Retirement Tax Shock: Why Many Canadians Pay More Tax Than Expected

Most Canadians expect to be in a lower tax bracket in retirement.

But many end up paying more tax than they expect.

How do tax brackets change after age 65 and why can common assumptions about RRSPs and retirement income lead to higher lifetime taxes?

Here are practical strategies to reduce tax over time, including how to use RRSPs, TFSAs, income timing and how to plan for a tax-efficient retirement.

This might be a real eye opener for some people because I think a lot of people that do some basic tax planning are doing it all wrong.

In my latest video, podcast episode, and blog post I’m going to give you tax planning made easy using tax brackets. Some basics of tax brackets, and briefly how tax planning is done, so you can get the concept.

Then we’re going to talk about why tax brackets for seniors are way different than you think – and how this completely changes tax planning. And how to plan for low tax through your retirement.

You’ll learn:

- Tax planning made easy using tax brackets.

- Why are tax brackets for seniors way different?

- What are the three main clawbacks on seniors?

- What are the actual effective tax brackets for seniors?

- How is tax planning very different with the actual effective tax brackets?

- Which is better for you – TFSA or RRSP?

- How can you plan for your retirement income to be taxed at only 22% or less?

- How does your financial plan become the GPS for your life?

Tax planning made easy using tax brackets.

– Much of tax planning is based on marginal tax brackets. These are the tax on the next dollar of taxable income – which is different from the average tax rate you pay on all your income.

– Tax planning is about being able to plan for or control your taxable income. You can plan ahead to see what it will be or often you can control it based on decisions you make about your income or tax deductions.

– For example, if you have a corporation, you can decide how much salary or dividend to withdraw from your corporation. If you are contributing to RRSP or TFSA, you can decide how much to contribute to which and how much to deduct on your tax return.

– Your taxable income can be very different from your cash income – especially if you are self-employed, have a corporation, or are retired. For example, you pay no tax on cash you withdraw from your TFSA and only pay tax on any capital gains triggered when you withdraw from non-registered investments.

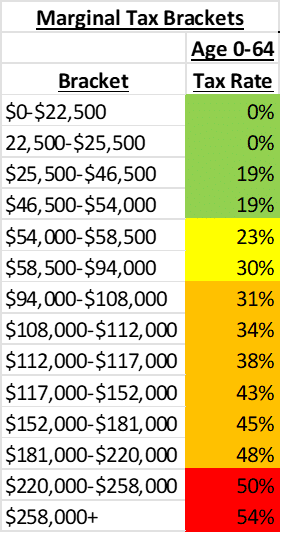

– Here are the basic tax brackets before age 65:

– Let’s look at some tax planning ideas based on tax brackets.

– When you have options on income, try to keep your income from being taxed at higher tax brackets. When you have options on deductions, try to get the largest refund by trying to keep your deductions from giving you refunds based on lower tax brackets.

– Example 1: Business owner can decide how much to withdraw from his company. Try to make it $54,000 to have all of it taxed at 19% or less. Or make it $117,000 to avoid paying 43% tax or more.

– Example 2: If you are deciding between contributing $10,000 to RRSP or TFSA and you have a salary of $65,000, contribute $3,500 to TFSA and $6,500 to RRSP to get a 39% refund on all of your RRSP contribution and avoid getting only a 23% refund.

– Note that actual effective tax brackets for parents can be dramatically different because of the clawback on the Canada Child Benefit. I have a video with details.

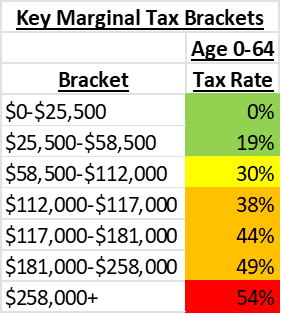

– Focus on the tax brackets that are a large tax increase from the previous bracket and the brackets that cover a larger range of income. Here are the main brackets to focus on:

