Unlocking Peace of Mind with the Smith Manoeuvre: Turning Your Home into a Wealth-Building Engine—Without Sacrificing Today

For many Canadians, homeownership is so much more than just a financial investment. It’s where our children grow up, where we host Sunday dinners, and where we build our lives. Because our homes mean so much to us, our natural instinct is to protect them. We work hard, make sacrifices, and commit to paying off our mortgages as quickly as possible—often directing every spare dollar toward that milestone.

But it’s worth asking a gentle, yet important question:

What if aggressively paying down your mortgage isn’t the only way to secure your family’s future?

For decades, the traditional path has unintentionally left many hardworking Canadians “house rich, cash poor.” They sit on a beautiful, valuable asset, but enter their golden years with anxiety because they lack the liquid investments needed to truly enjoy retirement.

Fortunately, there is a thoughtful strategy that challenges this trade-off. It’s called the Smith Manoeuvre, and it’s designed to help you build a secure tomorrow without sacrificing the joy of today.

The Story Behind the Strategy

This innovative approach wasn’t born in a corporate boardroom; it came from a desire to give Canadian families a financial leg up. The strategy was pioneered by Fraser Smith, a financial planner from Vancouver Island, British Columbia.

Fraser noticed a glaring inequality: while American homeowners could deduct mortgage interest from their taxes, Canadians could not. Recognizing how deeply this impacted the average family’s ability to save for the future, Fraser dedicated his career to leveling the playing field.

He developed a legal, structured way to help Canadians systematically convert expensive, non-deductible mortgage debt into tax-deductible, wealth-building equity. He eventually shared his findings with the world in his groundbreaking book, “The Smith Manoeuvre: How to Use the Equity in Your Home to Build Wealth.” Today, his legacy continues to give families across the country a sense of financial control and hope.

The Heart of the Strategy: Recycle, Don’t Restrict

One of the heaviest burdens families face today is the feeling that they aren’t saving enough. Between grocery bills, kids’ activities, and everyday life, finding “extra” cash flow to invest can feel nearly impossible.

The beauty of the Smith Manoeuvre is that it doesn’t ask you to find extra money. It doesn’t ask you to skip family vacations or cut out your morning coffee. Instead, it does something incredibly clever: it recycles the money you are already paying toward your mortgage.

Instead of waiting 25 years to finally start building a retirement nest egg, you begin investing from day one, seamlessly weaving wealth creation into your existing lifestyle.

How It Works: A Simple Journey

Let’s look at how this works in practice, using a straightforward example:

