RRSP Gross-up Strategy – Easily Contribute 40-70% More to Your RRSP (2024)

The RRSP Gross-up Strategy is a relatively simple concept that can help you contribute 40-70% more to your RRSP, without using any more of your cash.

Do this every year and you can retire with 40-70% higher income for life!

RRSP Gross-up Strategy (2024) – Easily Contribute 40-70% More to Your RRSP

- Cash flow may be tight with high inflation.

- RRSP Gross-up Strategy – Relatively simple strategy to contribute 40-70% more to your RRSP without using your cash flow.

- Do it every year and you can retire with 40-70% higher income for life!

Tax refund options

1. Spend it.

2. Invest it.

3. RRSP Gross-up Strategy.

Your Tax Refund

- NOT free money.

- Loan from government.

- You pay it back when you withdraw from RRSP.

- Your Financial Plan helps you think about the best use for your tax refunds.

RRSP Gross-up Strategy

Instead of contributing your tax refund:

- Contribute 40-70% more in February from credit line.

- You tax refund pays it off in March.

Need to know:

- RRSP room.

- Marginal tax bracket.

- “Optimal RRSP room”.

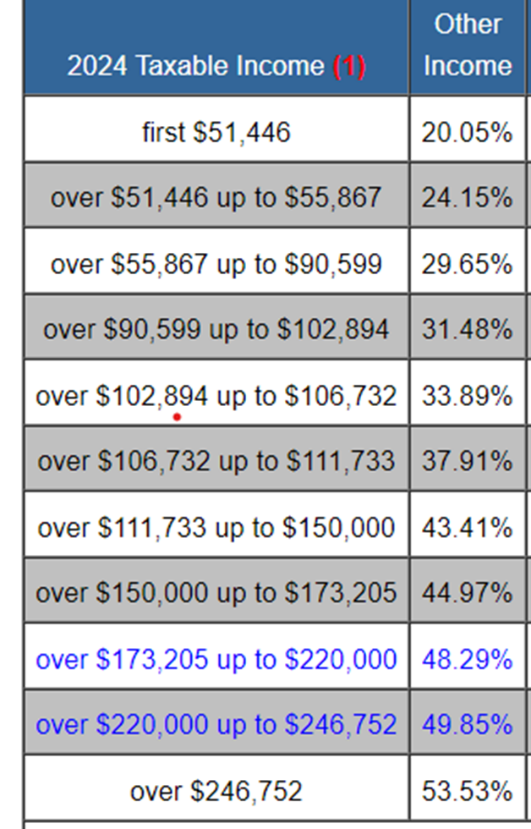

Marginal Tax Brackets (2024)

Major Tax Brackets (Ontario 2024)

From To Bracket

$0 $56,000 20%

$56,000 $107,000 30%

$107,000 $173,000 43%

$173,000 $247,000 50%

$247,000+ 54%

Optimal RRSP Contribution

How much should you contribute to your RRSP?

6 Factors:

1. Achieve your retirement goal.

o If you have a Financial Plan, you will know this amount.

2. Maximize your lifetime RRSP room.

3. Your current marginal tax bracket (or close).

4. Your current RRSP room.

5. Your available cash (or credit line available).

6. Target RRSP refund.

o Your refund covers the contribution.

“Optimal RRSP Contribution” – Valuable planning concept.RRSP Gross-up Formula

Expected tax refund / (1-Marginal tax rate) = Gross-up

E.g., $10,000 tax refund/ (1-43% tax bracket) = $17,500

Magically contribute $7,500 more to your RRSP without using your cash flow.

Compared to contributing your refund:

- Contributing $ 7,500/year for 30 years @8% = Over $900,000!

Compared to spending your refund:

- Contributing $17,500/year for 30 years @8% = Over $2 million!

RRSP Catch-up Strategy

- “RRSP Gross-up on Steroids”.

- Catch-up most or all your RRSP room in one step.

- Can be a game-changer for your life.

- Every case is unique.

- It takes creativity to work out the best strategy.

- Contribute up to 5 years’ RRSP contributions now.

- Deduct only the optimal amount on your tax return.

- Carryforward deduction to get a few large refunds.

- Roll into your mortgage for lowest interest rate.

RRSP Catch-up Strategy Example

- Income $150,000/year. $200,000 RRSP room. Age 45.

- Contribute $200,000 to RRSP.

- Deduct $40,000/year for 5 years.

- Get $20,000 tax refund for 5 years.

- Roll $200,000 into mortgage.

- Increased payment $1,300/month. Less than tax refund.

- $200,000 grows to $930,000 @8% in 20 years.

RRSP Catch-up Strategy Result

- You maximized your RRSP room.

- You can keep it maximized every year.

- Refund can be more than your payment for years.

- You retire more comfortably.

RRSP Catch-up + RRSP Gross-up

Combining RRSP Catch-up + RRSP Gross-up:

- Do RRSP catch-up.

- Do RRSP gross-up every year on expected refund.

Benefit can be 40-70% more than RRSP catch-up!

Related Videos/Podcasts/Blogs

Details of RRSP gross-up & catch-up strategies.

“Interactive” retirement planning.

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

Hey Ed. Thanks for this info.

In the catch-up strategy, how does the principal get dealt with after the 5 years of tax refunds? Are you not left with an extra $1300 to pay every month for the life of your mortgage? I get it that long term you are still ahead of the game providing markets return at historical levels, but you have to be prepared for this in terms of your cash flow capacity for quite some time, correct? Which by the math in this scenario is an additional 20 years, I believe. (I think 1300 is about the payment on a 25 year mortgage of 200,000 at 5-6%). Or am I missing something?