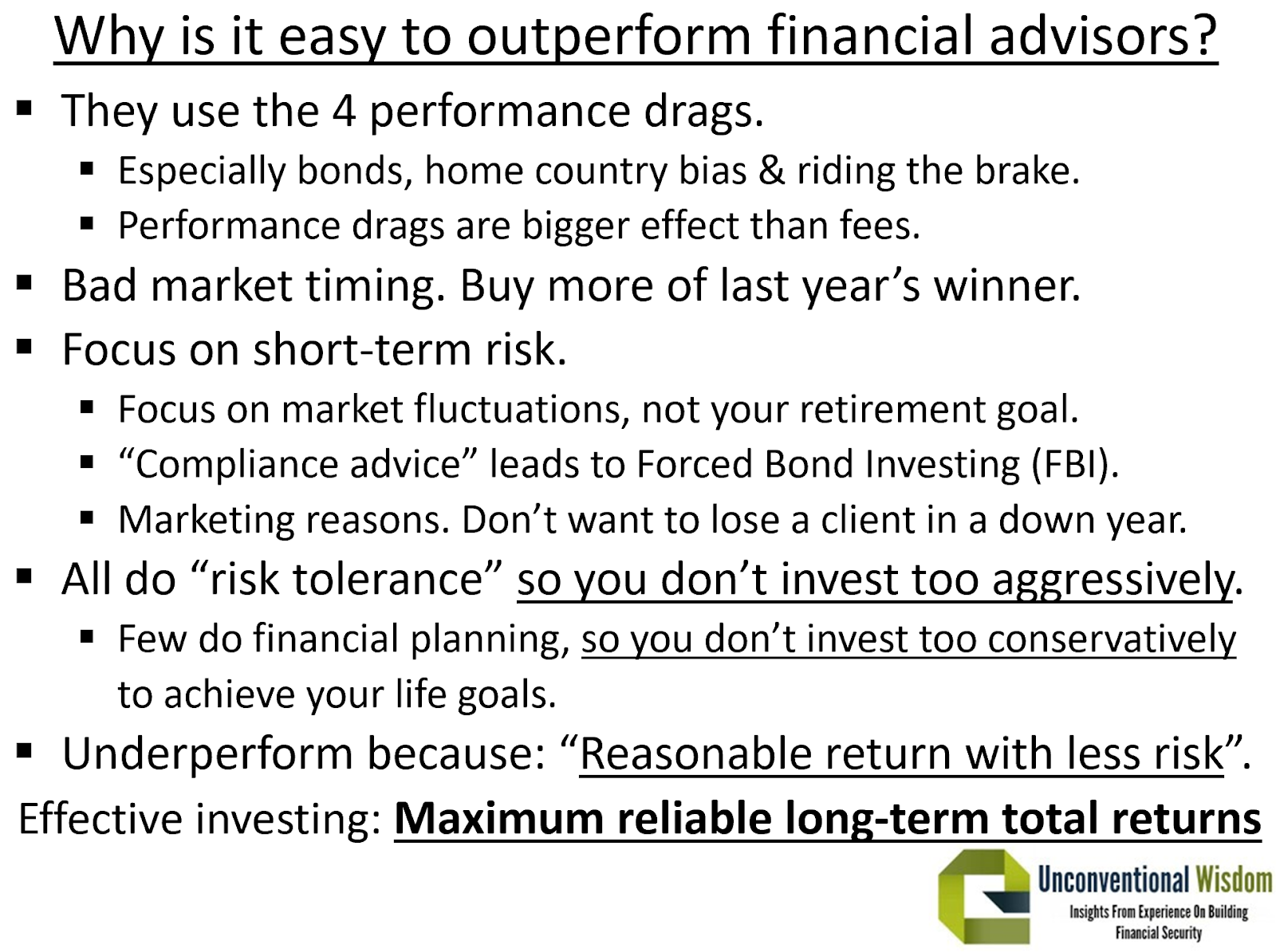

Why is it easy to outperform financial advisors?

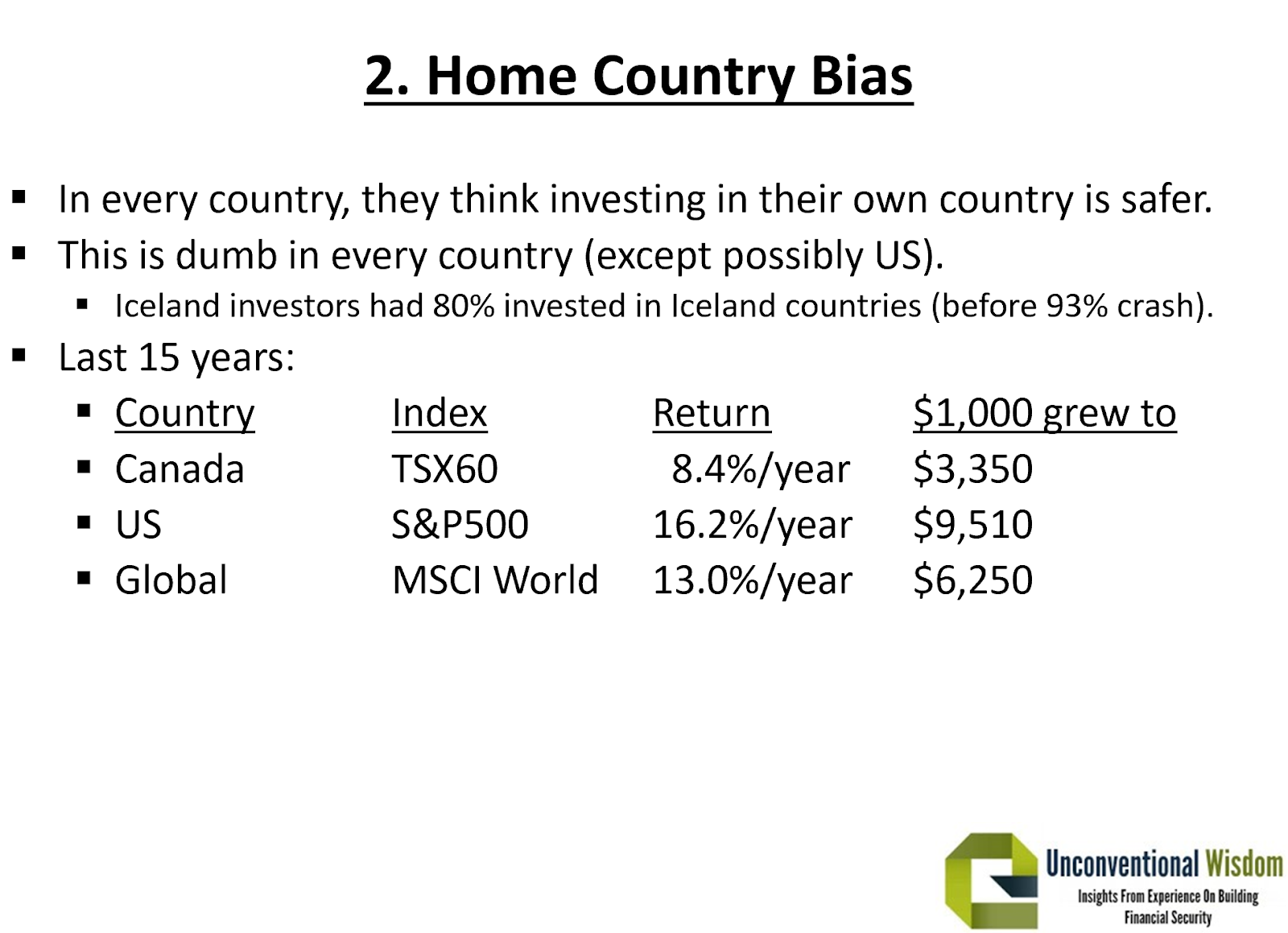

Many investors can outperform financial advisors due to systemic flaws like home country bias and short-term thinking in traditional investment advice.