The Starting Point

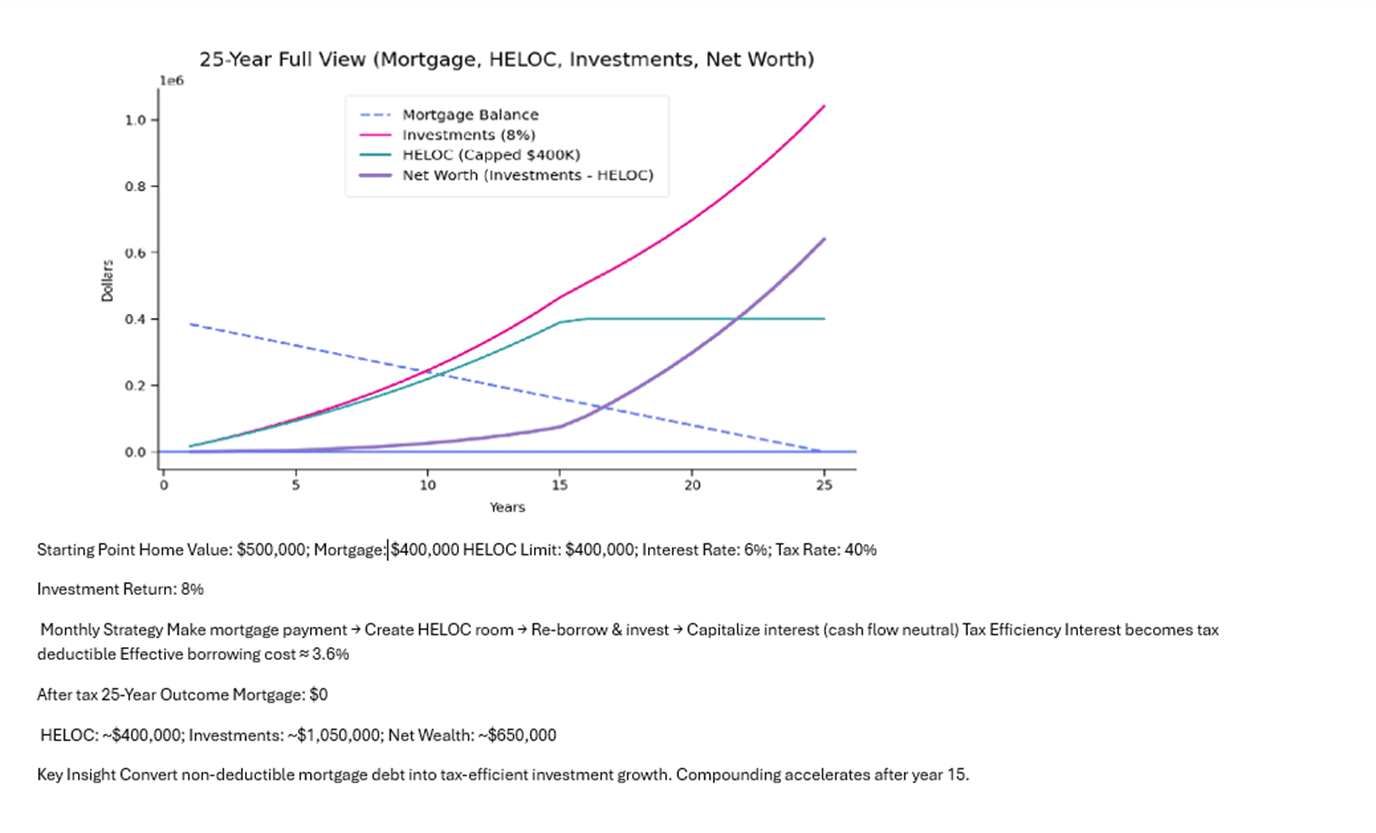

- Home Value: $500,000

- Current Mortgage: $400,000

- The Tool: A re-advanceable mortgage with a Home Equity Line of Credit (HELOC)

