The Financial Future Isn’t Broken—But It Is Optional

Is the financial system failing Gen Z, or does it just depend on whether we choose to participate?

If you’re Gen Z in Canada, economic pessimism doesn’t feel like a dramatic overreaction.

It feels entirely earned.

Rent in Toronto and Vancouver borders on the absurd. Homeownership has taken on the status of a myth. Student loans linger for years, and every few months, another headline asks whether markets, capitalism, or the economy itself still work for anyone under the age of 30.

Against that backdrop, being financially optimistic can sound naïve—or worse, completely out of touch.

But here is a claim worth sitting with: Pessimism isn’t a neutral emotional state when it comes to money. It becomes an active financial strategy, whether you intend it to or not.

The Quiet Choice Most People Don’t Notice They’re Making

Every financial decision you make carries an underlying assumption about the future:

- Investing assumes companies will continue to create value.

- Saving assumes your future self is worth protecting.

- Learning a new skill assumes that economic opportunity will exist tomorrow.

Choosing not to invest—or “waiting until things make more sense”—is also a decision. In practice, it usually means holding cash, staying on the sidelines, and willingly forfeiting the single greatest advantage Canadian Gen Z actually possesses: time.

This isn’t a moral critique. It’s a mechanical reality.

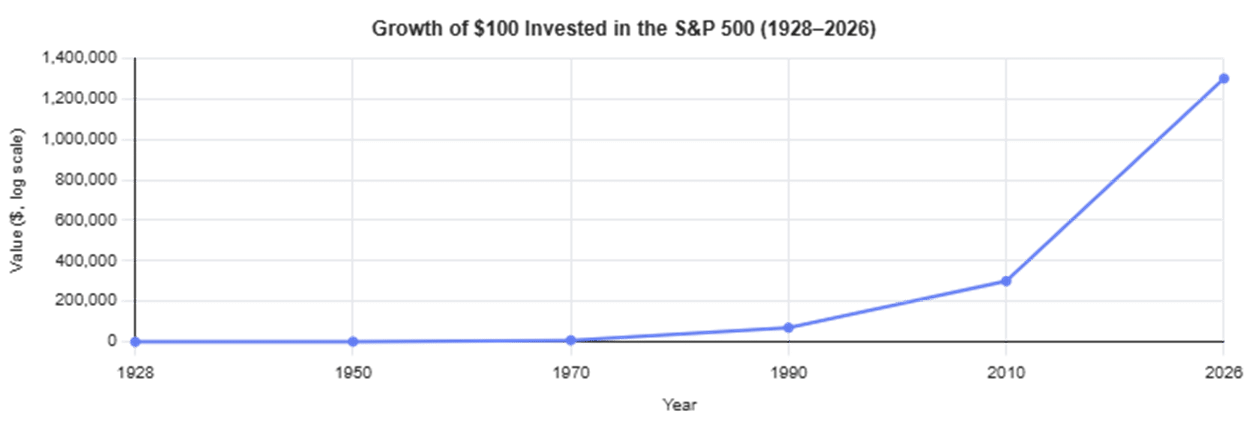

What Long-Term Participation Has Historically Delivered

Chart: Growth of $100 Invested in the S&P 500 (1928–2026)

“Every crisis felt permanent in the moment. None of them stopped long-term compounding.”

This chart isn’t an argument that markets are fair, smooth, or guaranteed. They aren’t. It is an argument, however, that long-term participation has historically outperformed pessimism disguised as caution.

The upward trajectory of global markets has absorbed:

- Two World Wars and the Great Depression

- Stagflation crises and hyperinflation

- The Dot-Com crash and the 2008 Financial Collapse

- A global pandemic

For young Canadian investors, this matters even if you are primarily allocating toward broad equity funds that track global indexes. Our retirement systems, the Canada Pension Plan (CPP), and our domestic capital markets are all hardwired into this exact same long-term growth engine.

“But That Doesn’t Help Me Buy a House”

That frustration is entirely valid.

Canada is facing a structural housing affordability crisis. Pointing to a stock market chart doesn’t lower your monthly rent or magically manufacture a down payment. People don’t live in statistical averages; they live in cities clogged by zoning constraints, immigration backlogs, and severe asset inflation.

Still, there is a vital distinction worth protecting:

- Affordability is a distribution problem.

- Long-term growth is a capacity problem.

They interact, but they are not the same. When we collapse them into one giant problem, we arrive at dangerous conclusions—like assuming that because housing is broken, building a portfolio through equity funds is pointless.

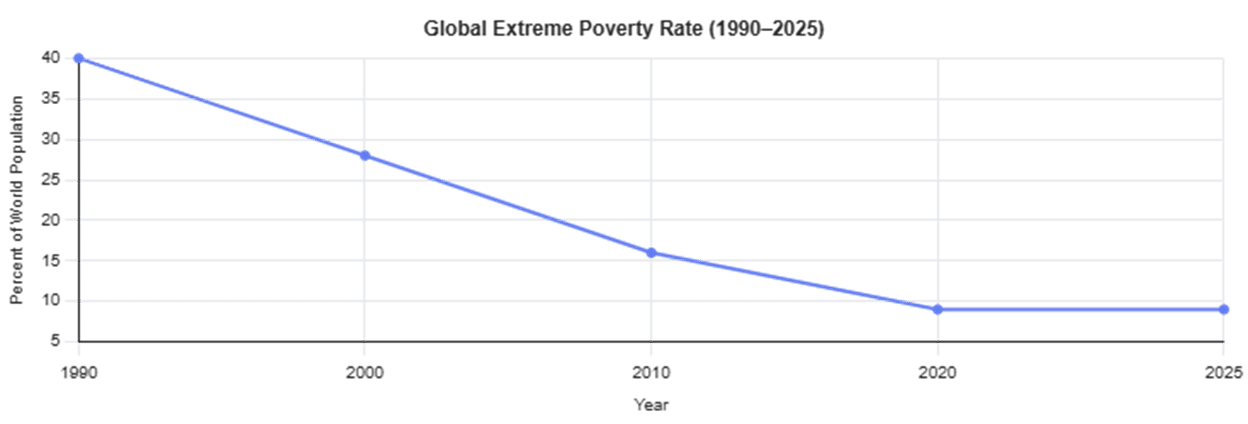

Global Progress Still Matters for Your Local Future

Chart: Global Extreme Poverty Rate (1990–2025)