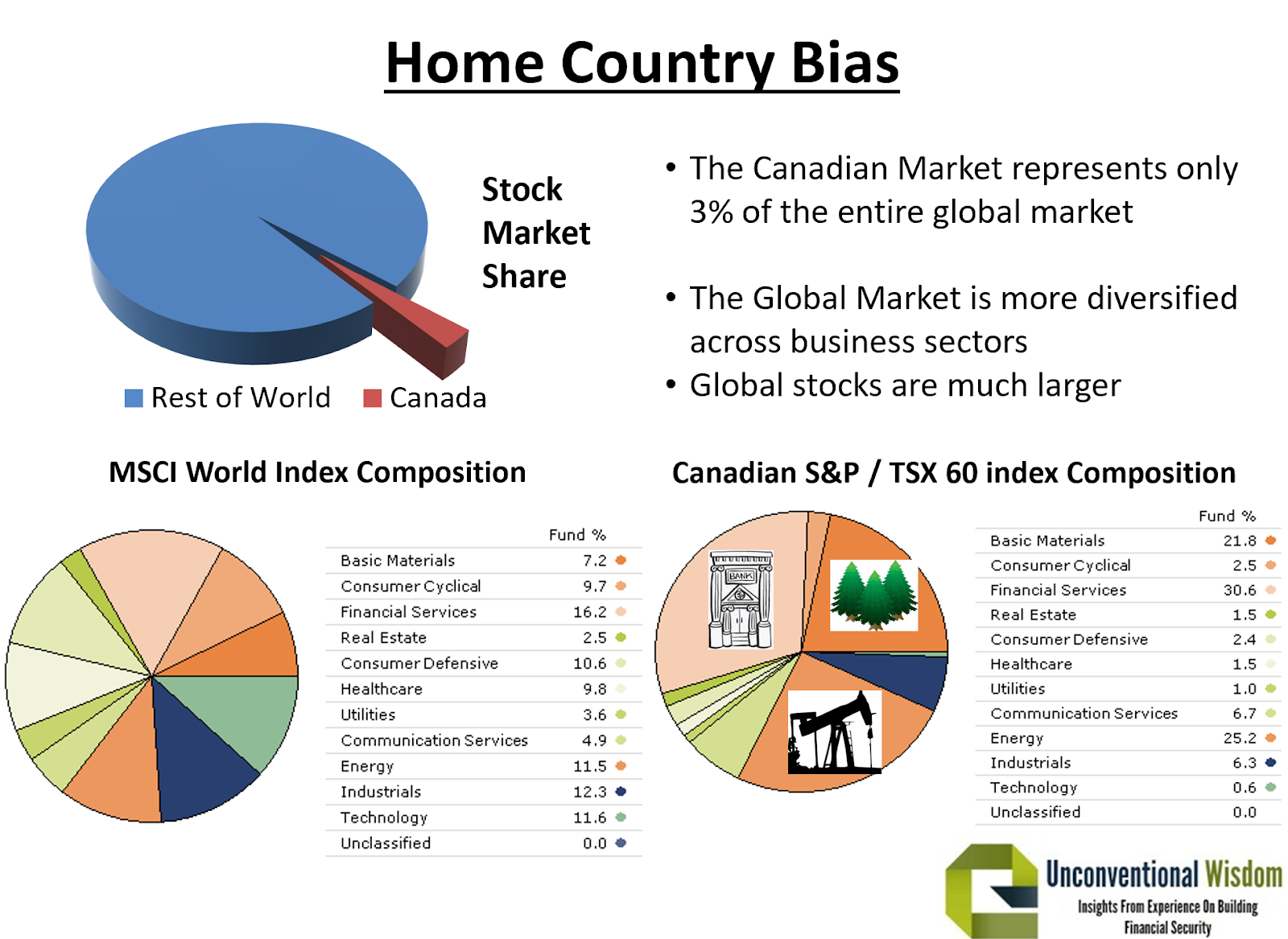

Home country bias, for example, leads investors to focus heavily on domestic markets, believing it’s safer. However, this strategy often underperforms. Take Canada as an example: Over the past 15 years, the TSX 60 Index returned 8.4% annually, growing $1,000 to $3,350. By contrast, the S&P 500 returned 16.2%, growing $1,000 to $9,500, and the MSCI World Index returned 13%, growing $1,000 to $6,250.

The Canadian market represents only 3% of the global market, and most of it is concentrated in three sectors: resources, energy, and financials. This lack of diversification limits growth opportunities. By investing globally or focusing on U.S. markets, where growth is significantly higher, individuals can access the world’s best companies and outperform portfolios constrained by home country bias or conservative strategies recommended by some advisors.

