How to Build a Retirement Plan That Actually Works (and Grows Your Wealth)

Most people go through life and at some point wake up and realize they should be doing something smarter with their money.

When you reach that inflection point, what should you do and what are the few fundamental basics that you need to know?

Many retirement plans are designed to feel safe, instead of giving you freedom.

Safety usually comes at the cost of long-term growth and may mean you never retire with the lifestyle you want.

This is an overview of my philosophy, explains how a financial plan becomes the GPS for your life, how to determine the return you actually need for retirement, and why equities often need to play a larger role than most people expect.

Learn how to think about risk, long-term investing, and when more advanced strategies may be appropriate.

You will learn:

- When you get serious about your money, what is the first thing you should do?

- Why is your financial plan the GPS for your life?

- Why does thinking long-term completely change your life?

- How is an interactive financial plan fundamentally different?

- Why are most advisors’ recommendations like driving with brakes but no gas pedal?

- Why do most people need a significant allocation to equities (stock markets)?

- What do equity investors need to know?

- Why can borrowing to invest be a relatively obvious way to grow wealth for many people?

- What do people who borrow to invest need to know?

- How important is tax planning and when should you do it?

- Why is financial freedom such an amazing time in your life?

When you get serious about your money, what is the first thing you should do?

You want to take your kids for a Disney vacation and drive to Florida. You bought tickets for 2 days from now. You only have 2 weeks for vacation and don’t want to spend 6 days driving back-and-forth.

When you go on this kind of long driving trip, what is the first thing you do when you get into your car? You put your destination into your GPS.

What would happen if you just drive without your GPS? Without your GPS:

– How would you know whether you are taking the optimal route?

– How will you know whether you will get the on time?

– How will you know how fast to drive?

– How will you know how much time you can spend in rest stops and overnight?

Your financial life is similar. The first thing you need is your financial plan so that you know:

– What specifically are your life goals?

– How much money will you need and by when to achieve them?

– Retirement is the biggest goal. What is the retirement lifestyle you want and when?

– How will you know whether you can realistically achieve it by the age you want?

– How will you know the rate of return you will need your investments to make?

– How will you know how much you need to save every year?

– How will you know how comfortable you can live now and still have the future you want?

– How will you know what more aggressive strategies you should consider?

– How will you know exactly what you need to do to have the life you want?

– How can you be confident in your future?

Your financial plan shows you clearly what your future is likely to be and gives you confidence that you will achieve it.

Why is your financial plan the GPS for your life?

Your financial plan is the GPS for your life. You decide on your specific life goals. Make them the life you want to live, but also make them realistically achievable. Figure out exactly what you have to do to live that life.

A proper financial plan should be your financial plan – not for a generic human. There is no right or wrong plan. It is your life.

Your financial plan should be in-depth, including the exact lifestyle you want to live (line by line of your expenses) and when you want to retire. It’s not enough to say you should retire on 80% of your income today, or some other percentage of your income that average people might want. Is that the lifestyle you want to retire on?

Your financial plan changes your thinking to long-term.

Why does thinking long-term completely change your life?

When you think long-term, your life is completely different. You do completely different things. You stop making decisions aimlessly. You stop making decisions one-by-one.

Your financial plan changes your thinking to long-term. You understand how decisions today affect your future. You make decisions today based on the effect they will have on your life decades from now. Your decisions are all coordinated towards your life goals. You are confident that your decisions are the right ones. You are not going to regret them in the future.

How is an interactive financial plan fundamentally different?

An “interactive financial plan” is when you use flexible software to look at a variety of possible options for your life until you find the one that is the life you want to live and that you can achieve.

You see precisely the long-term consequences of decisions today. Your interactive financial plan can show you many possible life options including what you would have to do to achieve them.

For example, you could retire earlier or work longer, work part-time for some years, decide to retire more comfortably with more travel and entertainment, you could downsize your home, you could buy a vacation property, you could invest for more growth, add a growth strategy like the Smith Manoeuvre, or you could add an investment loan.

These are all possible future lives. Which one do you want to live?

Why are most advisors’ recommendations like driving with brakes but no gas pedal?