“Not perfect. Not finished. But directionally clear.”

Over the last few decades, more than a billion people globally have lifted themselves out of extreme poverty. While that progress has stalled at times (such as during COVID-19) and remains deeply uneven, it has not reversed.

Why should a Gen Z investor in Canada care about global poverty metrics?

Because history suggests that housing reform, climate investment, healthcare stability, and wealth redistribution are far easier to achieve in growing systems than in stagnant ones. Shrinking, disengaged economies don’t suddenly become fairer or more just. They become zero-sum games where the powerful hoard what’s left.

The Risk That Pessimism Doesn’t Advertise

The biggest financial mistake young investors make isn’t bad individual asset selection or timing the market.

It is delaying participation because the system feels broken.

It cloaks itself in reasonable-sounding phrases:

- “I’m just holding cash because the markets feel fake right now.”

- “I’m waiting for a total market reset before I get in.”

- “Long-term investing won’t matter for our generation anyway.”

But here is the uncomfortable truth: The markets do not pause while you wait to feel convinced.

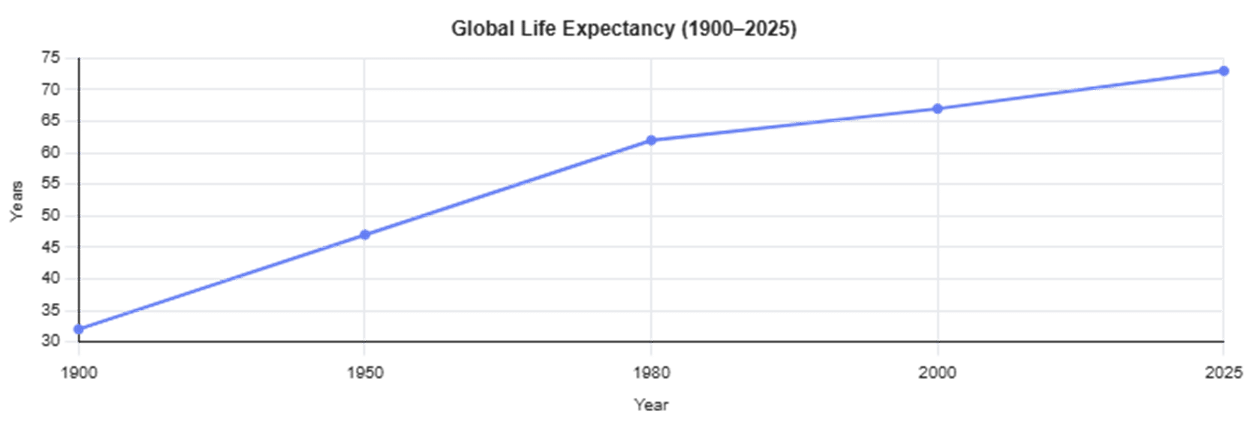

Why Time Horizons Matter More for Gen Z Than Any Generation Before

Chart: Global Life Expectancy (1900–2025)

“Longer lives quietly make compounding unavoidable.”

Gen Z is projected to live longer lives than any cohort in human history. That longevity changes the entire financial calculus:

- Retirement will last longer, requiring a larger nest egg.

- The compounding penalty of opting out early grows exponentially.

- Small, microscopic planning decisions made at 22 compounds into massive leverage by age 62.

You don’t need absolute certainty to act intelligently. You just need exposure over time.

Reframing Optimism for the Realist

Let’s be clear about what financial optimism isn’t. It does not mean:

- “Everything will magically work out.”

- “Just ignore systemic inequality.”

- “Just buy equities and chill.”

A much more useful, battle-tested definition is this: Optimism is staying exposed to positive-sum outcomes without pretending that certainty exists.

In practice, for a young Canadian focused on long-term wealth planning, that looks incredibly boring:

- Automating contributions into broad, low-cost global equity funds.

- Maximizing tax-sheltered asset allocation early through structural tools like the Tax-Free Savings Account (TFSA) and the First Home Savings Account (FHSA).

- Aggressively building career skills alongside your financial capital.

- Treating daily financial news as background noise.

That isn’t blind faith. It’s probability management.

The Glass is Cracked—But Don’t Walk Away

The economic glass is cracked. Some people got to start pouring into it much earlier than you. Canadian housing policy has undeniably failed younger cohorts.

All of this is true.

But treating the glass as completely empty solves absolutely nothing. Opting out entirely guarantees only one thing: that you won’t participate in the upside, while those with capital and a longer perspective quietly do.

Optimism isn’t a personality trait, and it isn’t confidence in a perfect world. It is a strategic decision to act without guarantees—because history shows that disengagement carries a devastating compound interest of its own.

The future doesn’t reward certainty. It rewards participation.

–Sabiha

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.