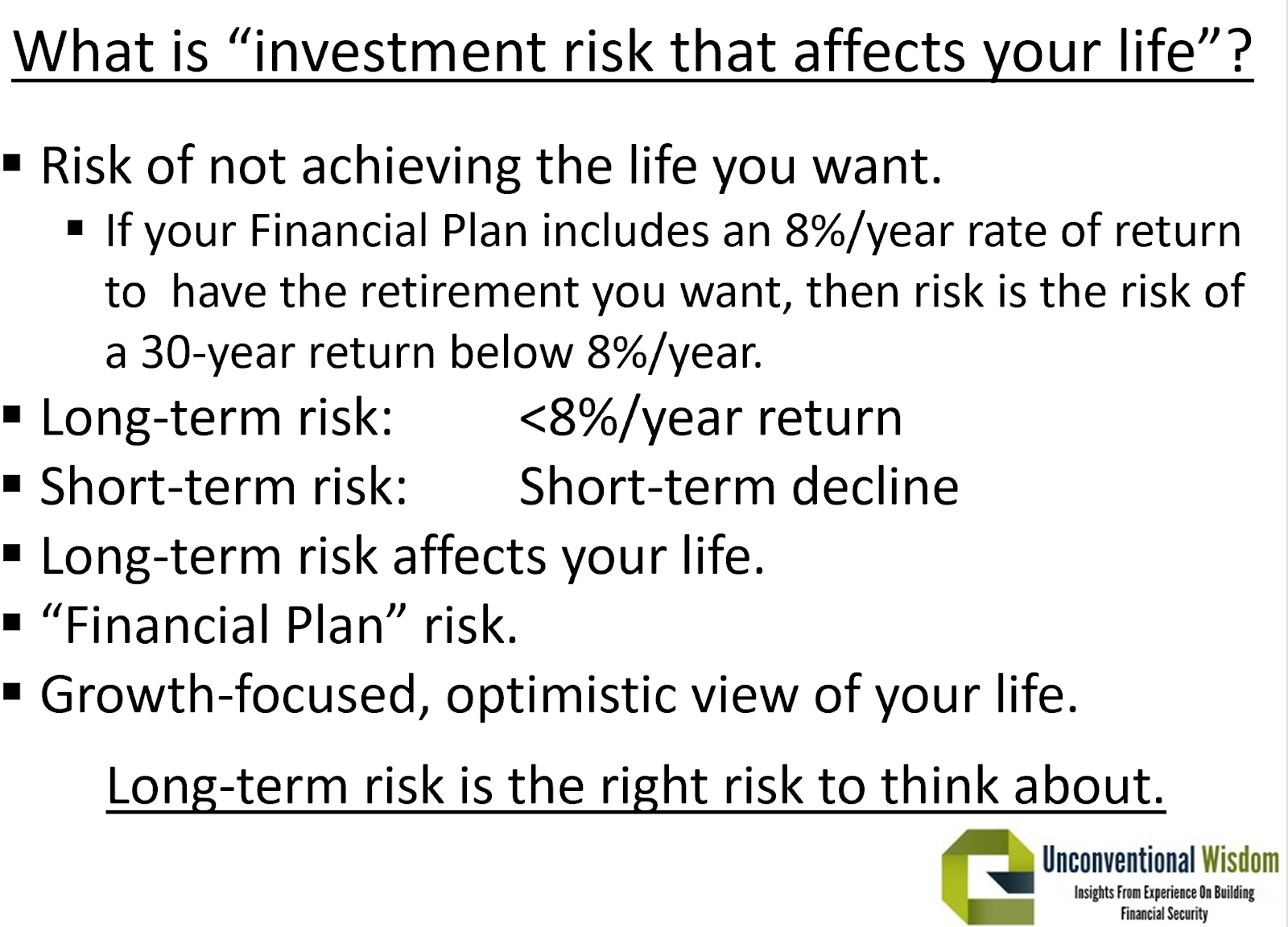

What is wrong with the investment industry definition of “risk”?

The investment industry often defines risk as short-term volatility, which can lead to overly conservative investment strategies. This focus on minimizing volatility—what I call “riding the brake”—causes investors to prioritize short-term stability at the expense of long-term growth. Common conservative strategies include balanced asset allocations, income-focused investments (like bonds and GICs), and trendy low-volatility or dividend-based stocks.

While these approaches reduce short-term fluctuations, they often result in suboptimal long-term returns.

For example, strategies like income investing or relying heavily on dividend-paying stocks limit growth opportunities by shrinking the universe of potential investments. This narrow focus is misleading because it emphasizes stability over the broader objective of achieving the maximum reliable long-term return. In reality, short-term volatility is not the real risk; failing to meet your long-term financial goals is the greater danger. Therefore, a better definition of risk involves considering the probability of not achieving the desired return to meet life objectives rather than simply avoiding short-term losses.

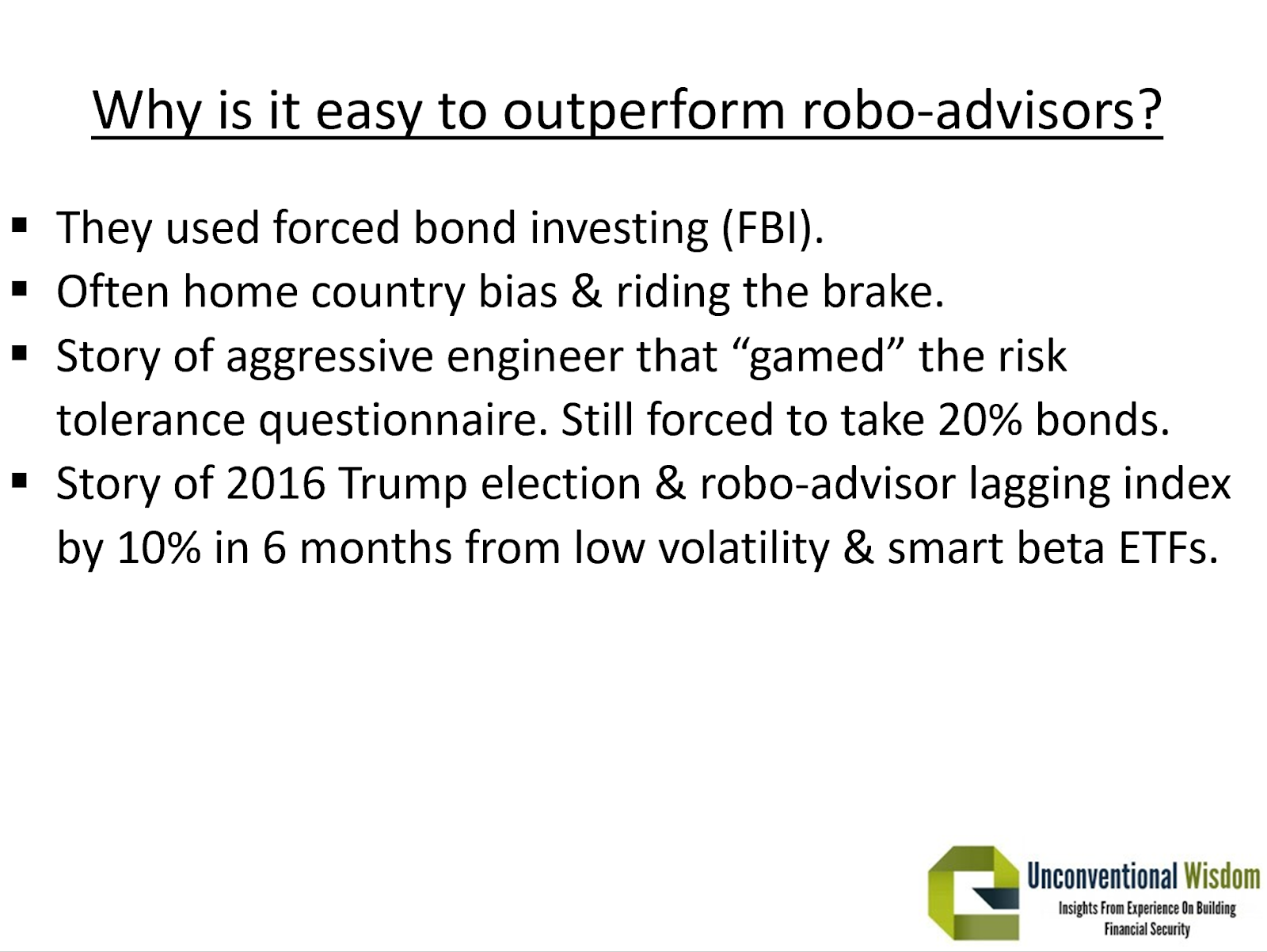

Why Is It Easy to Outperform Robo-Advisors?

