Who Are the Wealthy and How Did They Get Rich?

As a financial planner, I’ve had a unique view into the full financial picture of thousands of Canadians and have read countless studies.

My experience spans clients of varying financial backgrounds, as well as countless conversations with readers of my blog, friends, and acquaintances.

Although our clients may not represent the entire population—they tend to have higher incomes, are growth-focused, and always work with a clear plan—my broad exposure has helped me form a solid understanding of what wealth really is and the common ways people achieve it.

In my latest blog post, YouTube video and podcast episode, I’ll cover some key questions that get to the heart of wealth.

You’ll learn:

- How much do you need to be “wealthy”?

- What do media stories get wrong about the wealthy and the poor?

- Why are people with high incomes different from people with high net worth?

- Is a high income important to become wealthy?

- Do most wealthy people inherit their wealth, or do they grow it themselves?

- What types of people have high net worth?

- What does the Lifecycle Investing study tell us about growing wealth?

- How can you become wealthy?

Let’s explore these points to help you understand how wealth is built and why the reality may differ from what’s often portrayed.

How Much Do You Need to Be “Wealthy”?

“Being wealthy” isn’t about a specific income level.

To me, it’s about having enough investments to sustain your desired lifestyle without needing to work if you choose not to.

For financial independence, I suggest aiming to have investments that provide 20% more than what you need for your ideal lifestyle, just as a buffer.

Once you reach about 50% more than your goal, that’s when you can feel truly “wealthy.”

This amount allows you to live without financial worries and gives you the freedom to pursue what you want.

However, it’s essential that these investments are productive assets—assets that grow reliably over time.

Many Canadians count their home as part of their wealth, but unless you plan to use it as retirement income (by downsizing, renting, or leveraging through strategies like the Smith Manoeuvre), your home may not be a productive financial asset for the future.

What Do Media Stories Get Wrong About the Wealthy and the Poor?

There’s often confusion about the difference between income and wealth in media portrayals.

Many media stories talk about the top or bottom 20%, 10% or 1% yet these stories highlight income differences rather than net worth.

True wealth is about net worth. Being wealthy means high net worth, not high income.

Income statistics are also often questionable.

They are often salary and wages only, often excluding government programs received by low income people, investment income received by high income people, and income tax paid mostly by high income people.

Income stats are usually for households, where the lowest 20% are often a single person while the highest 20% is usually a couple. Income stats often compare single people with couples.

Net worth official statistics are questionable. Many assets that are hard to value, such as a business, property overseas, investments inside a corporation or a trust.

Media stories use statistics that use averages, which often don’t reflect actual people.

For example, 2 large low income groups – students with a net worth of zero and seniors with a net worth of $1 million have an average net worth of $500,000, which does not represent either group.

Why Are People With High Incomes Different From People With High Net Worth?

It’s common to assume that a high income equates to wealth, but the truth is more nuanced.

Take two groups:

Who is wealthy?

A couple earning $200,000/year, but with no savings (net worth of zero). E.g. Recent university grads with student loans.

A couple earning $30,000/year, with a net worth of $1.6 million. E.g. Seniors with a paid off home. “Millionaires in poverty.” 75% of seniors own a home and most are paid off.

The high-net seniors are technically wealthier, yet income-focused studies might miss this group’s financial security. It’s a reminder that a high income can certainly help, but it doesn’t guarantee wealth.

Is a High Income Important to Become Wealthy?

While having a good income can ease the path to saving and investing, it’s ultimately how much you save that matters.

It’s definitely important to have a good income, since you need a productive profession or skills, and it’s easier to save if your income is higher.

However, income for the top 20% is not much in Toronto.

There are many exceptions. For example, doctors are widely known to have the lowest net worth based on their income. They tend to think they should live a doctor’s high lifestyle and spend most of their income.

Chart: Higher net worth people tend to have higher incomes.

What Kinds of Households Have Different Income Levels?

Household income varies across different life stages.

People with low incomes, not working or only part-time are often in a high-income household.

General rule of thumb: Top, middle, and bottom 20% are mostly the same people at different times in their life.

Only a small percent of people stay in their income group most of their life.