I have seen the full finances of thousands of Canadians and then helped them set their retirement goals. The majority of them have been investing so conservatively that they have essentially no chance to achieve their retirement goal.

One of the main reasons most retired Canadians are not living the life they really wanted is that they invested too conservatively.

Investment advisors are required to look at your risk tolerance to make sure you do not invest too aggressively. But hardly any do a proper financial plan, so they don’t know how much growth you need to achieve your life goals.

One critical result from your financial plan is that you see the rate of return you need to achieve the future life you want. You still need to be able to tolerate the short-term market fluctuations and bear markets, but your financial plan can help you make sure you don’t invest too conservatively.

Think of your risk tolerance questionnaire as a tool to make sure you don’t invest too aggressively. It’s the brakes. And your financial plan is a tool to make sure you don’t invest too conservatively. It’s the gas pedal.

Since nearly all investment advisors will do a risk tolerance questionnaire, but not a proper financial plan, it is like driving with brakes and no gas pedal.

Picture driving to Disney World in Florida to take your kids and you want to arrive 2 days from now. You get advice similar to typical investment advisors – that your speed tolerance says you are uncomfortable driving more than 50 kms/hr. So you drive very slowly. At that speed, there is no chance you will be in Disney World 2 days from now!

This is part of why most retired Canadians are not living the life they wanted. They had to adjust their lifestyle down to the lower income they get.

Why do most people need a significant allocation to equities (stock markets)?

One big lesson from what I have seen creating more than a thousand comprehensive financial plans for Canadians is that almost nobody can retire with the lifestyle they want if they invest conservatively – like in a balanced portfolio.

A conservative, balanced, or “60/40” portfolio is often considered prudent and the default portfolio by investment advisors, but you can’t really make a financial plan work with it.

For example, if you are 35 and want to retire in 30 years at age 65, and you earn $100,000/year and want to retire on $75,000/year (assuming maximum government pensions and 3% inflation), here are 2 choices to achieve your goal:

You make only 5%/year while the cost of living rises by 3%/year. That is simply not enough growth!

With a balanced portfolio, you would need to invest $50,000 of it! That’s nuts! You make $100,000/year, but bring home only $74.000/year. There is no chance you are going to invest $50,000 of that $74,000.

However, if you can learn to become comfortable with the volatility and declines of an equity portfolio, you should be able to get at least 8%/year long-term. In that case, you only need to invest $19,000/year, which is only slightly more than maximizing your RRSP room. That is not simple, but definitely doable.

Remember: There is a high risk to your retirement plan from owning fixed income investments.

Bottom line: Nearly everyone needs a significant allocation to equities (stock markets) to be able to achieve the future you want.

What do equity investors need to know?