Robo-advisors often have rigid, standardized approaches to investing. A common feature is the forced inclusion of bonds in portfolios, even for investors with high risk tolerance. For example, an engineer in his late 20s, highly knowledgeable about investing, wanted a 100% equity portfolio. After manipulating the robo-advisor’s risk tolerance questionnaire to the most aggressive answers, he was still assigned 20% bonds. When he questioned this, the robo-advisor insisted that the minimum allocation to bonds was 10%, regardless of his actual preferences. This policy is more about protecting the robo-advisor than serving the investor’s best interests.

Robo-advisors can also fall into the trap of trendy investment strategies, such as allocating to low-volatility or “smart beta” ETFs. For instance, in 2017, some robo-advisors significantly underperformed broad market indices because they invested in these strategies, which lagged during a high-growth market. These trendy options might look appealing from a marketing perspective but often fail to deliver optimal results.

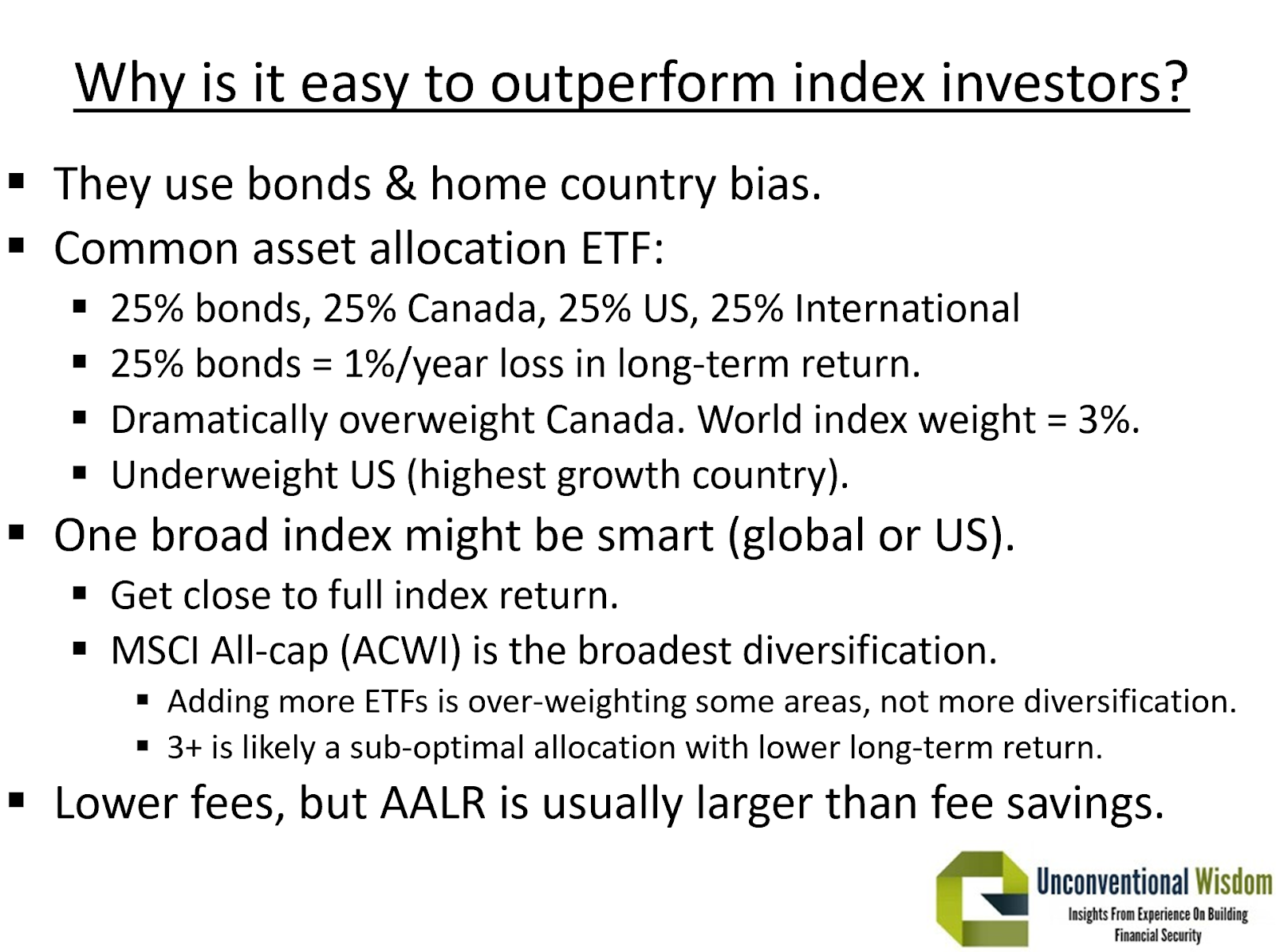

Why Is It Easy to Outperform Index Investors?

Index investors often don’t stick to a single, broad index like the MSCI World All Cap Index, which provides the most diversification. Instead, many diversify across multiple narrower indices, ironically making their portfolios less diversified. For instance, some may hold asset allocation ETFs with allocations such as 25% bonds, 25% Canadian equities, 25% U.S. equities, and 25% international equities. This approach has several flaws:

- Bond Allocations: Bonds can reduce long-term returns by 1% or more annually, depending on the allocation.

- Home Country Bias: Allocating 25% to Canadian equities when Canada’s market weight is only about 3% leads to overexposure to a lower-growth market.

- Underweighting U.S. Equities: The U.S. comprises about 60% of global market capitalization, yet many index investors significantly underweight it.

This misallocation often results in portfolios that are both less diversified and lower-performing compared to a single broad index. Additionally, the focus on minimizing fees often overshadows the impact of asset allocation losses (AALR), which can cost more than the savings from lower fees.