Bottom 20%: Income below $30K/year. The ones I see are mostly students & seniors. Stats Canada says students & seniors are the most likely groups to be in the bottom 20%. Quite often single people and not working full time. A single person at minimum wage working full time is $34,000/year, which is already above the lowest 20%.

2nd lowest 20%: Income $30K-$55K. 20s & 30s early in career, or the same people but now with a partner.

Middle 20%: Income $55K-$90K. 30s & 40s early or mid-careers. Could be a minimum wage couple with both working full time.

2nd highest 20%: $90K-$150K. Often the same people in their 50s & 60s late in their career. Have received raises for years or promotions, or changed jobs to higher income.

Top 20%: Income $150K+. Valuable skills & professions. Professionals (especially doctors & engineers), IT specialists, salespeople, or business owners of most ages 30-65. Productive degrees in STEM fields. Or tradespeople with a small business.

Also, many people with one year of high income. A significant percent of people are in the top 20% for only 1 or 2 years. For example, they sell a rental property or a business, or receive a severance.

Seniors: Back down to lowest or 2nd lowest 20% again in most cases. Most Canadians don’t save nearly enough to retire comfortably.

Interestingly, people don’t stay in one income group for life; they often shift depending on life events like career changes, marriage, or retirement.

This dynamic nature of household income is why lifetime financial planning is essential.

Do Most Wealthy People Inherit Their Wealth, or Do They Earn It?

Contrary to popular belief, few wealthy Canadians inherited their wealth.

The majority are self-made millionaires and billionaires built their wealth through hard work, saving, and investing.

E.g., Warren Buffett, Elon Musk, Bill Gates, Mark Zuckerberg, Larry Page & Sergey Bryn from Google, Jeff Bezos from Amazon.

If you look at the Forbes 400 – only 13% inherited it, and 87% made it themselves.

Classic stories: 1st generation makes wealth. 2nd generation maintains it. 3rd generation loses it. E.g., Eaton family.

I know a story of meeting the grandson of the owner of a huge business with a household name.

He is moving in with a roommate out west because he cannot afford his rent in Toronto. His grandfather had a partner and a bunch of kids, so he only received a small portion. Now the cost of living is high and he spent most of it. This story is the norm.

In fact, even those who inherit typically don’t see that money until later in life, when they are already in their 60s or 70s, as 50% of the couple, often one reaches age 94. Most inheritances don’t happen until the second parent dies.

Most people want to enjoy their wealth and leave a bit for their kids. Few plan for intergenerational wealth.

Warren Buffett’s advice: “I will leave my kids enough so they can do anything, but not enough so they can do nothing.”

What Types of People Have High Net Worth?

Wealth typically builds with age.

High-net-worth individuals are usually older people (50+), having saved and invested steadily over the years.

Income also tends to rise with age, but retirees are mostly low income, but still high net worth.

Investors, especially growth investors: Stock market (equity) investors, business owners and investors in leveraged real estate (with large mortgages).

Equities (stock market or businesses) are the highest growth asset class. Equity investors & business owners both invest in businesses.