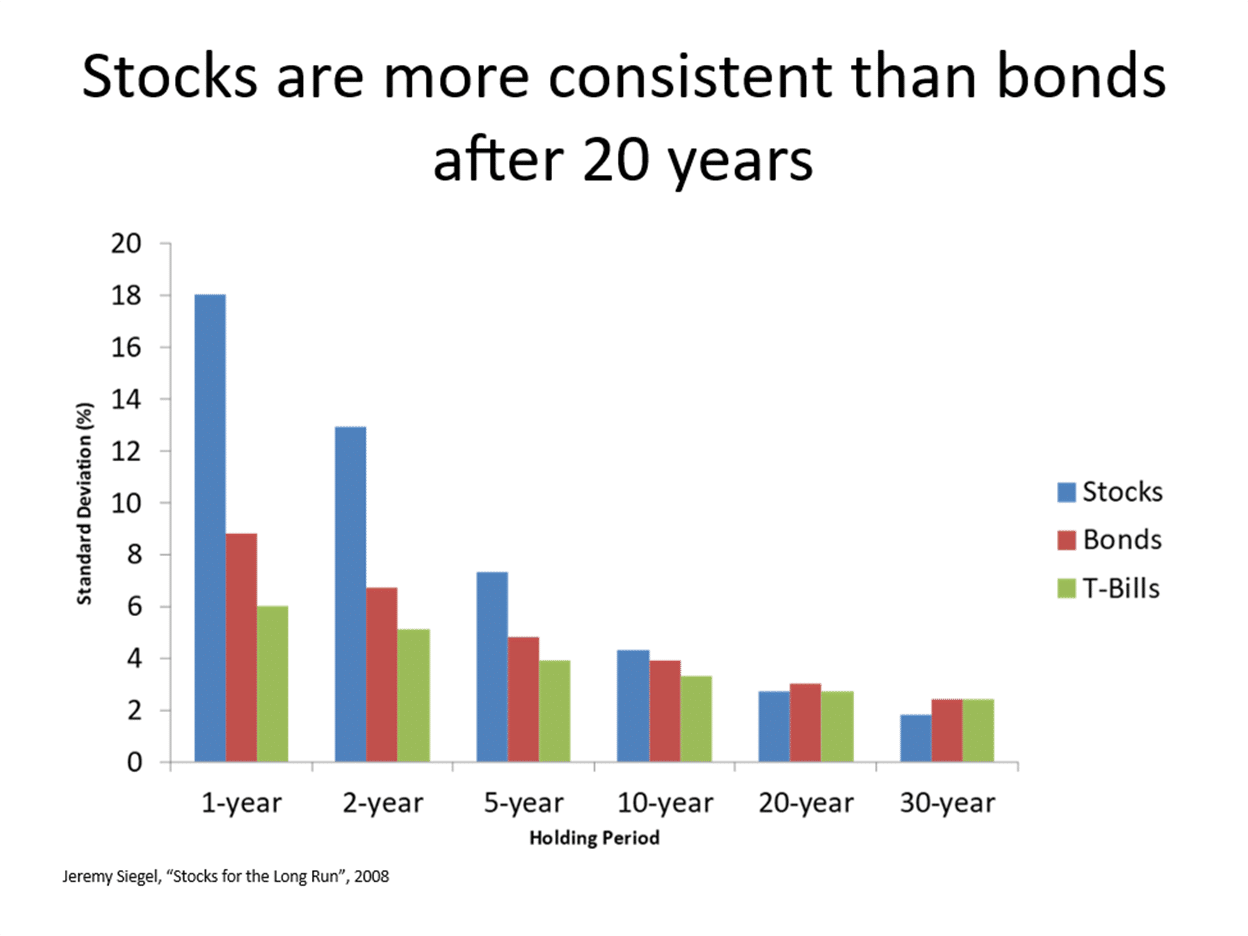

Most people know that equities fluctuate more than fixed income, but few understand that equities are more reliable long-term. The long-term return (20 years or more) for stocks after inflation has been more predictable than for bonds or fixed income.

That may be surprising but was shown statistically by Prof. Jeremy Siegel in his classic book “Stocks for the Long Run”.