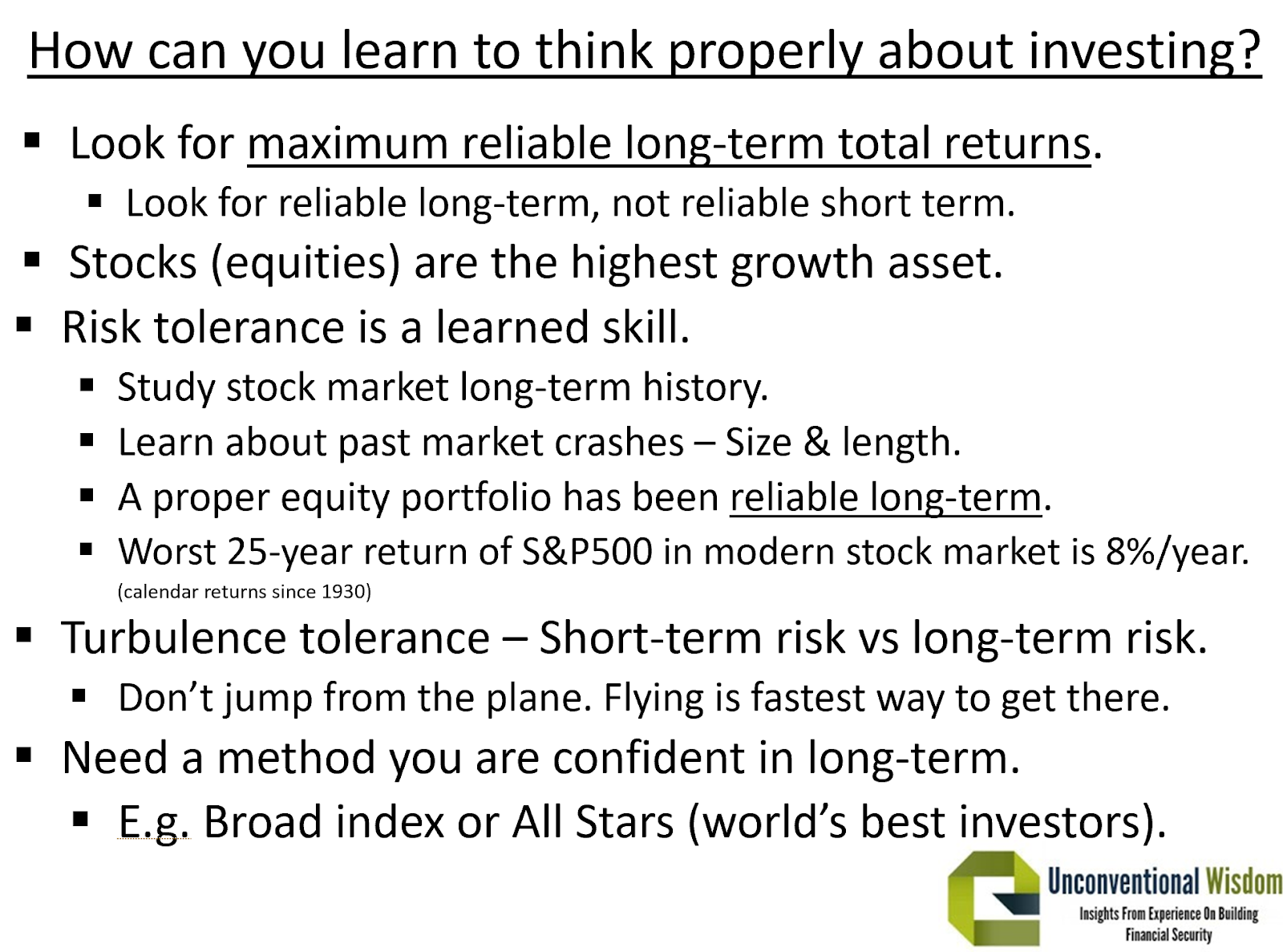

How Can You Learn to Think Properly About Investing?

To succeed in investing, focus on Maximum Reliable Long-Term Total Returns:

