National Post article: Does this 84-year-old suffer from the ‘Multimillionaire’s Dilemma?’

Louise (not her real name) has far more money than she is ever likely to spend. She has always invested in equities and is comfortable with them. However, now at age 84, she is wondering whether she should invest more conservatively.

This is a case study about the “Multi-Millionaire’s Dilemma.”

Louise says:

“Many of my women friends have the same concern: Is my asset allocation suitable for me? Specifically, what proportion should I invest in GICs versus broad-market index ETFs? Tax efficiency is also a concern.”

In my latest blog post, video and podcast episode you will learn:

- What is the “Multi-Millionaire’s Dilemma”?

- How is Louise’s situation similar to the “Multi-Millionaire’s Dilemma”?

- What reasons might she have for investing more conservatively with GICs?

- What reasons might she have for staying invested in equities?

- How can understanding the odds of losing money and the potential for growth help her decide?

- What are the odds that her investments will be worth less at the end of her life?

- How much could they be down in a worst-case scenario?

- How much less is she likely to earn by switching from equities to GICs?

- How can she simplify her investments if she stays in equities?

CLICK THE LINK BELOW TO READ THE ARTICLE BY MARY TERESA BITTI:

Does this 84-year-old suffer from the ‘Multimillionaire’s Dilemma?’

Louise’s Story

At 84, Louise is looking to simplify her investment portfolio, minimize tax, and make sure she maintains her current lifestyle. This includes continuing to travel five to six times a year, albeit more locally than her past global adventures, and age in place in her home in Vancouver, bringing in any additional help she might need.

To this point, Louise has built and managed a portfolio largely composed of equities. About a year ago, she sold most of her stocks and now has $1 million in nine guaranteed investment certificates (GICs) in three different financial institutions currently paying out about 3 per cent every other month. She has $70,000 in dividend paying stocks, $80,000 in two equity exchange traded funds (ETFs), $220,000 invested in gold wafers, $110,000 in cash, $130,000 in a Tax-Free Savings Account and $110,000 in a Registered Retirement Income Fund, both also invested in GICs.

Last year her annual income was $66,000 ($27,000 from an employer pension, Canada Pension Plan and Old Age Security, $3,000 in dividends and $36,000 in interest income from her GICs). Her largest expenses are monetary gifts to her family, 18 charities which include support of two Himalayan children, and personal costs. In total, she spends $10,000 a month to maintain her lifestyle. To meet shortfalls, she cashes in GICs.

“I am single with an independent Living Apart Together (LAT) partner and no children. I am not worried about leaving an estate and prefer to support people and causes while I’m alive,” said Louise, who is debt-free and in addition to her investments, also owns her condo valued at $900,000.

“I made a healthy portion of my net worth in the stock market, but as an octogenarian, I have to consider that I may not have enough time to recover from fallen growth positions in a downturn,” she said.

“I am no longer concerned with FOMO. I just want reasonable placement of my investable dollars and simplification of my financial picture.”

To that end, she would like advice on what to do with her holdings in gold and whether or not she should stay almost exclusively invested in GICs or direct a portion to an all-in-one ETF or other investment.

“Many of my women friends have the same concern: Is my asset allocation suitable for me? Specifically, in what proportion should I invest in GICs and broad index ETFs? Tax efficiency is also a concern.”

Ed’s Insights

Louise has $1,720,000 in investments and is 84. Moving to mainly GICs means her investment average return is down to about 3.2%/year – barely above inflation. Her money is parked. Average return only $55,000/year. It was almost $140,000/year average with investments growing in equities.

She only spends $66,000/year, so she won’t run out of money. She is in lower tax brackets, so tax-efficiency is only a moderate issue. Her income is comfortably below being affected by the OAS clawback and far above the level to be affected by the GIS clawback.

At age 84, if she is of average health, she has a 50% chance of reaching age 93 and a 20% chance of age 98. She should plan for at least 10-15 more years.

Bottom line: Louise has far more money than she needs and her life expectancy is likely 15 years or less. What investment allocation makes sense for her?