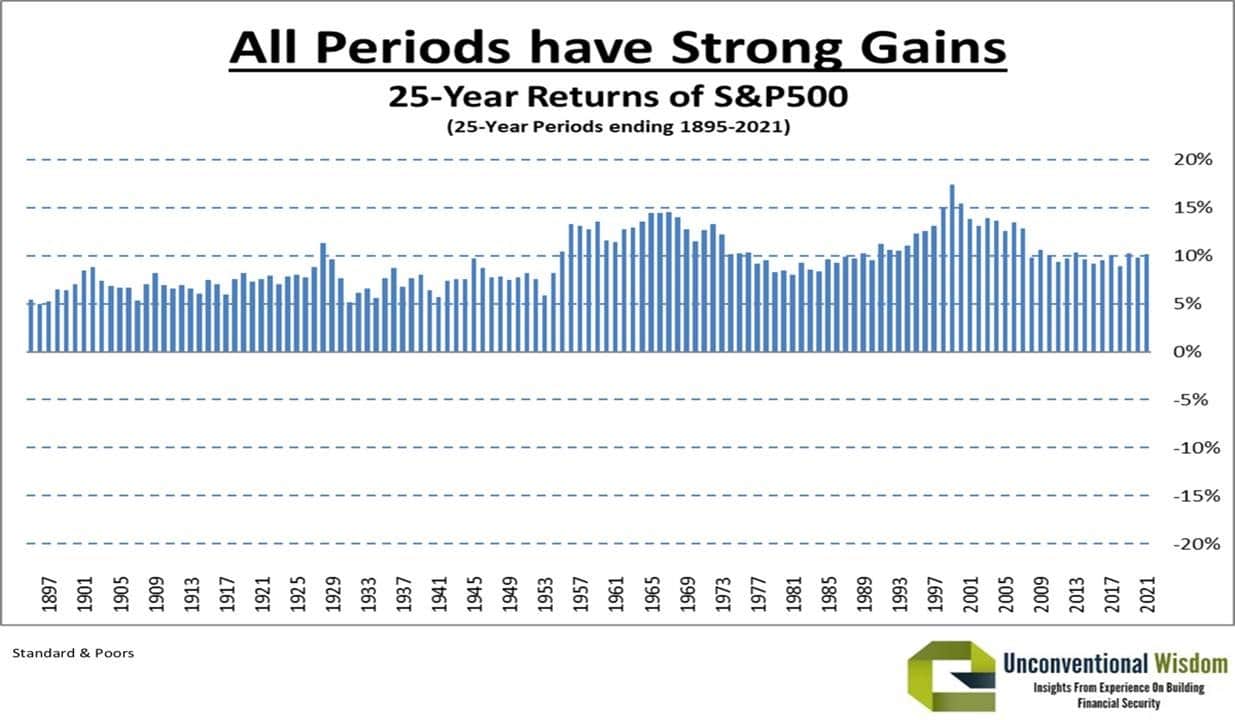

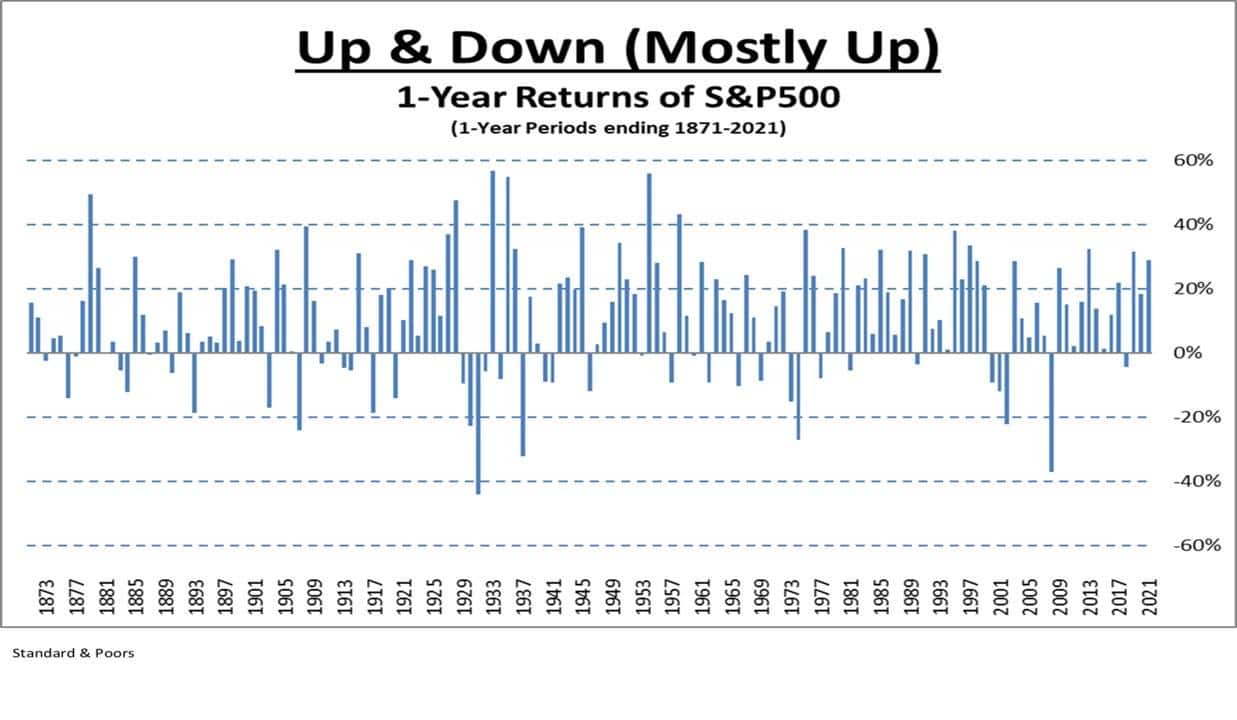

I found a similar result looking at calendar returns of the S&P500 since 1930 (essentially the modern stock market) where the worst 25-year return was 8%/year. That’s a good return for being a worst-case scenario!