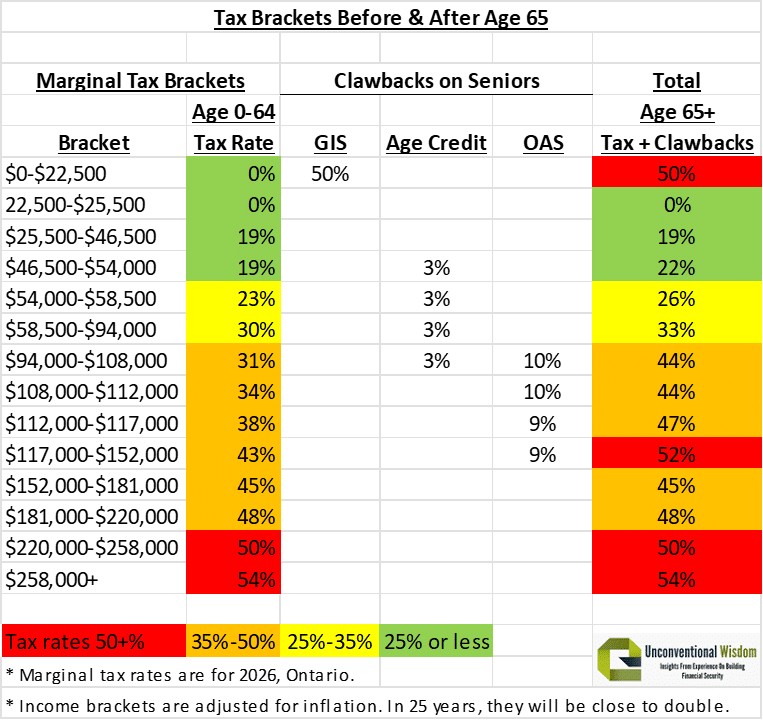

Why are tax brackets for seniors way different?

– Seniors have many government benefits clawed back based on their taxable income. These are exactly the same as a tax. It is the government taking money from you based on your taxable income.

– The 3 main clawbacks are the GIS clawback of 50% on low-income seniors, the age credit reduced by 15% for middle income seniors, and the OAS clawed back by 15% for higher income seniors.

– Note how tax brackets change when you include the clawbacks. These are for a single person and are different for married:

What are the actual effective tax brackets for seniors?

– Tax brackets after age 65 are way different than before.

– The GIS clawback is massive, the age credit clawback is small, and the OAS clawback is relatively large.

– People with a very low income below $22,500 are in a 50% tax bracket! One of the highest.

– Most seniors with incomes up to $152,000 will be in a higher tax bracket if they retire with the same income they had before they retire.

How is tax planning very different with the actual effective tax brackets?

– You save for retirement with one set up tax brackets, but then you have a different set after you turn 65 with higher tax brackets.

– For example, people with very low incomes may contribute to an RRSP and get a 19% tax refund, but then pay 50% tax in lost GIS income after they retire. In that case, the RRSP was a bad idea for them.

– Most incomes up to $152,000 are taxed at higher brackets after age 65. If you expect to retire close to the income you have before age 65, then you need a closer look at your current taxable bracket and the tax bracket you expect to be in after you retire to make smart decisions, such as about your RRSP contributions. For example, people making $110,000 and retiring at the same income would get a 34% tax refund when they contribute but pay 44% tax when they withdraw years later.

Which is better for you – TFSA or RRSP?

– You can invest the same in both and you are not taxed on either for investments while you hold them inside the RRSP or TFSA. The difference is your marginal tax bracket when you contribute vs. when you withdraw. If you will withdraw at a lower tax bracket, then RRSP is probably the best strategy for you. If not, then TFSA is probably better.

– For example, many people get a 40% refund when they contribute and then withdraw decades later paying only 20% tax. Then RRSP is a good thing for you and better than TFSA.

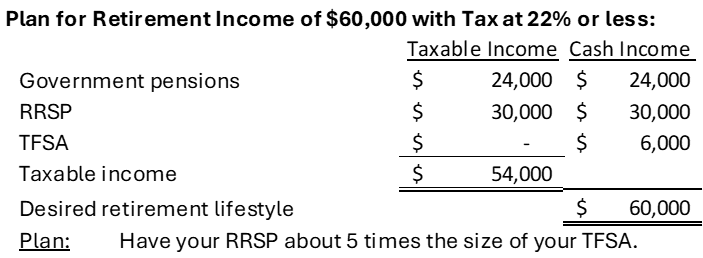

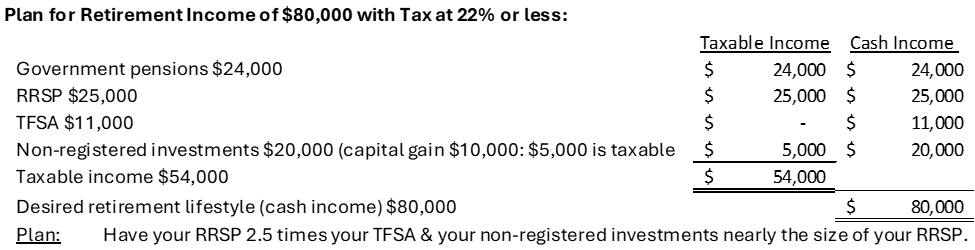

– Most Canadians can plan to pay only 22% or less on their retirement income. If your taxable income before you retire is over $54,000, then you are in a higher marginal tax bracket.