We call this the “Multi-Millionaires’ Dilemma”. We have seen it many times. Far more money than you will spend during your life. Continue investing for growth or switch to conservative?

Here are 2 possible ways to think about it:

Go conservative:

- She could decide to just avoid losing any money. Invest in GICs to avoid being down at the end of her life.

- Her portfolio is her security. I meet wealthy people that say, “I’m already rich. Why make more? I just have to avoid making a mistake and losing it.”

Continue investing for growth:

- She was comfortable with her equity investments, so she could choose to just keep the investments she had. The odds of her equity investments growing during her life are very high. Over the long run, equities have crushed everything else. If you look at the last hundred years, stocks have returned about 10%/year on average. She could easily live another 10-15 years or more. That is long enough for compounding to still matter a lot.

- Her money is her freedom. More money means more options in life. She can enjoy it or give more to her family or causes important to her.

- The “multi-millionaire’s dilemma” can be insightful. The classic version is this: She has far more money than she will ever need. If she was walking down the street and found a $100 bill, would she bother to pick it up? She does not need the money and it takes a little effort to pick it up. On the other hand, it’s easy to pick up and only takes a second. What would she do? Similarly (but not as simple), if she is comfortable with equities and highly likely to have them grow, why not?

General questions are often clearer when you see the numbers.

- What are the odds that her investments will be down at the end of her life?

- How much are they likely to be down in the worst-case scenario?

- How much less is she likely to make by switching to GICs from equities?

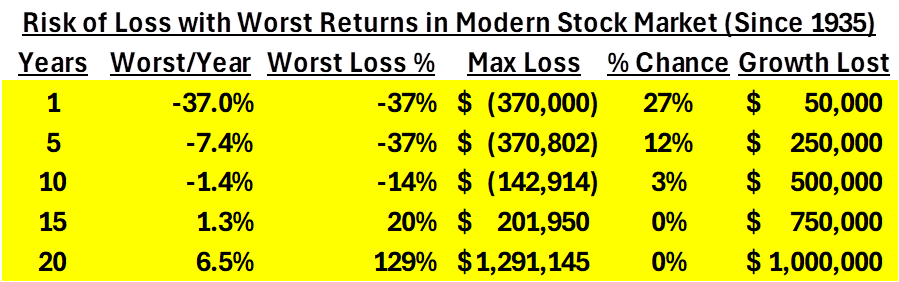

The “Max Loss” is per $1 million of her portfolio.

To understand this, if she lives 10 more years, the worst 10-year return in the modern stock market was a loss of 1.4%/year. If this worst-case happens, she would be down 14%, or $245,000. Her $1,720,000 portfolio would be down to $1,475,000. That is not a lot with the size of her portfolio.

In 10-year periods, the markets have been down only 3% of the time, so it is quite unlikely she would be down and not recover during the next 10 years. By being in GICs vs. equities for the next 10 years, the average return she could expect to lose would be about 5%/year (3% return of GICs vs. equity return conservatively 8%/year), or at least $860,000 in lost growth.

In 20-year periods, there has not been a loss. The worst case is a gain of 6.5%/year and she would gain $1,291,145 on each million she invests. The worst-case scenario is over 20 years is great news!

Looking at the numbers for 10 years or longer, the case for staying in equities is quite strong. She is likely to be $860,000 or more ahead with only a 3% chance of being down a little bit.

There is, of course, a risk that equities could lose more or make more than these figures. Nothing is guaranteed. But looking at expected returns based on history can make the decision much clearer.

For Louise, any option could be fine. It is up to her. Staying in equities when she was comfortable with them and can make far more could make sense. Avoiding any loss could also make sense.

If she stays with equities, she can simplify by buying one broad-based equity ETFs like the MSCI World Index or S&P 500, or working with a portfolio manager to look after it for her.

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

Great commentary Ed, the topic feels very close to home for me as you never know when that last day is?? Interesting point on the $100 bill on the sidewalk, makes you think.

Hope you have enjoyed your travels lately. I feel very comfortable with Sabiha and the Sage team taking on more responsibility. They are in my opinion a good group and my girls feel good with them also.

Take Care: Jack