Living Healthy Past Age 100 – Will Your Retirement Plan Survive?

Last week, I revealed my longevity journey, introduced some of the explosive developments, and why we may be able to start living significantly longer within the next 10–20 years.

Living with health and vitality past age 100 could become common.

What happens to your money if that happens?

If we live 20 more years, can we actually be retired for those 20 years?

How much more would we need to save—or how much longer would we need to work?

In my latest video and blog post, you’ll learn:

- Why would we want to live decades longer?

- Would it be good for society?

- How much more would you have to save to be retired 20 more years?

- How many more years would you need to work?

- How are these different depending on the allocation of your portfolio?

- What is likely to happen to CPP, OAS, company pensions and annuities?

- What is likely to happen to life insurance?

Why would we want to live decades longer?

Only 29% of people want to live to age 100, based on a 2025 PEW study.

Why so few?

What is your picture of people age 100? Feeble, sick and with dementia? That’s why only 1/3 want to live to 100.

However, if they would be healthy, 74% want to live to 120 or longer.

The important issue is not just how long we live. It is how long we are healthy.

Healthspan – not lifespan.

Would it be good for society?

First of all – it already happened. Average life expectancy from birth in 1900 was age 48, in 1950 it was 68, and today it is age 83. That is 20 more years between 1900-1950 and 15 more since then.

A big reason is that our quality of life is much better. We eat better with more protein, have vaccines for many major diseases, and have better medicine like antibiotics.

But a lot of it is that a lot fewer deaths during childbirth average it down.

For an average life expectancy of 80, one death in childbirth would require 4 people to live to age 100 to offset it.

Average life expectancy from birth is a flawed number, dragged down by deaths of children.

The median age when older people actually died was about 78 in 1900, 83 in 1950, and 90 today. So we are living more than 10 years longer already.

We are also healthy longer. Anecdotally, 70-year-olds are like 60-year-olds in 1950.

And 80-year-olds are like 70-year-olds in 1950. 80 is the new 70.

Living longer has contributed to better lives for us so far.

There has been debate about whether living longer healthy is good, but the effects should be mainly very positive for several reasons:

1/ More years at peak productivity.

Most companies today suffer from a shortage of skilled, knowledgeable employees.

Most people are most effective in their careers in their 50s and 60s and have extensive knowledge and experience when they retire. If they are still healthy and vibrant, then having people work longer is a big boost for productivity.

2/ Help to avoid underpopulation.

Many people fear that we will have overpopulation, but that is not expected to happen. The world population is about 8 billion and expected to rise to about 9.5 billion by 2050, but then start declining rapidly because of falling birth rates. Most developed countries today have too few births to maintain their population. It is mostly the developing countries that still have high birth rates, but as they develop and get closer to the middle class, their birth rates are expected to be much lower. Economies work much better when the population slowly rises than when it falls. We will need people to be productive longer.

3/ Grandparents knowing their grandchildren and great grandchildren, and being able to mentor them.

It is grandparents that often keep families together.

4/ I should add that it is important to be optimistic in life. Optimism is realism. And optimists live longer.

In most of the important ways, the world is dramatically better than 100 years ago. Many people are pessimistic today because of a political belief or fear of a warmer world or running out of resources. However, look at how much our lives have improved the last 100 years! Human ingenuity continually makes our lives better.

Remember the famous quote by Thomas Macaulay: “On what principle is it that with nothing but improvement behind us, we are to expect nothing but deterioration before us?”

How much more would you have to save to be retired 20 more years?

Let’s get into the details. A specific example shows the effect of living healthy longer.

Lonnie is 30 and plans to work till age 60 and then be retired to age 80, earning $100,000/year and wanting to keep the same income & lifestyle through retirement. Lonnie finds out about all the new methods to live healthy longer and now expects to retire at 60 and be retired to age 100 with the same lifestyle.

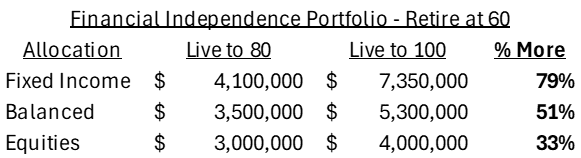

How big a portfolio will Lonnie need at age 60 to afford the desired retirement for 40 years vs 20 years? It depends on the investment portfolio allocation. Here are the needed portfolios. It comes down to needing to save 33% more for equity investors, 50% more for balanced investors and 80% more for fixed income investors.

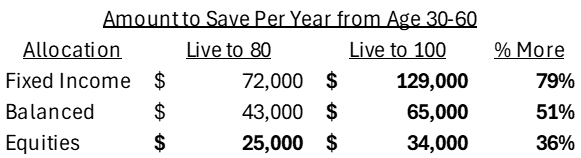

How much more does Lonnie need to save per year from age 30-60 to support the extra 20 years of retirement? Here are the amounts Lonnie would have to save & invest per year. The percent additional savings is the same – 33% for equity investors, 50% for balanced investors, and 80% for fixed income investors.

Those numbers may look large, so let’s put them into perspective for someone earning $100,000/year.

For equity investors, saving $25,000/year is just maximizing their RRSP + TFSA room. $34,000/year could include FHSA contributions or investing a bit more than the tax refunds into a non-registered account. For equity investors, it is not easy, but doable.