– The general rule of thumb is that people with taxable incomes over $58,500 should usually contribute to RRSP and those with lower incomes should usually contribute to TFSA.

– There are many exceptions to this, though. For example, very low-income seniors with little or no retirement savings should contribute to TFSA, instead of RRSP, since they may lose 50% GIS income on RRSP withdrawals after they retire. People who expect to retire with the same income as before they retire should probably focus on TFSA, as well.

– The only way to know what your tax bracket is now and what it will be after you retire with the lifestyle you want is with a Financial Plan. It figures it out for you and shows you how to plan for the life you want.

How can you plan for your retirement income to be taxed at only 22% or less?

– The important point is not what your taxable income is, but what you can plan it to be. This can be very different from your cash income – which is your lifestyle.

– For example, you can pay 22% or less on all your income if you retire with a taxable income below $54,000.

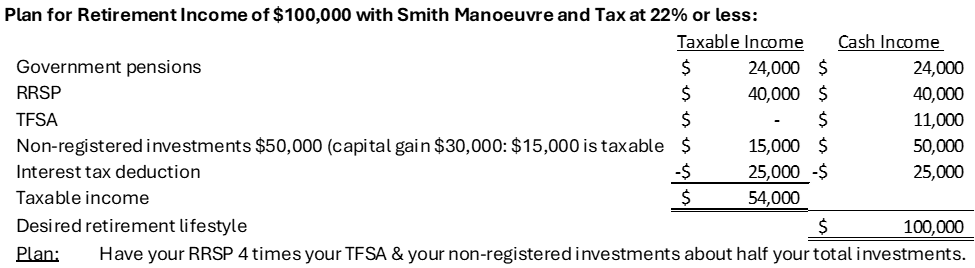

– Here are 3 examples of how to structure your retirement income to all be taxed at 22% or less:

– How do you get non-registered investments? Most people only contribute to RRSP and TFSA, since it is a challenge just to maximize your contribution room for both. However, some people are big savers and save much more than the limits. The extra savings that are not RRSP or TFSA are all non-registered.

– Many people also use strategies of borrowing to invest, such as the Smith Manoeuvre. If you maximize the Smith Manoeuvre, you can typically have non-registered investments as large as your RRSP and TFSA. This is true even though you contributed your cash flow to RRSP and TFSA, since the Smith Manoeuvre generally does not require your cash flow.

– The Smith Manoeuvre also gives you a tax deduction, which might be your only tax deduction after you retire.

– This example assumes that you use “self-made dividends” for your retirement cash flow from your non-registered investments. “Self-made dividends” just mean you sell a bit of your investments each month to give you the exact amount of cash flow you want. You pay tax only on any capital gains you triggered. This allows you to continue to invest for growth through your retirement and focus on triggering as little taxable income as possible. Focusing on deferred capital gains that are triggered when you eventually sell over time is the most tax-efficient way to structure your retirement income.

– Self-made dividends are better than ordinary dividends in every way.

– Many people think you need to invest for income after you retire. You don’t. You need cash flow, not income.

– Many dividend investors think they are paying the lowest tax, but they almost always pay more than with self-made dividends. I have a video with details: Dividend Investing Perfected with Self-Made Dividends .

How does your financial plan become the GPS for your life?

– To eventually be financially free living the lifestyle you want and an optimal lower taxable income, you need a Financial Plan.

– Rough estimates in your head can easily be far wrong and may lead you to make wrong decisions from not knowing your future tax bracket.

– You have many options for how to live your life now and after you retire, plus many possible decisions on how to structure your finances. Therefore, you need an “Interactive Financial Plan” where you look at a wide variety of options while deciding on how you actually want to live. You need to be able to see very quickly what effect various life decisions will have on your future life and your tax.

– Your Financial Plan is the GPS for your life. The first thing you do when you start a trip is put your destination into your GPS so you know exactly the best way to go. Life is the same. The first thing you should do is get your Financial Plan so you know exactly how to achieve the life you want.

– Make it your goal – not something you think people typically end up with.

– Life feels completely different when you are financially independent. You are free to make whatever life choices you want.

– Live life intentionally. Real freedom is financial freedom.

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.