The stock market has consistently provided solid growth long-term. After 25 years, the stock market has ranged between being 7 and 17 times higher.

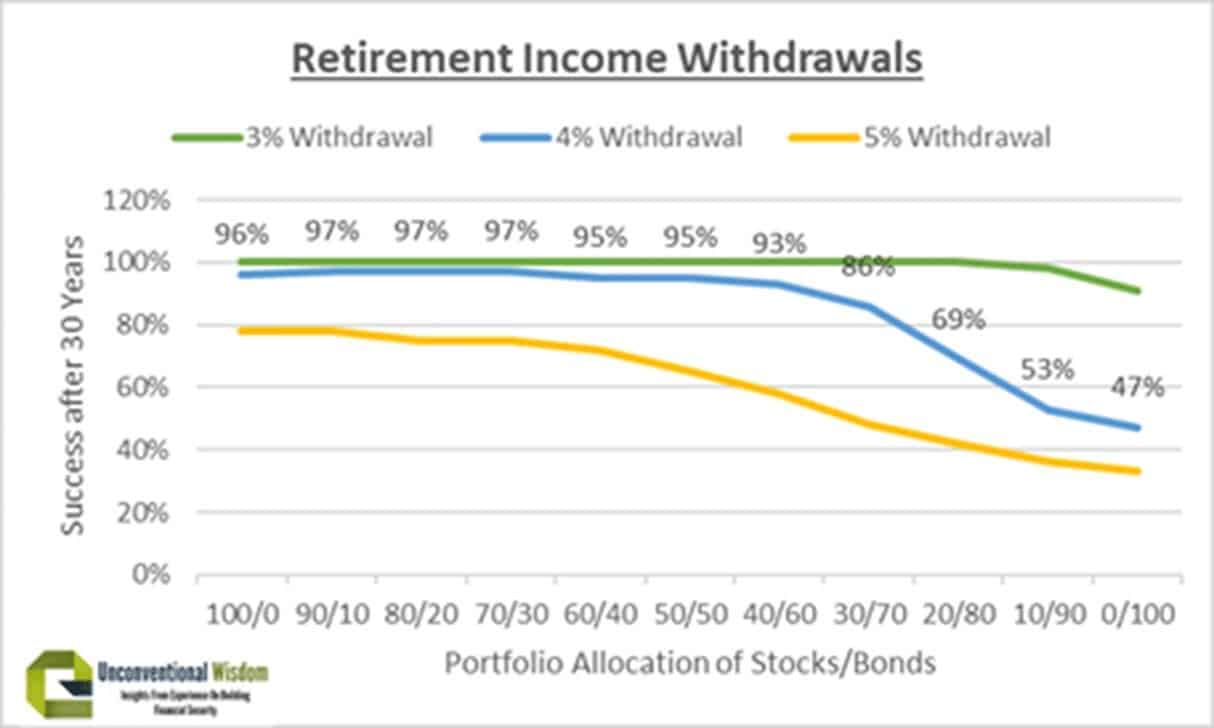

I found in my study that stocks have been more reliable than bonds (fixed income) over a 30-year retirement while withdrawing regularly from them. Using the “4% Rule” of thumb by withdrawing 4% of your starting portfolio in year 1 of retirement and then increasing it by inflation, a portfolio of 70-100% equities successfully provided the income for 30 years 97% of the time, while a 100% bond portfolio (most conservative portfolio) provided it only 47% of the time.

Stocks provided a reliable retirement, while fixed income failed more than half the time to provide for a 30-year retirement!

Of course, stocks fall a lot sometimes. They generally fall 30% or more a couple times per decade and 40% or more on average every few decades. The largest declines tend to be roughly 50%.