For balanced or fixed income investors, it is not really possible. Earning $100,000/year, you bring home $75,000/year, or $80,000/year including your RRSP tax refund. To invest $65,000/year as a balanced investor or $129,000/year as a fixed income investor is impossible!

I have shown this in other videos. Balanced and fixed income investors need to expect a lower standard of living when they retire. Maintaining the same income as when they worked is probably impossible.

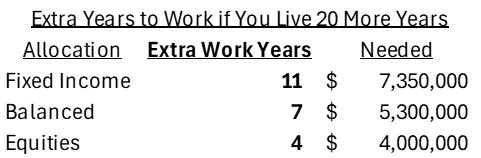

It would be awesome to be retired and healthy for 40 years or more – wouldn’t it! However, the more likely scenario is that people will save the same as they did each year, but will have to work longer. If you live 20 more years, how many of those years do you have to work and continue to save to pay for your retirement? Here are the portfolios needed at retirement and the extra years of work while continuing the same savings.

Equity investors can work & save 4 more years and enjoy retirement for the remaining 16 years. Nice! Balanced investors can work 7 more years and enjoy 13 years. Decent. Fixed income investors would have to work 11 more years and enjoy retirement for only 9 more years.

All this clearly shows the massive advantages of investing in equities for the long-term. It is worthwhile becoming comfortable with equities. They are volatile and fall a lot sometimes, but recover and have historically provided reliable high returns over long periods of time like 20-30 years. I have a bunch of posts showing the results from history.

What is likely to happen to CPP, OAS, company pensions and annuities?

Pensions will have a big problem if they get the same contributions but have to pay out pensions for 20 more years.

For CPP, if the official retirement age stays the same, it will have to raise contributions. Today, contributions are 12% of your income (6% from you and 6% by your employer). To pay for 20 more years, they would have to rise to about 16% of your income (8% each).

OAS has no retirement portfolio. It is just a redistribution system with younger people paying taxes that go to OAS pensions. It costs the Canadian government about $80 billion/year. If we were retired twice as long, that is an additional $80 billion/year. With the government already forecasting a deficit of $80 billion/year (government expenses more than all tax revenue), doubling it is not sustainable. All of the additional OAS would have to be borrowed every year.

OAS could reduce the payouts, but that is unlikely. OAS would have to increase the starting age to later than age 65. Actuaries have already been saying we need to increase it, since we are living a lot longer than when OAS was created in 1952. Stephen Harper had implemented the first step of the needed reform increasing the start age to 67 over time. However, Justin Trudeau reversed this progress and put it back to 65. The best estimate is that OAS should already start at close to age 70.

OAS is likely not sustainable. When it was created, there were 16 workers for every retiree. Today, there are only 3 workers and that is expected to be only 2 workers per retiree in 2050. That is without us living decades longer. We have told thousands of young Canadians that OAS will likely not be there when they retire and nobody has ever questioned it. Keeping the cost level similar to today, the starting age for OAS likely needs to rise to about age 72.

Employer pensions are structured by actuaries and will be set up to be viable and profitable for the employer and pension firm. They will have to reduce the pension, increase the contributions, or set the pension start age later. All 3 or a combination are likely.

Today, very few companies in Canada can afford defined benefit pensions, other than the government. With a defined benefit pension, the employer is taking the risk of having to pay you as long as you live. The way the pricing is set by actuaries and auditors, makes them unaffordable. Most companies have already converted to defined contribution pensions, which are essentially group RRSPs with the employer matching, or partially matching, your contributions.

To be clear on the difference, a defined benefit pension means the pension benefit is defined by a formula, like government pensions. You don’t know how much money is in the pension. A defined contribution pension means the contribution is defined, like with a group RRSP. You see an investment account. The retirement income it will provide is not defined.

Note that for equity investors, defined contribution pensions are a good thing, as long as your employer maintains the same contribution. If you and your employer contribute the same, investing in a group RRSP or DC pension into equities should provide a higher retirement income for life than the defined benefit pension.

The news always seems to be bad for balanced and fixed income investors. A group RRSP would mean lower retirement income than a defined benefit pension, which is essentially invested in a balanced portfolio.

Annuities are thought of as being like lifelong GICs. They are really the same as a pension, except you own it, not your employer. Pricing is set by actuaries to be viable for the insurance company. The cost to buy them will have to be higher or the payouts will have to be reduced if the insurance company has to pay you for 20 more years.

What is likely to happen to life insurance?

Living decades longer is great news for insurance. Lifelong insurance policies, such as “term to 100”, universal life or whole life policies, will be able to reduce their premiums. They can pay you 20 years later. The premiums are also set by actuaries to be viable for the insurance company. Term insurance is likely unaffected.

What is your why?

What’s your why? You need a reason to live decades longer to make it. Is it to be productive longer, have decades more of a fun retirement, or seeing your great grandchildren grow up?

Personally, I’m very excited about being able to live healthy decades longer!

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

Hi Ed

Great post, thanks for sharing. I’ve read plenty of 60/65+ case studies and most of them seem quite vanilla with a few personal nuances.

Do you have any aiming to retire at 45 studies? (average Canadian family not looking at eating cup noodles for life).

Curious to know how that looks for a young/ish family which adds a very different uncertainty factor over decades longer including RESP drawdown plus the usual OAS/CPPs and non-reg withdrawals.

If not, would love to volunteer.

Rick