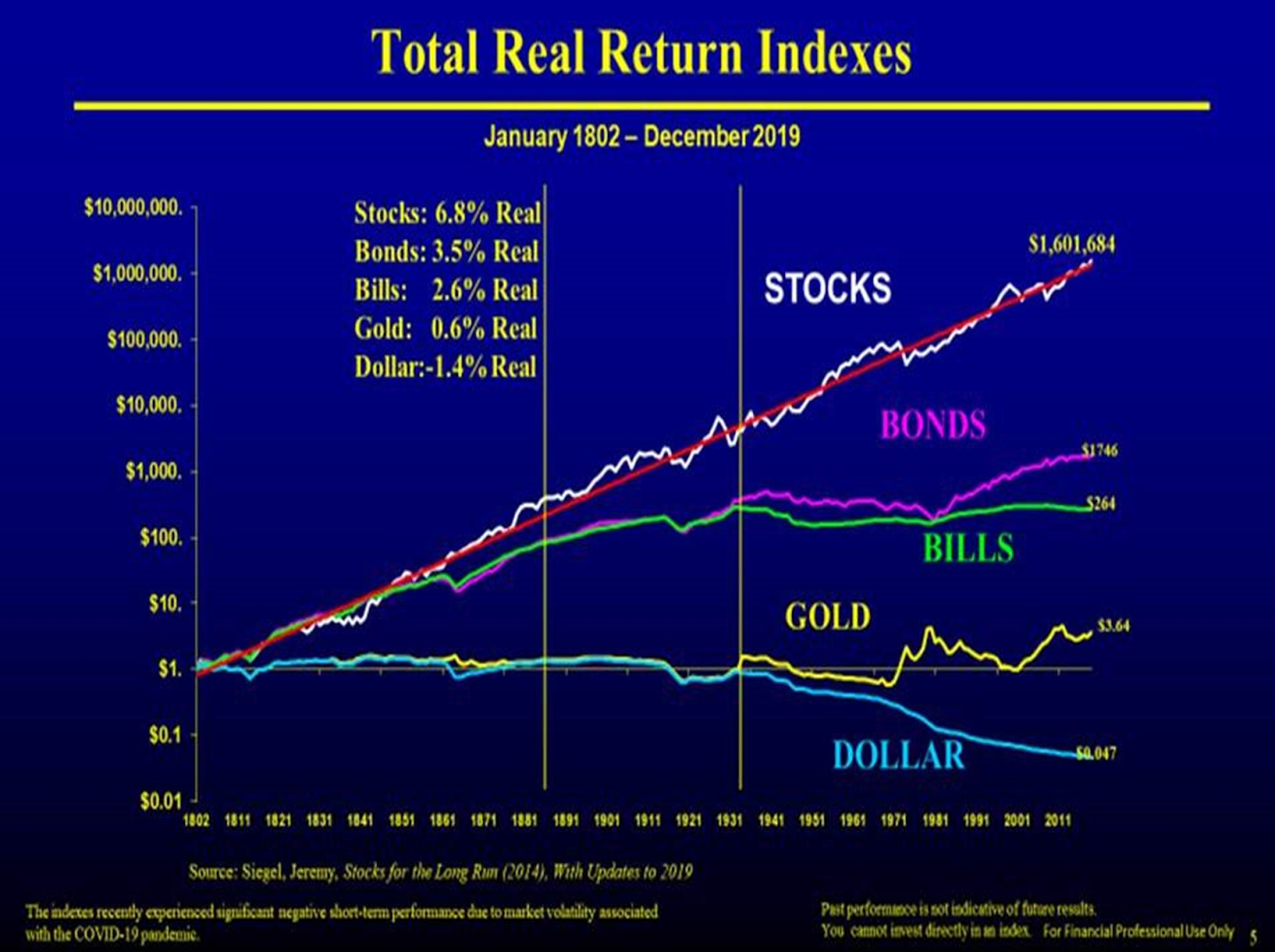

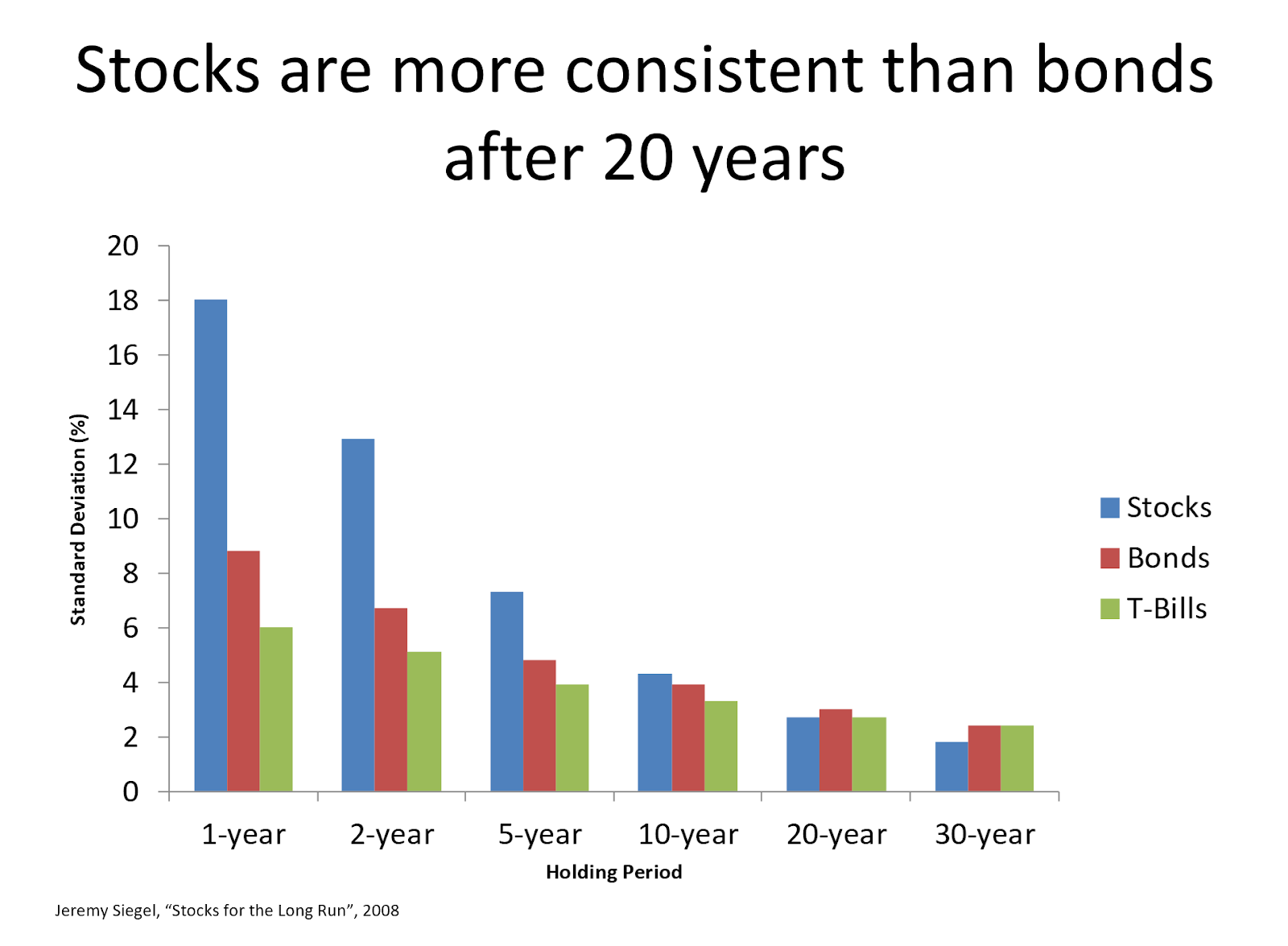

- Understand Equity Performance: Historically, equities have provided consistent long-term returns, averaging inflation plus 7% annually over the past 150+ years. This makes equities more reliable than bonds over 20+ year periods.