However, the stock market has recovered from 100% of declines – with 88% of declines being recovered in 1 or 2 years.

The secret to effective stock market investing is to stay invested long term. You need a higher risk tolerance – but risk tolerance specifically means: “The ability to do nothing when your investments go down.” You probably have the ability to do nothing!

The reason fixed income is less reliable is that it often makes less than inflation – and sometimes for decades at a time! In periods of high inflation, such as the 1970s and 1980s, bonds suffer a large permanent loss after inflation.

The issue is that you need an income that rises by inflation every year – not a fixed income.

In short, fixed income is reliable short-term, but risky long-term. Stocks are risky short-term, but reliable long-term.

I don’t know where the stock market will be next year, but I am confident that 25 years from now it will be between 7 and 17 times what it is today.

The mindset you need to invest effectively in equities:

– Successful investing is goal-oriented.

– Any market decline of 20% or more is a great buying opportunity.

The 3 principles of successful investing:

– Faith, patience and discipline.

– Faith that equities will provide a solid long-term return.

– Patience to stay invested.

– Discipline to stick with your financial plan.

Why can borrowing to invest be a relatively obvious way to grow wealth for many people?

If you are comfortable investing 100% in stocks and will stay invested for the long-term, then borrowing to invest often seems like a relatively obvious way to make a lot more money. It’s called investing with “other people’s money”.

You borrow at lower interest rates, perhaps 4-5%, and the interest is tax-deductible every year. You invest it in the stock market that long-term have averaged 10-11% with the worst 25-year return of 8%. The stock market gains are capital gains, which are taxed at lower tax rates and only when you sell, which could be years from now.

The interest payments are a flat number, while your stock market investments grow exponentially over time.

For example, a common strategy of borrowing to invest is the Smith Manoeuvre. You borrow against your home equity bit-by-bit as you pay down your mortgage. You replace your mortgage with a tax-deductible credit line over time. The credit line also pays its own interest. Your total debt stays the same.

This process converts your mortgage to a tax-deductible credit line over time without using your cash flow. Your net gain after tax from this process as you pay off your mortgage over 25 years with typical stock market returns is roughly the value of your home today.

What do people who borrow to invest need to know?

Borrowing to invest is not for everyone. You have to know that you will be able to stay invested for the long-term especially when your investments are down. You have to be able to make the interest payments even if your life has major problems. You can use your investments to help with the payments, if necessary, but it’s best not to rely on that for a long time.

However, borrowing to invest is probably the most powerful wealth-building tool. Nearly all wealthy people borrowed to invest in the stock market (many companies) or their own company.

The wealthiest people are usually the ones with the most debt. But it’s good debt, not bad debt. It was borrowed to invest in higher growth investments, not borrowed to spend on consumer items.

How important is tax planning and when should you do it?

There are all kinds of ways to save tax by arranging your finances in the optimal way. It can make a huge difference in your life, especially when you do it consistently year-after-year.

For example, planning based on tax brackets can give you the largest tax refunds when you make contributions and cost you the least tax when you withdraw it. Stock market investments are taxed more favourably and often years later than fixed income investments. Borrowing to invest in tax-efficient investments can give you large tax refunds in most years.

However, the advice is: “Never let the tax tail wag the investment dog.”

In other words, don’t do things just for the tax savings. Make solid decisions for how to plan your finances and choose high quality investments – and after that consider how to plan to save tax with it. Don’t start with saving tax and base your finances on that.

Why is financial freedom such an amazing time in your life?

Planning your finances and your retirement can be complicated and takes some effort. Many people feel intimidated by it. Is it worth it?

One of the most satisfying parts of my career has been seeing long-term clients retire comfortably with more than enough money to confidently live the life they want no matter how long they live.

A long-term client told me: “With Ed’s knowledge and vision, he has shown how his plan can generate the additional income per year throughout our retirement years. And THAT, in short, is the difference between penny pinching “golden years” or the freedom to finance all the plans we had already made, but for which we didn’t really know if the money would be there or not.“

When you are financially free and have both money and health, life can be truly awesome!

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.