Multi-Millionaire’s Dilemma: Stay in Stocks or Go Conservative After Retiring?

You’ve worked hard, built up a few million dollars, and now you’re seventy-five, retired, and staring at your portfolio wondering — do I really need to keep riding the stock market rollercoaster?

Or is it finally time to play it safe?

That’s the multi-millionaire’s dilemma, and it’s a lot more common than you might think.

We have seen it many times. Far more money than you will spend during your life.

Continue investing for growth or switch to conservative?

In my latest video, podcast episode and blog post you’ll learn:

- What is the “Multi-Millionaire’s Dilemma”?

- Why consider going conservative?

- Why consider continuing to invest for growth?

- What is the maximum that equities are likely to be down at the end of your life?

- What are the odds equities are down over periods of 5, 10, 15 or 20 years?

- How much growth are you likely giving up by switching from equities to GICs?

- Can the numbers make this clearer?

- What is your money for?

- Why Ed will be 100% equities his entire life.

Multi-Millionaire’s Dilemma

“Multi-Millionaire’s Dilemma”: You have far more money than you will ever need. You are walking down the street and find a $100 bill. Would you bother to pick it up?

You don’t need the money and it takes a little effort to pick it up. On the other hand, it’s easy to pick up and only takes a second. What would you do?

Similarly (but not as simple), if you are comfortable with equities and they are highly likely to grow, why not stay invested for growth?

This post is about people that have been investing in equities, are comfortable with it, and now have a portfolio far larger than they will need for the life they want – even if they live unexpectedly long. However, they are getting older and their life expectancy is 5 or 10 or 15 years.

What investment allocation makes sense?

Why consider going conservative?

You turn on the news, watch your account drop twenty percent in a few months, and suddenly the math feels different. Why have the emotional stress? At seventy-five, do you have time to wait for the market to come back?

Your portfolio is your security. I meet wealthy people that say, “I’m already rich. Why make more? I just have to avoid a mistake and losing it.”

That’s where conservative investing starts to look appealing. Just switch everything to GICs or bonds so you so you don’t lose money. You can avoid being down at the end of your life.

Why consider continuing to invest for growth?

The case for staying in stocks is pretty simple on paper. Over the long run, equities have crushed everything else. If you look at the last hundred years, stocks have returned about ten percent a year on average. Even if you’re seventy-five, you could easily live another fifteen or twenty years. Twenty years is long enough for compounding to still matter a lot.

Plus, if you have five million dollars, even a bad decade in the market isn’t going to wipe you out. You’re not living paycheck to paycheck — you’re living off a portfolio most people would kill for. Why give up that extra growth just because you’re older?

Your money is your freedom. More money is more options in life. You can enjoy it or give more to my family or give more to causes important to you.

Bonds mean you pay a lot more tax and they can lose money by getting killed by inflation. Keep investing tax-efficiently to make at least more than inflation – and hopefully a lot more.

Equities can support you living comfortably. You can get a reliable, tax-efficient cash flow from your equity investments with self-made dividends by just selling a bit every month. It’s a monthly deposit of the amount you choose to your bank account – just like a salary. Let your money keep growing to feel safer about your lifestyle.

You have been comfortable with equity investments for many years, so just keep the investments you have. The odds of your equity investments growing during your life are quite high and it can be a lot more money. The math of compounding is amazing.

Can the numbers make this clearer?

Those are the 2 main arguments. Many people make this decision based on their gut.

However, questions like this are clearer when you see the numbers.

- What is the worst-case scenario? What is the maximum that equities are likely to be down at the end of your life?

- What are the odds that equities are down from today at the end of your life?

- How much growth are you likely giving up by switching from equities to GICs or bonds?