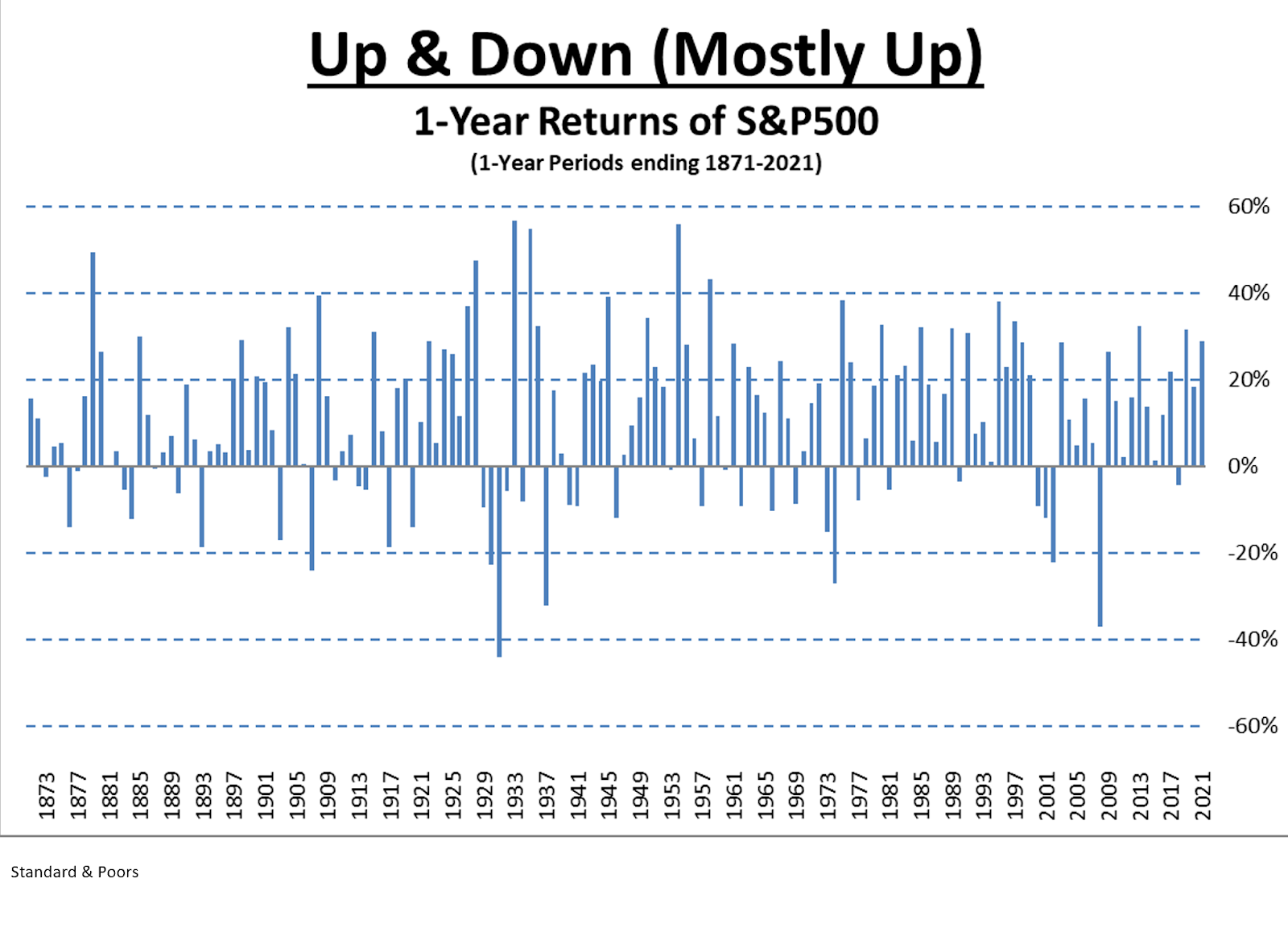

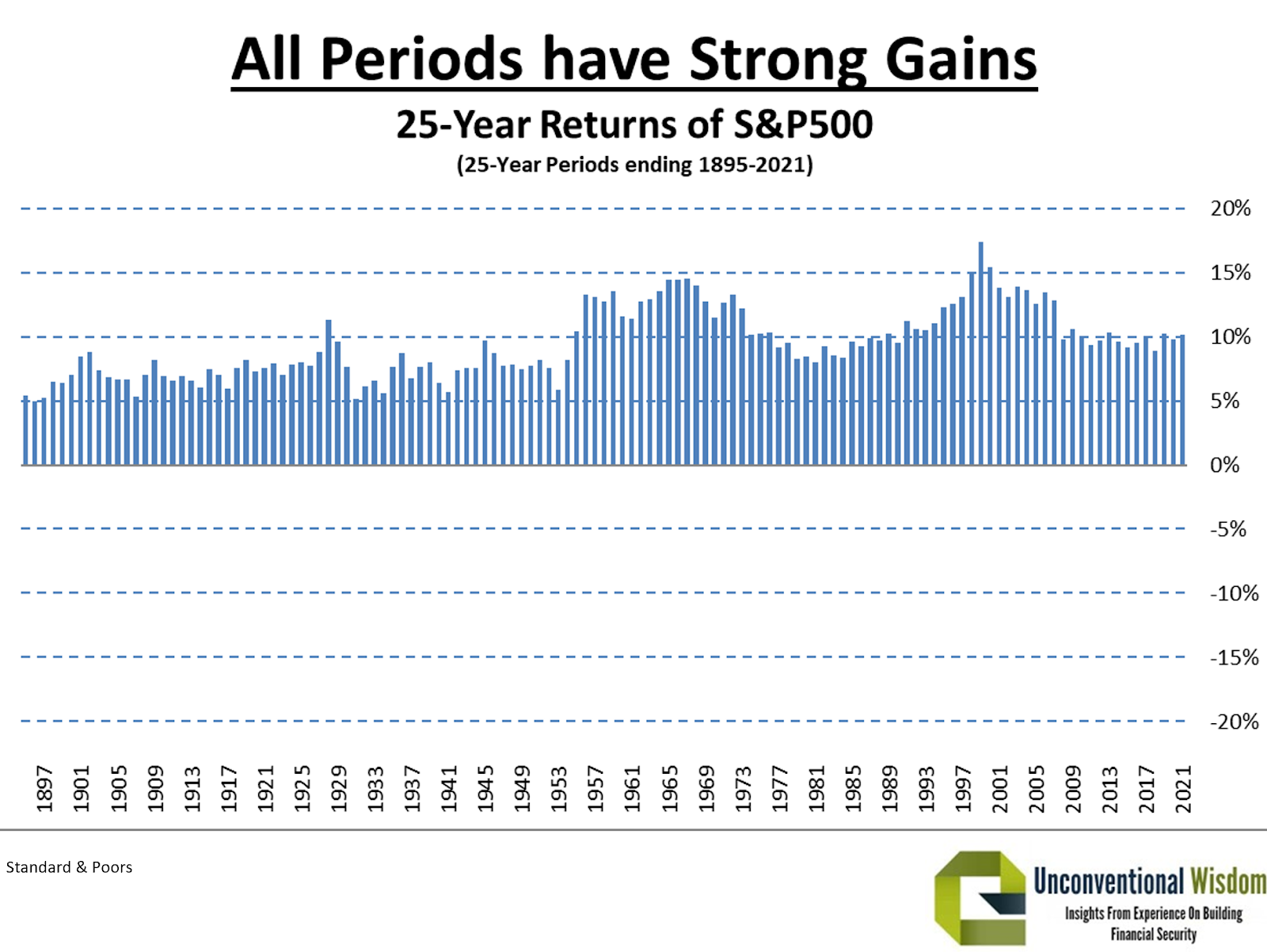

- Study Market Behavior: Learn the realities of market declines, recovery times, and long-term trends. Many investors perceive the market as riskier than it is due to a lack of understanding. For example, the worst 25-year return for the S&P 500 since 1930 was still a solid 8% annually.