- Interest Rate: 6% | Tax Rate: 40%

The Monthly Rhythm

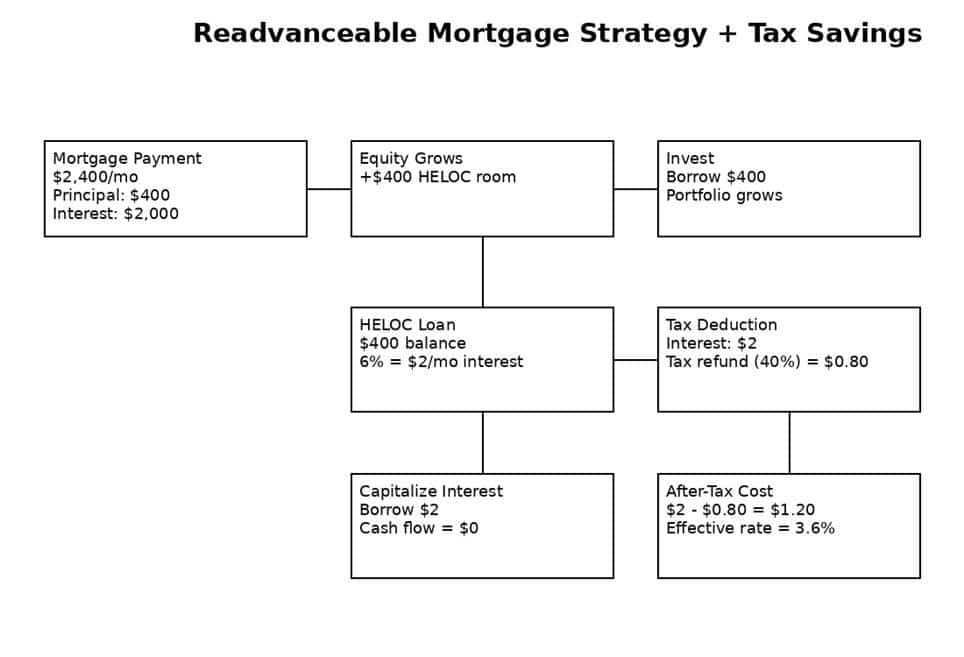

- You make your regular mortgage payment: Your life and monthly budget remain exactly the same.

- Your equity grows: With every payment, the principal portion reduces your debt and automatically increases your available credit line (HELOC).

- You invest in your future: You draw that newly available credit and invest it into a non-registered investment account.

- The cycle repeats: Month after month, a quiet transformation takes place.

Over time, your inefficient, non-deductible mortgage debt shrinks, while your tax-deductible, wealth-building investment loan grows. You are safely converting “bad debt” into “good debt.”

Protecting Your Cash Flow

A common worry is, “Won’t paying the interest on the loan hurt my monthly budget?” The elegance of this strategy lies in capitalizing the interest.

If your monthly HELOC interest is $65, you pay it, and then immediately re-borrow that $65 from the credit line to cover it. The net impact on your daily cash flow is exactly zero. Your strategy runs quietly in the background while you focus on living your life.

Real Stories, Real Peace of Mind

Behind the math are real people who have used this strategy to reshape their futures.

1. The Busy Mid-Career Family (The Gift of Time)

- The Profile: Parents in their early 40s. Dual income, but life is expensive and surplus cash is tight.

- The Worry: They felt guilty that their mortgage was shrinking but their retirement savings were stagnant.

- The Journey: They implemented the Smith Manoeuvre. Over 15 years, without changing their lifestyle, they built a robust six-figure investment portfolio alongside their home equity.

- The Wholesome Impact: Today, they have options. They can afford to ease into retirement three to five years early, spending precious time with future grandchildren rather than feeling locked to a desk.

2. The High-Income Professional (Relieving the Burden)

- The Profile: In their late 30s, working long hours, and facing a heavy tax burden.

- The Journey: Used the strategy to generate tax deductions, reinvesting their annual tax refunds directly back into the mortgage to accelerate the safety of a debt-free home.

- The Wholesome Impact: By building a parallel wealth engine, they bought themselves optionality—the freedom to reduce working hours or pivot careers without compromising their family’s security.

3. The Late Starter (Restoring Hope)

- The Profile: In their early 50s, holding a mortgage, and feeling a sense of panic about a late start to retirement savings.

- The Journey: Adopted a mindful, scaled version of the Smith Manoeuvre.

- The Wholesome Impact: While they might not retire decades early, they successfully closed the retirement gap. The true victory? Replacing financial anxiety with confidence and a sense of control over their golden years.

Is This Path Right for Your Family?

While the math is beautiful, the Smith Manoeuvre is ultimately an emotional and behavioral strategy.

| This might be a perfect fit if you: | This might not be the right fit if you: |

| Focus on the long horizon (15+ years) | Lose sleep over short-term market drops |

| Want to protect your current lifestyle | Prefer the psychological comfort of being entirely debt-free |

| Value discipline and organized finances | Want a quick fix or a DIY weekend project |

The Bigger Picture: Your Home as an Active Partner

The true magic of the Smith Manoeuvre isn’t just the tax deduction. It’s the gift of time and compounding.

Instead of waiting decades to let compound interest work its magic, you invite your home to become an active partner in your financial wellness today. Your home goes from being a passive asset that simply absorbs your income, to a living engine that quietly builds a prosperous, stress-free future for the people you love most.

Final Thoughts

Building wealth doesn’t have to mean compromising your current happiness. With patience, structure, and the right professional guidance, you can protect your home, nourish your family’s lifestyle today, and step boldly into a secure tomorrow.

-Sabiha

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.