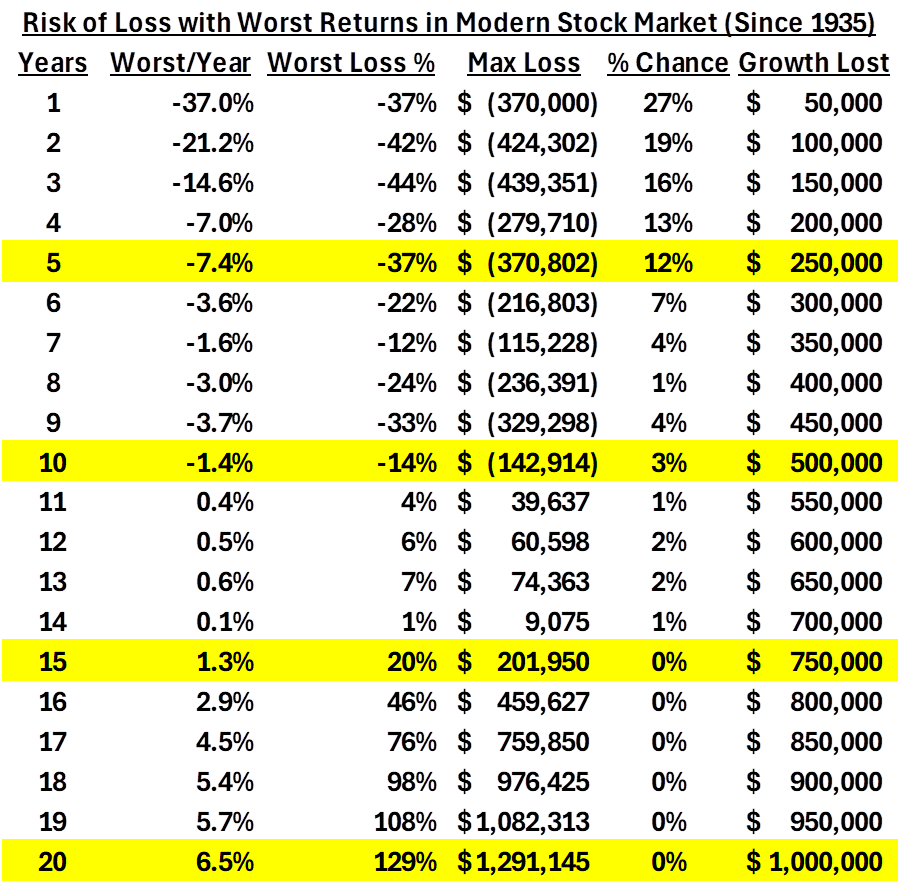

Here are the numbers based on calendar year returns in the modern stock market (since 1935). They show:

- How much of a decline has the worst-case scenario been?

- What is that in dollars for every $1 million you have?

- What are the odds that equities are down at the end of your life?

- How much growth are you giving up by selling your equites to buy bonds or GICs? Equities should conservatively make 8%/year, and GICs or bonds about 3%/year. The table shows simple math excluding the compounding, assuming you spend or give away the money.

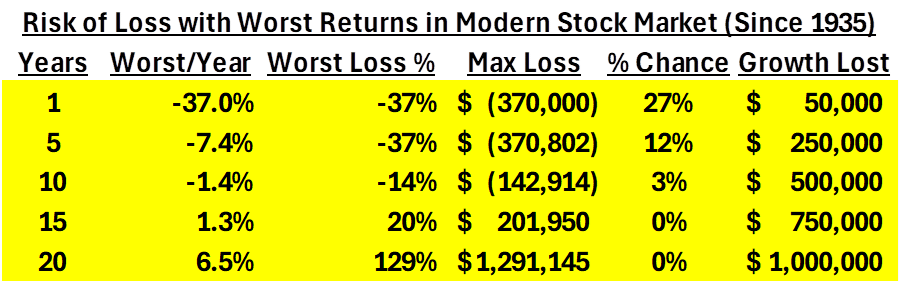

Here is a short version:

To understand this, let’s say you believe you have 10 years left to live. The worst 10-year return in the modern stock market was 1.4%/year. If this worst-case happens, you would be down 14%, or $143,000. Your $1 million portfolio would be down to $857,000. The worst-case is not really down a lot with the size of your portfolio.

In 10-year periods, the markets have been down only 3% of the time in the modern stock market, so it is quite unlikely you would be down and not recovered during the next 10 years. That is not a 3% chance of the worst-case scenario. It is a 3% chance of being down at all.