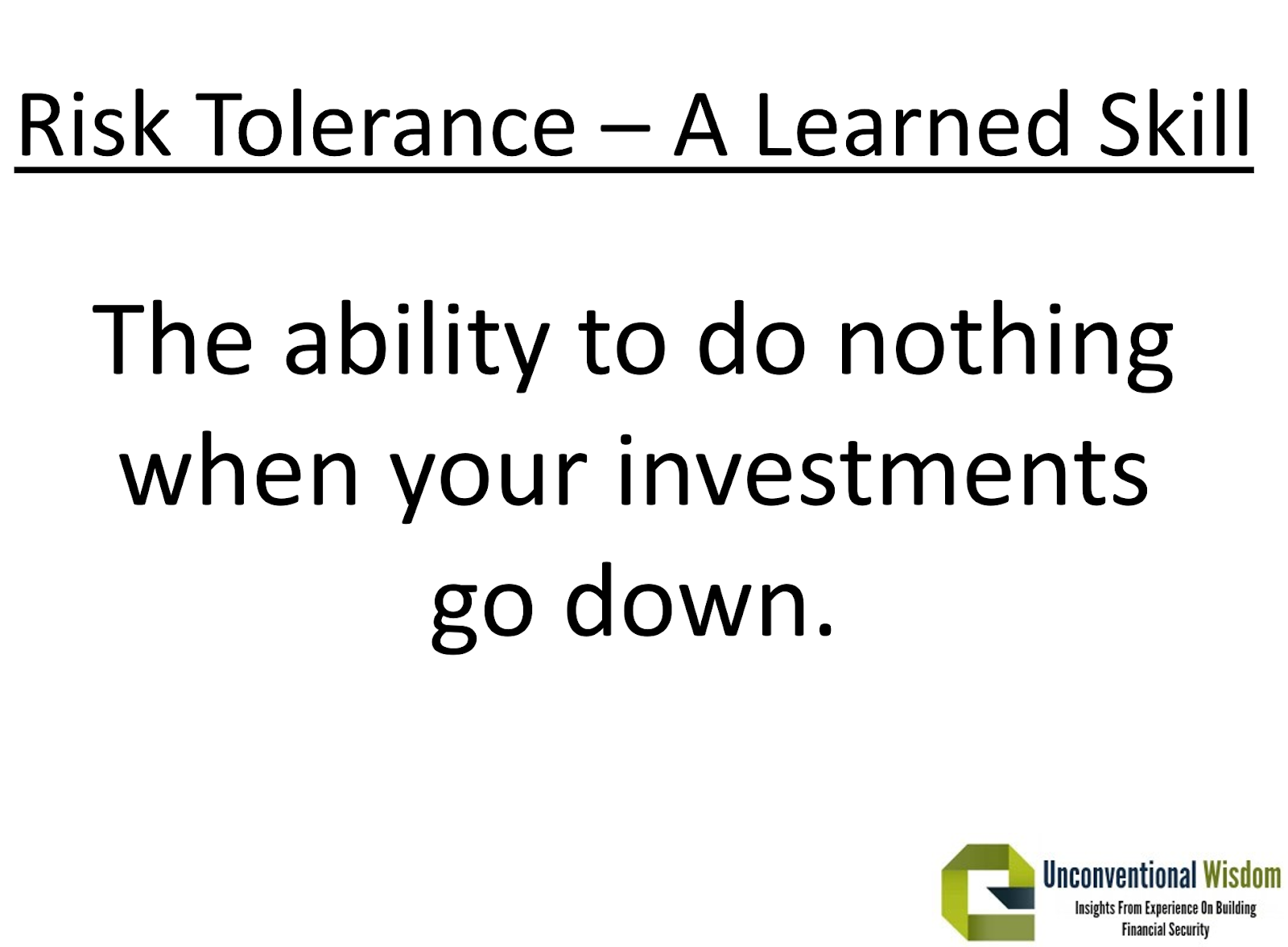

- Develop Turbulence Tolerance: Accept that short-term volatility is a natural part of investing. A market crash is typically a temporary drop of 20–50%, followed by recovery. Understanding this can help you stay focused on the long-term benefits.

By gaining a clear, data-driven understanding of market behavior, you can build confidence and increase your tolerance for volatility—a skill that is learned, not innate.

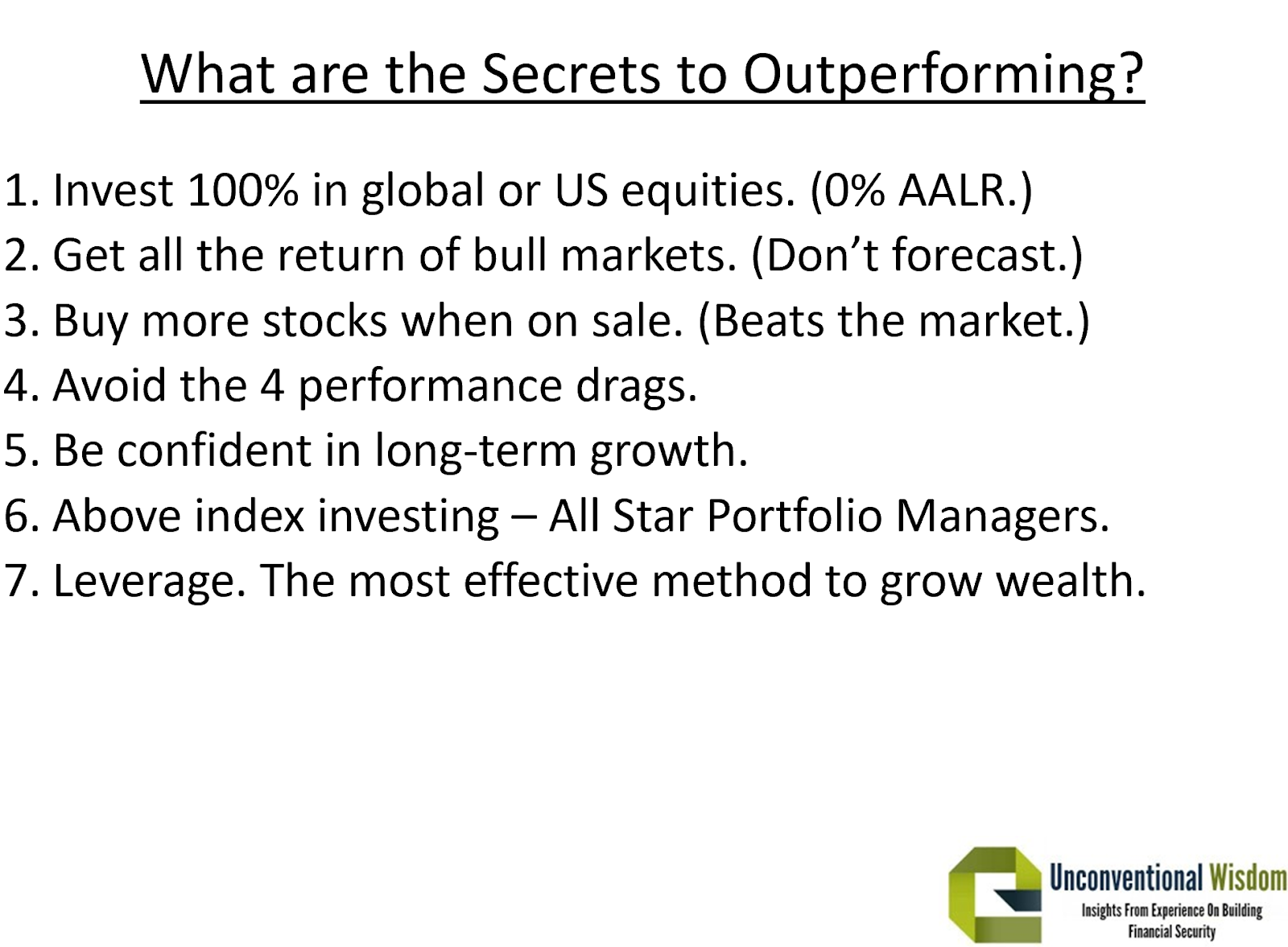

What Are the Secrets to Outperforming?

- Avoid Unnecessary Bonds: Bonds may provide stability, but they often come at the cost of lower long-term returns. Investors with a high risk tolerance should consider prioritizing equities for better growth.

- Stay Broadly Diversified: A single, comprehensive index like the MSCI World All Cap Index provides maximum diversification. Avoid overcomplicating your portfolio with multiple indices or trendy strategies.

- Think Long Term: Focus on reliable, long-term growth rather than short-term gains or losses. Understand that market declines are temporary and part of the investing journey.

- Educate Yourself: Knowledge reduces fear. By studying market trends and understanding the data, you can improve your confidence and decision-making.

- Avoid Trendy Investments: Resist the allure of strategies like smart beta or low-volatility ETFs that often underperform during strong market periods.

By following these principles, you can build a resilient portfolio that consistently outperforms robo-advisors and poorly constructed index strategies.

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

What do you mean by “long term “….10 yrs, 20 yrs, 30 years?

Doesn’t it depend on your age?

30 yrs to a 50 yr old might be reasonable

30 yrs to a 70 yr old doesn’t seem appropriate at all.

An I completely off base?