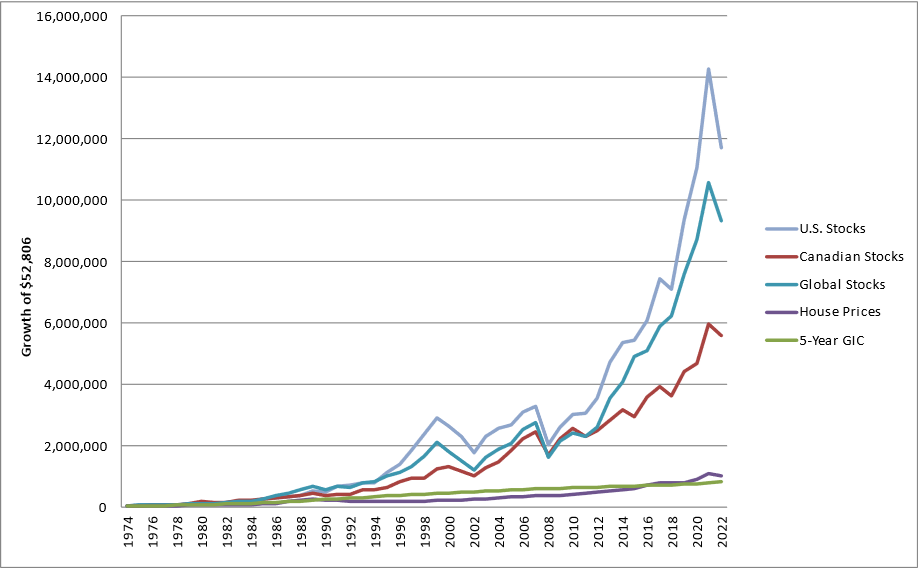

Example of wealth over 40 years in stocks vs fixed income (bonds) vs real estate. Growth of $52,800 (average house in Toronto) in 1974 is just over $1 million now in real estate, $825,000 in fixed income, but almost $10 million in global stocks:

The highest net worth individuals also often use leverage effectively, borrowing to invest in growth assets. Nearly all very wealthy people borrowed to invest in investments or their business.

Those who can handle investment risk may benefit from strategies like the Smith Manoeuvre or other forms of investment loans, which, over decades, can significantly amplify wealth.

For example, the Smith Manoeuvre or investment loans (e.g., 3:1 investment loans) for investors, a business with large loan, or real estate with huge mortgage.

Example of wealth for people that leveraged vs. no leverage.

Invest $4,167/month for 30 years: Investments $5,869,000.

Borrow $1 million to invest and pay $4,167/month interest for 30 years (30% tax bracket): Investments $20,825,000 (net of loan).

Investments 4 times higher with the same cash flow.

What Does the Lifecycle Investing Study Tell Us About Growing Wealth?

A study by Yale professors shows that starting with a large investment portfolio early in life can yield more wealth than incremental savings.

It works much like borrowing as much as possible to buy a home when you are young and then pay it off by your mid-50s and move to your target asset allocation by retirement.

This study showed that 100% of the time this has created more wealth than the normal bit-by-bit savings most people do.

It works because you start with a large investment portfolio when you are young.

This method minimizes the “last decade risk,” where low returns late in your investing years can reduce your lifetime gains.

For instance, If you invest for 40 years from age 25-65 and your investment returns are low in the last decade from age 55-65, then your 40-year return is low, because nearly all your investments are held in the last decade.

Your rate of return the first decade from 25-35 is almost irrelevant, because you have hardly any investments then.

Conclusion: When you are young, having large investments is what matters much more than your rate of return. To build wealth, try to get as much money invested as possible when you are young and it can grow for 40 years – even if you have to borrow it.

Note this is not for everyone. Only for growth-focused people that want to focus on being wealthy and who will stay invested for the long term.

The key takeaway?

Investing as much as possible when young allows wealth to compound over 40+ years.

How Can You Become Wealthy?

1/ Wealth Builds with Age: Invest as much as possible when you are young.

2/ Save and Invest Early: You’ll benefit from 40 years of compounding.

3/ Invest in Equities (stock market investments): Make regular contributions to growth investments like equities, a business, or real estate with a large mortgage are critical.

4/ Borrow To Invest (leverage) into equities: This is the most effective growth strategy if done by the right people in the right way over the long term. Lifecycle Investing study is an example of how this can work over decades.

Wealth doesn’t happen overnight.

It’s a gradual process of smart investments, consistent savings, and strategic planning.

With these insights, you’ll have a better sense of what it takes to build wealth and the types of choices that support financial success over the long haul.

Ed

Planning With Ed

Ed Rempel has helped thousands of Canadians become financially secure. He is a fee-for-service financial planner, tax accountant, expert in many tax & investment strategies, and a popular and passionate blogger.

Ed has a unique understanding of how to be successful financially based on extensive real-life experience, having written nearly 1,000 comprehensive personal financial plans.

The “Planning with Ed” experience is about your life, not just money. Your Financial Plan is the GPS for your life.

Get your plan! Become financially secure and free to live the life you want.

Hi Tonet,

I’m glad you found it helpful for you.

Ed

I am thankful that I found this web site, just the right information that I was searching for! .