By being in GICs vs. equities for the next 10 years, the average return you could expect to lose would be about 5%/year (3% return of GICs or bonds vs. equity return conservatively 8%/year). Losing 5%/year is $50,000/year, or $500,000 in lost growth over 10 years. This does not include compounding. It assumes you spend the $50,000 or give it to your kids or charity every year. An extra $500,000 is a good number and gives you more freedom.

Looking at the numbers for 10 years or longer, the case for staying in equities is quite strong. You are likely to be $500,000 or more ahead with only a 3% chance of being down a little bit.

What about 5 years? If you are quite sure you have less than 5 years left to live, then a worst-case scenario could be being down 37% or $370,000 at the end of your life. The risk of being down at all based on history is about 12% – still low, but not irrelevant. The most likely scenario is that you would be missing out on $250,000 or more of growth.

The worst-case loss of $370,000 is larger, but it is very unlikely. The $250,000 growth is the average growth you are likely to lose. The markets have tripled in 5-year periods, so the maximum growth could be much higher, but it’s best to look at most likely outcomes.

Looking at the numbers for 5 years, the case for staying in equities is less strong, but still there. You are likely to be $250,000 or more ahead with only a 12% chance of being down a little bit plus a very low chance of being down quite a bit.

There is, of course, a risk that equities could lose more or make more than these figures. Nothing is guaranteed. But looking at expected returns based on history can make the decision much clearer.

The truth is that any option could be fine. It is up to you. Avoiding any loss could make sense. Staying in equities when you are comfortable with them and can make far more could also make sense.

It is always worthwhile to look at the numbers. Understand the risks, how likely they are, and how much growth you would lose. The numbers can make it a lot clearer for you.

What is your money for?

When we talk with people that have more money than they will ever spend, they are usually equity investors and have been for many years and are comfortable with equities. They usually have a bigger purpose for their life than just enjoying it.

It is wise to plan to have enough money to maintain your desired lifestyle, even if you live much longer than expected – and even if you have major unexpected expenses later in life. Have a comfortable margin of safety so you don’t have to worry about money.

What if you have much more than that? If you will never spend your money, then it goes to your estate or whoever you give it to. The money you won’t spend won’t be wasted. It’s smart to still be smart with that money.

We talked with people that invest conservatively to feel safe with their money. They expect to live 5 or 10 more years. All the money they won’t spend will go to their kids. Meanwhile, all their kids are investing in equities. When they pass away, their conservative investments will go to their kids who will mostly invest it in equities.

In other words, your extra money is probably really your children’s money and should be invested smartly to help them in the future. That probably means investing with a longer-term time horizon for long-term growth.

Why Ed will be 100% equities his entire life.

I will always invest 100% in equities for a few reasons:

1. I’m a huge believer in humanity, continuous growth and free enterprise, and I want to participate in it. The stock market is where we see human ingenuity and ambition, and new technologies that improve our lives. And the stock market has provided high, reliable growth over longer periods of time through history. It is the most reliable, high-growth asset class – which is why it is most effective for retirement planning.

For me, even if I knew for a fact I have only one year left, 73% of years are up, so staying invested in equities is still the best choice.

2. I fight aging every step of the way. I have so much to live for. I’m in the best longevity programs I can find and in better shape than 15 years ago. I believe that medical science will figure out how we can start living decades longer in 10 or 20 years.

I would not accept it if doctors told me I have an incurable disease with only a short life left. I would be searching for any options, including experimental treatments all over the world. I would fight it until the end – which means I could easily live longer than expected.

3. How many years you have left is uncertain. What happens if you live much longer than you think? You can believe you have only 5 years left and look at the numbers on the table to see what makes sense for you. But what makes you think you have only 5 years left? That is usually doctors telling you what happens on average – if you have an average lifestyle and don’t do anything unusual to help yourself. The average years left doctors tell you means half of people live longer. There are constantly new medical discoveries. You can look after your health and improve your odds.

4. My money is not just for me. I have family to leave it to and a charitable foundation that will get much of it. The longer I am in equities, the more money is likely to go to all these causes that are important to me.

I hope these numbers can help you make an informed decision in your life. But as for me, I will always be in equities.

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

Very insightful discussion on balancing growth and capital preservation in retirement. The perspective on staying invested is thought provoking and practical. Thanks for sharing this.